Highlighting FHA Exposure

In light of today's news about BAC hindering the HUD foreclosure investigation, we are revisiting Bank of America's exposure to potential losses from the FHA insured loan pool.

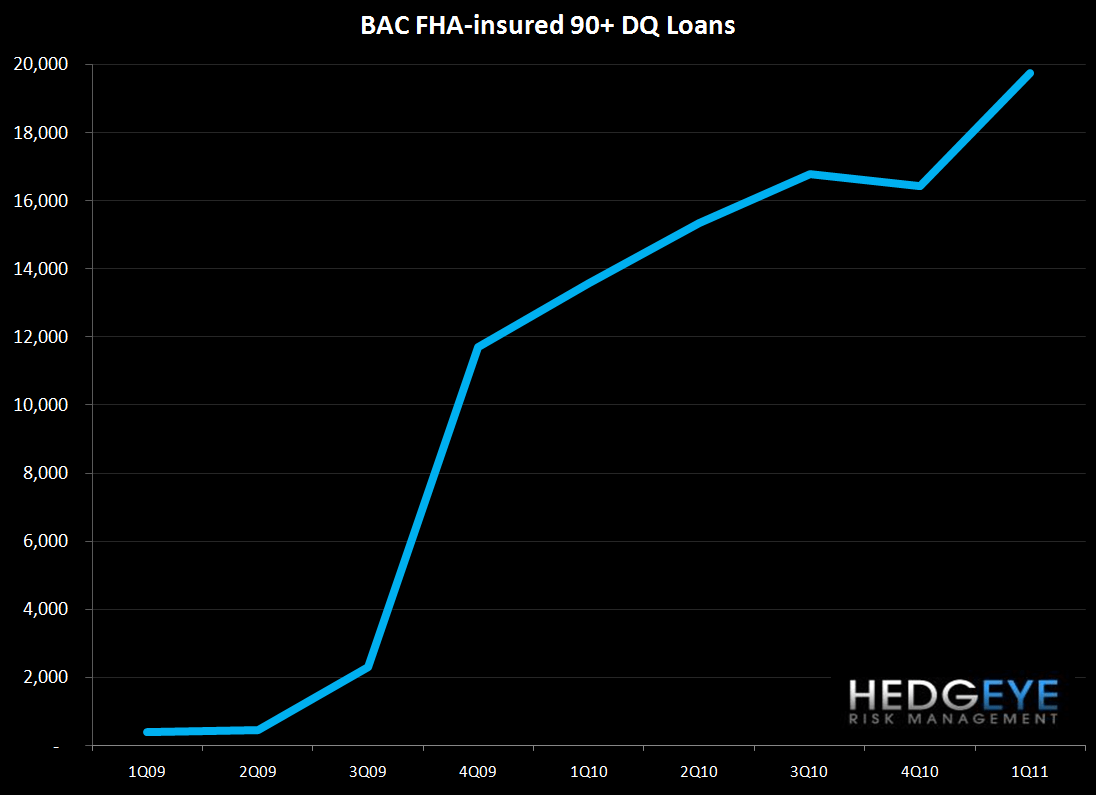

Bank of America currently holds $20B in 90+ days delinquent FHA-insured loans on its books, up from just $400 Million two years ago. When a loan defaults from a GNMA trust, BAC buys it out of the trust to minimize the servicing advances on the loan. Since these loans are insured by the FHA, Bank of America should theoretically have no associated liability. However, we doubt that this will be the case.

Return of the "Fantastical Stretch"

Our primary concern around BAC's exposure is that they would be subject to a suit analogous to the May 4, 2011 Dept of Justice suit against Deutsche Bank. As we wrote when the lawsuit hit the news in early May, "The US Attorney said in the press conference that it would not be a "fantastical stretch" to expect other institutions to face lawsuits, while the general counsel for HUD added that HUD would make "appropriate referrals" to the DoJ wherever they suspect underwriting fraud."

Recall that the DoJ sued Deutsche on behalf of the FHA under the False Claims Act, which permits triple damages. The treble damages is a punishment clause intended to dissuade businesses from defrauding the government. As the GSEs are not technically government entities this law did not apply to them, but the FHA is a direct government agency. The FHA alleged that Deutsche had lied about its underwriting policies on 39,000 loans originated between 1999 and 2009, of which 12,500 later defaulted. The FHA had paid out $386M in insurance on the contested loans. If all $386M in insurance payments was a False Claim under the law, Deutsche's liability could be more than $1B.

Afterparty at the FHA

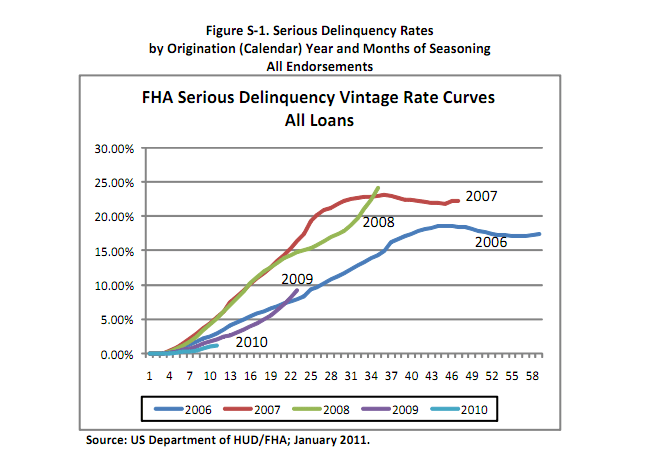

As the chart below demonstrates, credit quality at the FHA deteriorated significantly in 2007-2008. At the same time, volume increased sharply on both a market share and absolute basis. This is a classic case of adverse selection. The subprime party ended in 2006/2007 and the party then migrated to the "afterparty" at Fannie and Freddie where it carried on for about 18 months. Beginning in early 2008 and continuing still today the "after-afterparty" has been at the FHA. If anyone doubts this, have a look at the loss curves associated with late vintage FHA loan books. The bottom line is that the FHA will ultimately get around to seeking recourse on what was clearly terrible underwriting. The Deutsche case was the first shoe to drop, but there will undoubtedly be others.

GSE Putbacks as a Model - Liability Likely $4.5B+

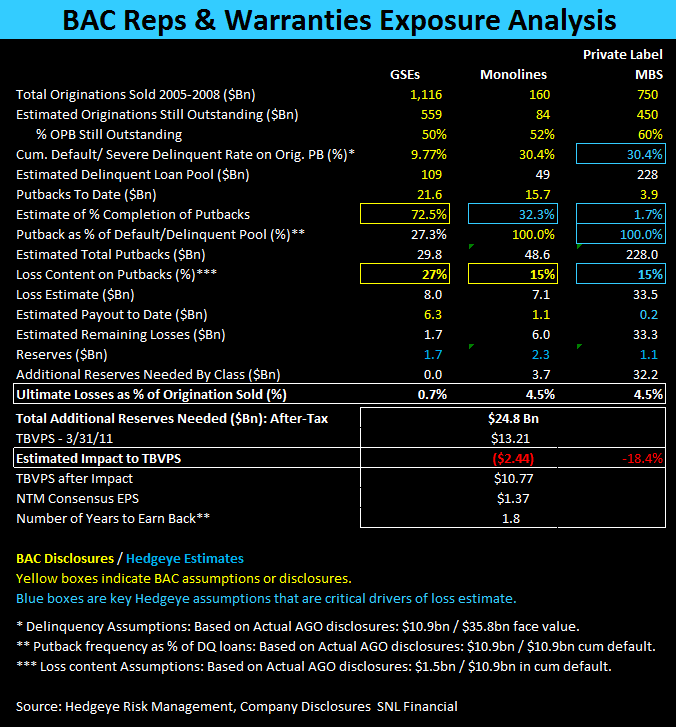

To get some idea of the magnitude of potential losses from FHA loans, we can use the GSE experience as a guide. Bank of America has disclosed that the GSE delinquent loan pool is $109B. The table below walks through the steps to determine ultimate loss content. Bear in mind that this methodology is predicated largely on BAC's own numbers and estimates, which likely understates the problem. The bottom line is that BAC will likely end up paying $8B+ on $109B in delinquent Fannie/Freddie loans, or a loss rate of 7.3%.

Looking at only the $20B in 90+ FHA loans currently on BAC's balance sheet, and applying a 7.3% loss rate, the minimum liability would be $1.5B. This doesn't take into consideration defaulted loans no longer on BAC's books (where the FHA has already paid the insurance claim).

Keep in mind that if the Department of Justice were to pursue BAC under the False Claims Act, as they have with Deutsche, BAC would be exposed to triple damages. On our math, that works out to at least $4.5B. This would be in addition to the $25 billion we already think they're on the hook for (see our table below for details).

Chinese Water Torture

For Bank of America, housing exposures keep adding up. We estimated in our 5/10/2011 note ("BAC: Another Big Charge is Coming in 2Q11 as Home Prices Fall Faster") that BAC is likely to see another $1B write-down related to the GSE settlement in 2Q, based on ongoing declines in home prices. Further, the PCI book is significantly exposed to downside in home prices - we estimate potential further losses of 10-30% on the $41.7B book, or $4-12B, over the next several years. Again, all of this is in addition to the $25 billion itemized in the table above and the $4.5 billion enumerated on the FHA front. Moreover, Bank of America will have a substantial share of the eventual servicer settlement (we estimate $6.7 billion here), when it is finalized in the likely not-too-distant-future. For those keeping score, that's a sum total of $45.2 billion.

Given this magnitude of loss content coming down the pike, we think it goes without saying that it's justified for BAC to be trading well below tangible book value until some clarity emerges to contradict these estimates.

Joshua Steiner, CFA

Allison Kaptur