“We’re not just going to start with a clean slate, we’re going to throw the old slate away.”

-Vince Lombardi (1959)

That was one of the first iconic leadership quotes to come out of Vince Lombardi’s mouth when he moved his family to Green Bay, Wisconsin in 1959 (page 207 of “When Pride Still Mattered”, by David Maraniss).

As all great leaders across history have proven, results matter more than rhetoric. But, when you can combine both, you have the holy grail of life’s opportunities – to “be the change you want to see in this world” (Gandhi).

Barack Obama and Johnny Boehner are not Gandhi. Neither are they Lombardi. These two gentlemen would have a tough time leading me to the men’s room at a Yale Hockey game without forming a committee. And, sadly, after we get this morning’s stock market rally out of the way, we’re all going to be stuck with their same Old Slate.

This isn’t to say that this gong show of a Debt Ceiling Debate isn’t going to help America start with a clean slate. First though, we need to throw away the old one! That will take time. Change is a process; not a point.

Back to the Global Macro Grind…

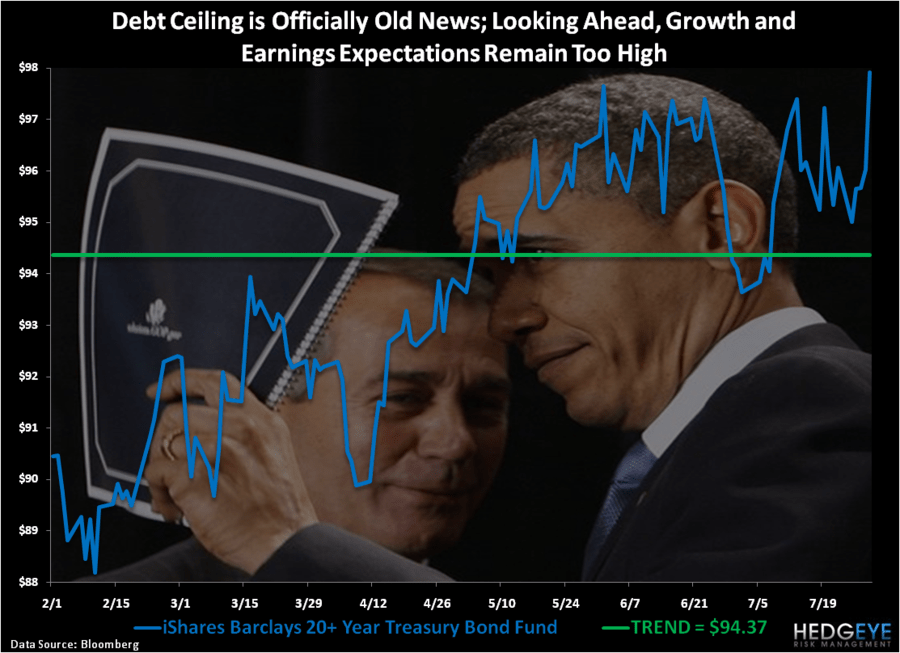

With the most anticipated headline since ‘sun rising in the East’ behind us, the question for Risk Managers now isn’t about the mechanics of the debt “deal” (it will be back end loaded and will not move the dial until all of these politicians are gone) – it’s about Global Growth and Earnings Expectations – both are still too high.

Here’s how the globally interconnected market is reacting to the “news” that Washington does career risk management:

- STOCKS – Asia rallied across the board to lower-highs and remains the best looking region of the 3 majors (Asia/Europe/USA); European Equities are up marginally on low volume and basically still look awful; US Equities have immediate-term downside support at 1286, but a wall of intermediate-term TREND resistance up at 1319 on the SP500.

- TREASURY BONDS – We’ve been on the other side of the PIMCO “credit risk” trade (El-Erian) and focused more on the two things that have really provided a bid for bonds since April – US Growth Slowing and Inflation Expectations coming down. We saw new highs in 10 and 30-year UST bonds on Friday into the “news.” Now Treasuries are immediate-term TRADE overbought.

- EUR/USD – This is the one strike price that should continue to whip around in the next 48 hours as we finally put this debt deal dog to bed. Watch $1.43 as your TREND line that inflates/deflates everything else (across asset classes). The global market’s Correlation Risk moves off that.

From the Eurocrats to the Fiat Fools of the Keynesian Kingdom in America, do any of these people realize the causal relationship between debt and growth?

Republicans and Democrats, Reid my Boehner on this:

DEBT STRUCTURALLY IMPAIRS GROWTH.

That’s it. So keep it simple stupid. The only thing that you are really doing to global markets and economies are:

- Shortening economic cycles

- Amplifying market volatility

How short was the last “bullish” economic cycle? You tell me (if you are a Washington/Wall Street person you will have a different answer to this question than Main Street, fyi). The only thing worse than Friday’s Q2 US GDP report of 1.3% is the thought that the government’s made-up number could be off by 81%! (Q1’s was restated at 0.36% versus 1.92% prior!!!)

I think that’s the first time I have used 3 exclamation points in an Early Look. Re-read that fact about reported US GDP. Maybe I should have used six!!!!!!

Either these Republicans and/or Democrats figure out how to throw out this Old Slate of failed economic policy, or The People are going to throw all of them out. That’s the change I can believe in.

My immediate-term support and resistance ranges for Gold (sold ours last week), Oil (no position), and the SP500 (no position) are now $1, $95.96-100.49, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer