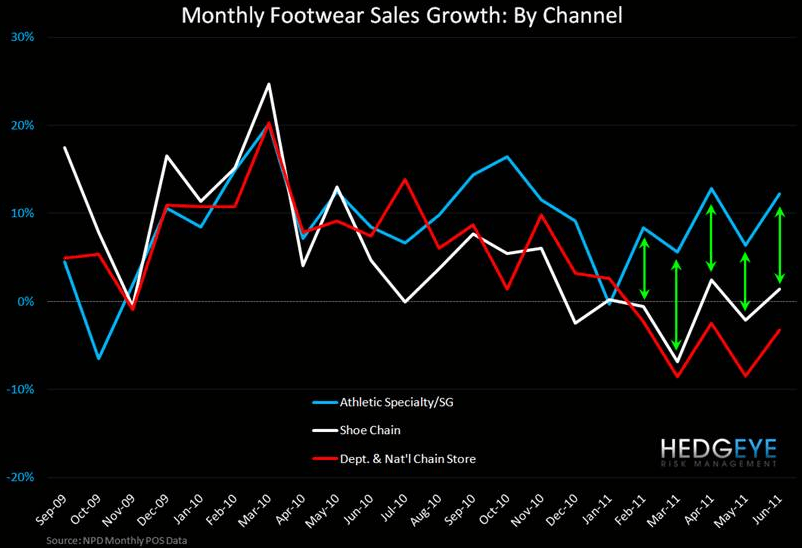

Big switch in FW vs. Apparel this week. The key is that apparel had tough numbers to comp, FW didn’t. This is in contrast with the strong monthly data we have for June, but that’s backward looking vs. the weekly numbers. The spread between the athletic specialty and other channels is getting wider suggesting that the FLs and FINLs of the world are not getting hit nearly as hard as the weekly numbers suggest, but still down sequentially nonetheless.