R3: REQUIRED RETAIL READING

June 28, 2011

RESEARCH ANECDOTES

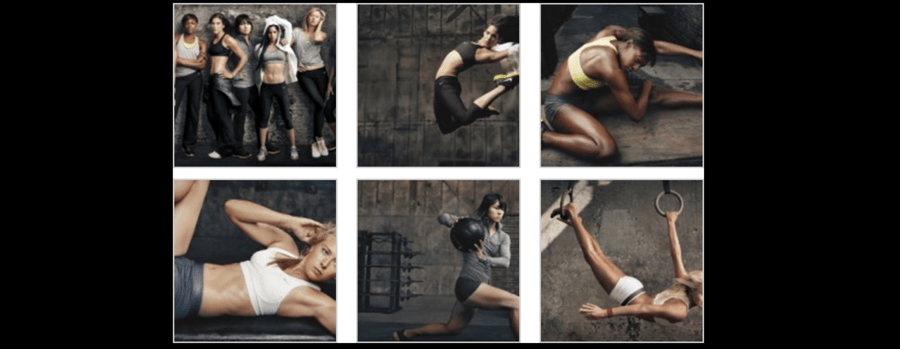

- Among the many new product previews likely to accompany Nike’s analyst day presentations, today could include a sneak peak at the company’s latest “Make Yourself” campaign. The 2011 iteration slated to air this fall was shot by Annie Leibovitz highlighting seven professional women athletes. Interesting to note the stark contrast between these images and Lululemon’s current campaign (leisurely, bright, airy). Chiseled physiques like these don’t just happen. Accompanying a campaign like this with new innovative product, will make for a highly competitive women's athletic apparel market over the next 12-24 months.

OUR TAKE ON OVERNIGHT NEWS

Tommy Hilfiger Eyes Stake in Michael Kors - Tommy Hilfiger’s original investment team may soon be back together again. Tommy Hilfiger and Joel Horowitz are said to be among the private investors due to invest in Michael Kors, joining their previous partners, Silas Chou and Lawrence Stroll, who bought Michael Kors in 2003 for a reported $100 million, according to sources. Kors is seeking to raise as much as $500 million to fund its global expansion plans and has hired Morgan Stanley to sell an equity stake of about 25 percent. The round of financing is closed and is expected to be finalized in July, according to a financial source. Hilfiger, who was traveling in Europe, declined to comment on whether he will invest in Kors, but told WWD: “Anybody would be crazy not to invest in it. Michael Kors is the next major global player in my eyes.” <WWD>

Hedgeye Retail’s Take: Kors has been one of the fastest growing brands in recent years and his recent efforts to expand the brand internationally illustrates its strength. Back in March, Kors opened his first full collection international store with a flagship in Paris to accompany the five he has stateside. With Kors looking to sell only a 25% stake, we can’t imagine demand was an issue here. Given Tommy’s international experience and ties to the brand’s current owners, it would be more surprising if he wasn’t involved in some form.

Old Gringo Sues Lucky Brands - Western boot maker Old Gringo has sued Lucky Brands, a division of Liz Claiborne, for unfair competition. Old Gringo alleges Lucky has made a “cheap knock-off” of its popular Marsha boot, and sold an “unauthorized” copy of the style, which involves a distinctive embroidered boot with a side zipper. The style has been a best seller for Old Gringo, and the Chula Vista, Calif.-based firm is seeking injunctive relief for unfair competition and false advertising. It first filed its complaint on March 23, 2011, in the U.S. District Court for the Southern District of California. In the lawsuit, Old Gringo claims it first designed, manufactured and sold the Marsha boot to specialty boutiques in the western U.S. in July 2008. Calling the boot “a work of art,” the firm added that the Marsha became the firm’s best-selling style by 2009. <WWD>

Hedgeye Retail’s Take: This one falls into the any news is good news camp. Lucky is starting to finally turn under Dave DeMattei and this ‘slip up’ may not be the worst thing for the brand since it suggests a fashion awareness that the brand had been lacking. Anecdotes like this suggest the brand could be starting to get the women’s business right.

Macy’s Goes Global - Macy’s Inc. today kicked off international sales to online shoppers in 91 countries. Consumers can place orders at the retail chain’s Macys.com and Bloomingdales.com e-commerce sites. U.S.-based shoppers also can ship gifts bought through Macys.com or Bloomingdales.com to customers in those 91 countries (see the list below). “International shipping will enable Macy’s to build upon its existing customer base beyond the United States by exposing our product offerings abroad,” says Kent Anderson, president of Macys.com. The company says international shoppers accounted for 36 million web site visits to Macys.com last year. Macy’s Inc. is No. 17 in Internet Retailer’s Top 500 Guide. <internetretailer>

Hedgeye Retail’s Take: Macy’s is among the early adopters to take their business global. Within the past month, Williams-Sonoma, Barneys New York, and Jos. A Bank all launched international e-commerce programs. While not as aggressive as WSM’s free shipping launch, this move provides Macy’s with a substantial opportunity to further expand its online business, which the company has been successful in growing and which accounts for over 20% of sales.

Brooks Bros. to Carry College Licensed Apparel - Brooks Brothers has reached an agreement with IMG Worldwide Inc., the owner of The Collegiate Licensing Company (CLC), to sell college-licensed apparel for the first time in its almost 200-year history. The agreement allows for the sale of merchandise, beginning Aug. 15, from 15 schools, including Alabama, Auburn, Boston College, Cornell University , Georgetown, Georgia, Harvard, the U.S. Naval Academy, New York University, Notre Dame, Ohio State, Princeton , Stanford, Vanderbilt and Virginia, according to a report by Bloomberg. Items were be available depending on the proximity of each school's campus to Brooks' stores. The lines, for men only, will comprise sweaters, dress and polo shirts and ties. Eventually a children's and women's line is expected to be added as well. <SportsOneSource>

Hedgeye Retail’s Take: Really? Brand dilution is the first thing that came to mind after reading this. There are a lot of ways to capture a younger demographic, but this one is a stretch. There’s something about logoed shirts that just doesn’t resonate with preppy.

Blue Nile Moves Away from Engagement Rings - Online jeweler Blue Nile Inc., which posted record sales of $80.2 million during the first quarter, plans to grow its business by offering more moderately priced engagement rings and expanding its product assortment. Blue Nile’s core business is engagement rings, which represent about 68% of its annual revenue, Vijay Talwar, interim chief financial officer and general manager of international, told analysts last week at the Goldman Sachs Second Annual Dot Commerce Day. Non-engagement business, such as necklaces or bracelets, accounts for the remainder of revenue. “That’s essentially what our model is based on and how we’ve been able to grow and get to this point,” Talwar says. For Blue Nile, No. 60 in the Internet Retailer Top 500 Guide, the average ticket for engagement rings is about $6,100, he says. That compares with the U.S. average of about $3,200.

Hedgeye Retail’s Take: Now this makes sense. Evolve as your customer’s needs do is a time honored retail tradition. Ideally, Blue Nile would have evolved its offering a few years ago, but as they say, better late than never.

Dwyane Wade Designs for Hublot - Dwyane Wade might have sat front and center during the men’s fashion weeks in Milan and Paris, but on Monday the basketballer unveiled a luxury design venture of his own: a limited edition timepiece created in partnership with Hublot. Hublot’s King Power “D-Wade” watch, which will bow in late fall, is comprised of a black, micro-blasted ceramic casing offset with red detailing. Retailing for $20,000 with production limited to 500 pieces, the 48mm timepiece is Wade all the way — from the stitching on the black leather strap that’s made to look like a basketball net, to the subtle “basketball effect” of the watch face. There is also a “3” on the face (Wade’s Miami Heat number), and the player’s new logo appears on the back. <WWD>

Hedgeye Retail’s Take: Yet another sign that the premium luxury watch market is in the stratosphere.