This note was originally published at 8am on July 26, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The measure of who we are is what we do with what we have.”

-Vince Lombardi

This weekend I finished the “heavy book” (Truman) and opted to do what I don’t do enough of – re-read my favorite books. If “When Pride Still Mattered – A Life of Vince Lombardi” can’t get you fired up to lead people in this good life, I don’t know what can.

Leadership isn’t what you saw coming out of Washington yesterday. That was a joke. As Lombardi reminds us, “leaders aren’t born, they are made.” And President Obama is learning that lesson the hard way right now – unfortunately, on the job.

I’ve written about this for what feels like forever now, but the reality of both the Bush and Obama Administrations is that the American people don’t like either. Americans aren’t stupid. They know who these people are by watching what they do with what they have. Both Bush and Obama had/have awful economic advisors.

Back to the Global Macro Grind…

Last night, after the President of the United States fear-mongered the country that we could face a “deep economic crisis”, the rest of the world’s market participants took his word for it and said ok, we’ll sell more US Dollars on that.

Can you imagine the leader of any great team delivering that message to the troops on the week of the one of the biggest games is US history? I can. I’ve seen plenty of losing coaches in my day, and so have you. Obama better wakeup to a winning message – and soon.

The good news is that market prices are already discounting political gravity. If you haven’t noticed, professional politicians chase polls and the President’s approval rating won’t be flushed out of the toilet until he makes a decision to get a deal done.

Here’s how I see this globally interconnected marketplace discounting Obama bellying up to the bar:

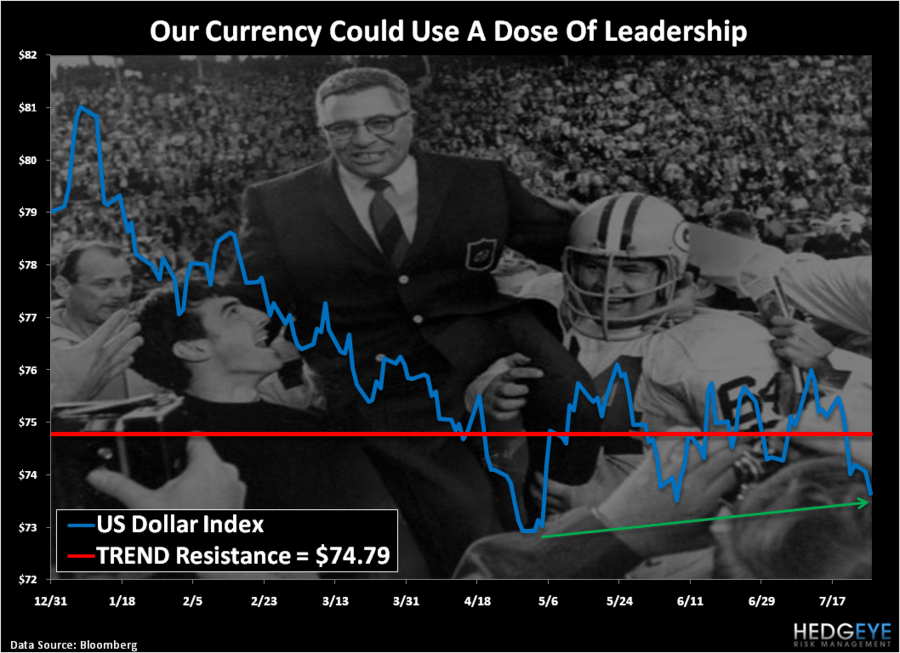

1. US Dollar – yes it was down -1.2% last week and, yes, it’s down on “no deal” already for the week-to-date. But, the US Dollar Index is finally making higher-all-time-lows on selloffs. All-time is a long-time. Obama, this buck stops going down with you.

2. US Treasuries – you know you have basically no stroke with markets when 3 of the “top” central planners of America (Obama, Geithner, and Daley) try to scare the living hell out of the bond market, and Treasury Yields move a beep. Or was it 2 beeps?

3. US Stocks – like Braveheart, US stocks are holding every line of support that matters. Holding our TRADE line of support (1325). Holding our intermediate-term TREND line of support (1319). “Hold… hold…”

The People of America are like that. I’m sure Lombardi would agree that our markets are a measure of who we are. We are resilient. We are fighters. And we will not let conflicted and compromised politicians decide our future.

This will not be easy. This won’t change the fact that Washington/Wall Street has been wrong on their US GDP Growth estimates by about a half in 2011 either. But this definition of leadership will not continue.

America will do what she needs to do with what she has to make sure of that.

My immediate-term support and resistance ranges for Gold (sold ours yesterday), Oil (no position), and the SP500 are now $1596-1619, $97.90-100.55, and 1325-1352, respectively.

Best of luck out there today and God Bless America,

KM

Keith R. McCullough

Chief Executive Officer