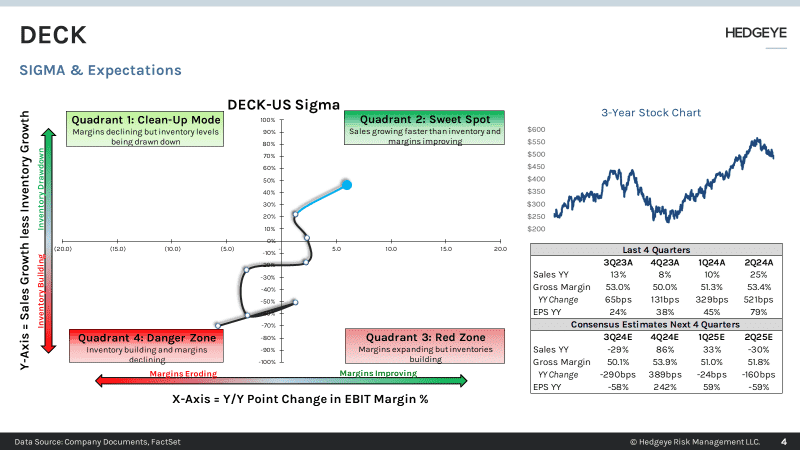

DECK out with an impressive print... big revenue and EPS beats and revenue accelerating on a consolidated basis and at UGG. HOKA growth has been slowing over the last few quarters, still up 27% YY but that rate is stable with last Q also up 27%. About a month back we took DECK from our Best Idea Long List to our bench due to a) the fact that the stock doubled since we made it a Best Idea, while the consensus closed about 50% of the gap between our estimates and the Street, and b) headwinds from Nike, which is likely to release a major running platform in the Spring, which we think is targeted at ONON in particular. The 'monkey math' around DECK is to give HOKA an ONON multiple, and slap 6x EBITDA on UGG. Note...that would still get you to a stock over $700. But we think the risk of ONON blowing up is very real, which could take DECK lower. The company characteristically kept the year on a beat, and guided down the upcoming quarter, which we think is too conservative given the momentum that the brands have, as well as the extremely bullish SIGMA move we saw this quarter (bullish for margins in the upcoming quarter). The company also stepped up its stock repo with $185mm this quarter. In fact, the only change we made to our model is materially upping the stock repo in 2024 and the outer years. While no longer a Best Idea, we still think this stock is headed higher. If it trades down with the rest of retail over the next 6 months (we expect the group to act like death) or if it gets shellacked on an ONON blow-up, we're likely to put this back on our Best Idea Long list. See Elevator Pitch and SIGMA analysis below.