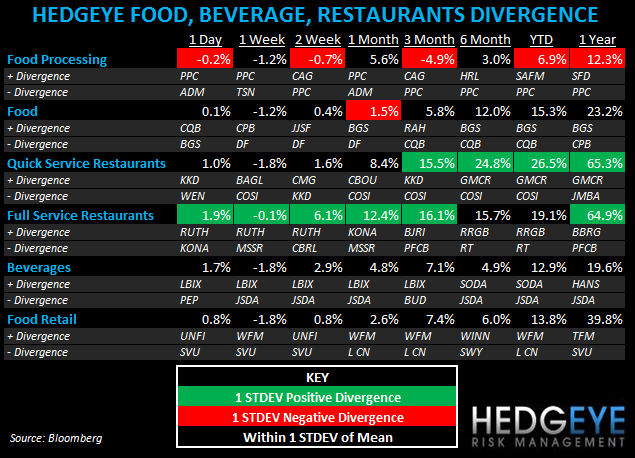

Notable news items and price action pertaining to the restaurant space as well as our fundamental view on select names.

MACRO

The performances of the QSR stock yesterday continue to suggest that business trends continue to remain strong ad that this should be a strong earnings season. The food processors continue to struggle with high commodity prices.

Lower energy prices and a downshift in the domestic economy have taken the edge off U.S. import prices, as they fell 0.5% in June. Imported food and beverage prices fell 1.9% in June, larger than the 0.7% decline in May.

This morning, jobless claims were above 400k yet again, coming in at 405k. While this was below consensus at 415k, and the week prior’s revised 427k, it shows that the employment scenario is still far, far away from improving meaningfully. 4-week rolling claims declined slightly week-over-week but remain elevated at 423k.

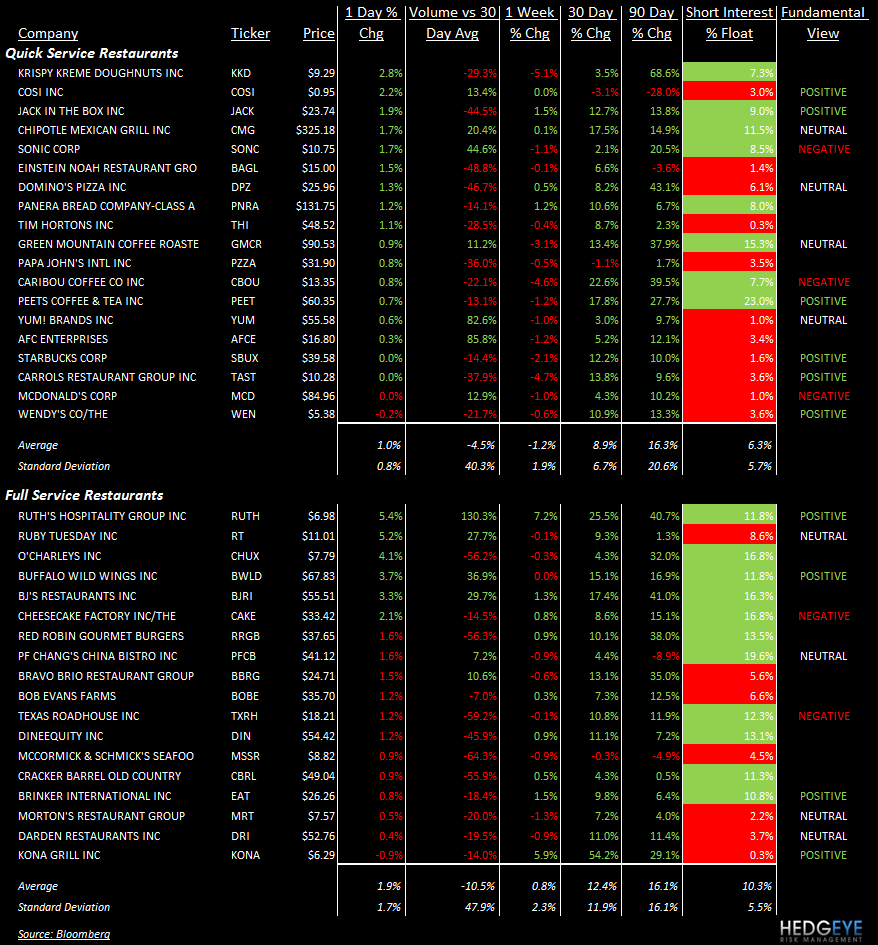

QUICK SERVICE

- YUM beat expectations on the back of outstanding +18% same-restaurant sales growth in China. Margins in China were down, however, and the consolidated tax rate was lower-than-usual, providing a boon to earnings. YRI comps were up +2% and the U.S. comps declined -4%. The earnings call will take place at 9:15 am.

- YUM’s KFC was mentioned, alongside KO, as two companies that sent representatives to North Korea earlier this month to discuss opening branches in Pyongyang.

- SBUX has debuted a new kiosk concept at the JW Marriott Indianapolis. According to a company release, the new kiosk will feature the full Starbucks menu.

- MCD has prevented Russian authorities not to double its tax bill by persuading them that its outlets are supermarkets rather than restaurants.

FULL SERVICE

- RUTH, RT, BWLD, and BJRI all gained on accelerating volume.

Howard Penney

Managing Director

Rory Green

Analyst