Conclusion: Sales look decent headed into Thurs. But we think that anecdotes We will fuel the fire for the Street on 2H margin weakness – especially as it relates to earnings season beginning for the vendors in 2 weeks. This has been our call (4.5 Below – 450bos of margin weakness beginning in 2H) and we’re sticking with it. Short JCP, HBI, GIL, COH, CRI, JNY. Long NKE, LIZ, FL.

Before looking forward, let’s set the context as to where we stand today, and what we’ve been fed over the past year at a Macro level.

As important as things like weather and calendar shifts are, let’s start off with a couple of bigger picture points about the Macro climate ‘then versus now.’

- Gross Personal Income was running at about 2.5% compared to about 4.5% today. That’s a function of slightly lower unemployment and marginally higher nominal wage. (positive point)

- The two main levers that account for the delta between Gross Income and Personal Consumption pretty much wash each other out.

- The consolidated personal tax rate has risen above 10% vs 9.1% this time last year. (negative point)

- The personal savings rate, which had been running at 6.1%, has since trended back to 5%.

- When we look at what we call ‘essential spending’ (food, energy, healthcare), we’ve seen growth go from 2.6% last year up in nearly a straight line to around 4.3% today.

- All that’s left goes into the ‘discretionary spend’ bucket which is far more volatile. This stood at a healthy 7.5% a year-ago – a level that remains today (at least for now).

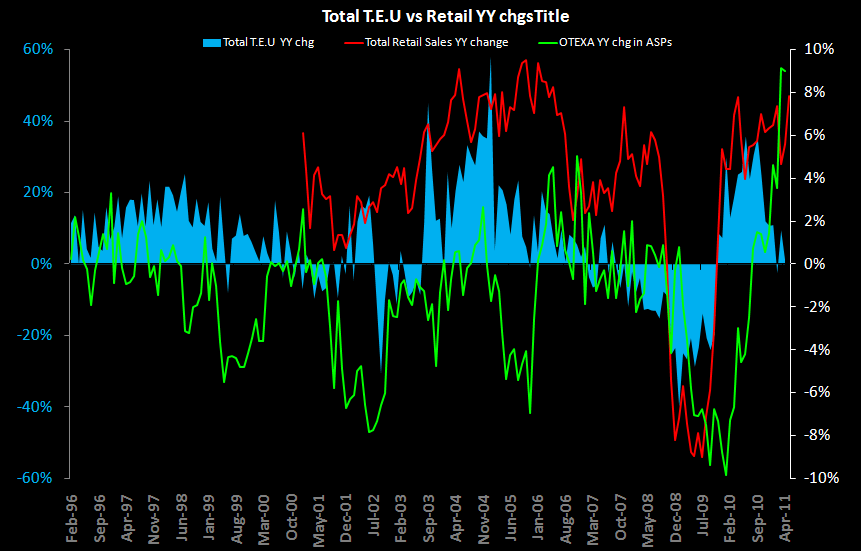

- Based on our read out of POS data (NPD, SportscanINFO), sales for the month of June were pretty much middle of the road. Apparel decelerated over the course of the month, albeit still positive. Footwear unit growth accelerated, though it the direct result of slightly lower price points. Overall there are nit picks here and there, but the trend overall is unremarkable.

What’s Next?

- We think that sales day will be another domino to tip as it relates to giving additional datapoints to the Street about margin weakness – especially as it relates to earnings season beginning for the vendors in 2 weeks. This has been our call (4.5 Below – 450bos of margin weakness beginning in 2H) and we’re sticking with it.

- The consumer’s top line – believe it or not – strengthened materially beginning in July of last year. Personal income growth accelerated over 3% -- -and hasn’t looked back. Now we go against that in 2H. Perhaps it stays at that level. But our point is that the yy delta helped out so many in retail – and that’s no longer there.

- Could we get a few bps of tax relief to buoy spending? Maybe. But not over 100bp. It’s simply not there – even with the political calendar heating up.

- Is the consumer going to draw the personal savings rate back down to 2-3% to free up a few points of spending? It’s possible – especially given US consumer spending habits. This is the biggest area where we could be wrong with our call in 2H. But that will make the setup for 1H12 very grim – i.e. low taxes, trough savings rate, with interest rates nowhere to go but up. That’s the ultimate defensive position for the consumer.

- Check out the weekly average earnings chart below. There was a whole lot of nothing until May 2010, until growth accelerated meaningfully – peaking in October, and remained at healthy levels throughout year-end. We’ve got to comp against this.

MIND THE LAG!!!

We all know that ‘the cotton trade is dead.’ That’s been the consensus for 7 months now. But we still think that the ‘earnings trade’ is very much alive. Remember that cotton, oil and other raw materials generally have a 9-12 month lead time. That means that what is selling today was procured last summer/early fall of last year. That’s precisely when costs started their precipitous ascent. We’ll have to deal with this for the next year at a minimum. Likely longer. We still don’t think we’re looking at a recovery until 2013 in this space.