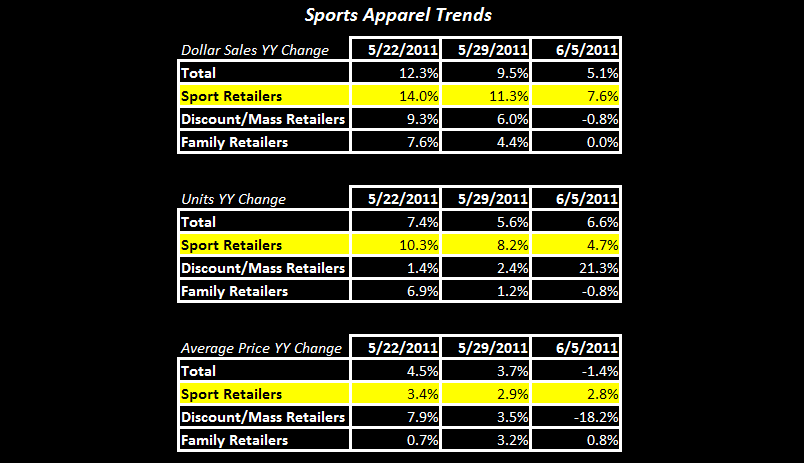

Despite ASP strength in the athletic specialty channel, a sharp deceleration in pricing across the industry suggests retailers could be looking to clear inventory ahead of the 2H driving further margin pressure near-term.

Athletic apparel sales slowed for the second consecutive week. Sales in the athletic specialty are also slowing on a sequential basis, however, the channel outperformed the broader industry and for the fourth consecutive week. More notable is the ASP strength in the athletic specialty channel up MSD relative to a sharp deceleration in pricing across the industry, which was down for the first time since March. This is consistent with recent commentary across the industry suggesting that retailers could be looking to clear inventory ahead of the 2H, which we expect to accelerate margin pressure in here in Q2 – less favorable for DKS and HIBB.

Casey Flavin

Director