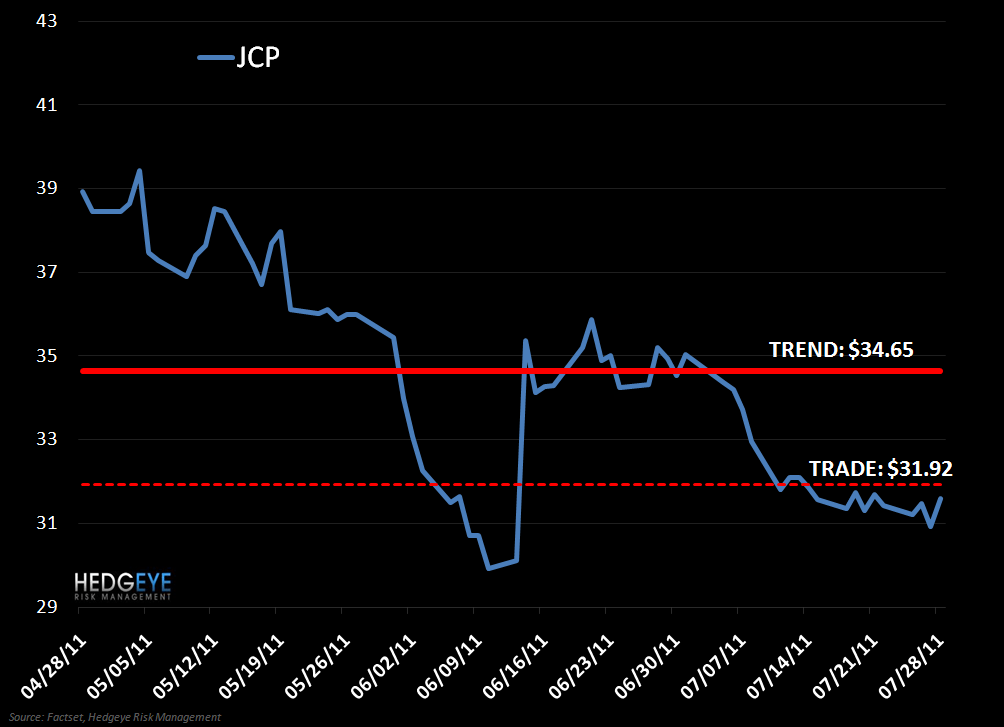

Keith re-shorted JCP after an analyst upgrade offered the opportunity for more downside. Hedgeye Retail remains negative on all durations (TRADE, TREND and TAIL). Too much storytelling around Ackminism obfuscating poor positioning in the face of major industry risks, and what is likely to be a very sloppy management transition – both of which should take estimates (and the stock) down before they can ultimately go up.

This afternoon, the Hedgeye Retail team will be releasing our RETAIL Black Book, JCPENNEY - WHAT ACKMANISTS ARE MISSING, following up with a conference call on Tuesday August 2.

Please contact if you would like to receive the report and/or participate in the conference call.