This note was originally published at 8am on June 03, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The century of megacities has already begun.”

-Lawrence C. Smith (“The World In 2050”)

I’m writing the Early Look from Los Angeles, California this morning. According to Lawrence Smith’s research in an excellent book I just finished reading, “The World In 2050”, Los Angeles-Long Beach-Santa Ana is the world’s 11th largest Mega City (a city with more than 10M people). Next to New York-Newark, which I’ll be on a plane to later this afternoon, that makes LA the only US city in the global top 19.

Most of you probably knew that.

What I didn’t know (from Lawrence’s data compilation in his chapter titled “A Tale of Teeming Cities”):

- The world had 2 megacities in 1950

- The world has 19 megacities now

- The world will have at least 27 megacities by 2025

“Of the eight new megacities anticipated over the next fifteen years, six are in Asia, two in Africa, and just one in Europe. Zero new megacities are anticipated for the Americas. Instead this massive urbanization is happening in some of our most populous countries: Bangladesh, China, India, Indonesia, Nigeria, and Pakistan.” (Smith, page 34)

Now there are obviously plenty long-term investment implications associated with a world that continues to move East. And I assume most of you probably know that too – but what we don’t know is what this balance of population-power is going to do to our Western Dogma of ZERO percent interest rates - and the associated pillaging of our savings (Asians and Muckers like to save).

Being on the road, I get into a lot of fascinating debates with some of the world’s sharpest investing minds. This has been the most intellectually fulfilling aspects of building Hedgeye. Meeting with people who run the buy-side is infinitely more interesting than having a sell-sider beg me for a bonus, bailout, or an II vote.

One of the current debates I have been getting into with buy-siders centers on how long America can sustain Japanese and Western European monetary policies?

Good question - with answers that continue to be tattooed with partisan politics (yes, being a Keynesian is partisan):

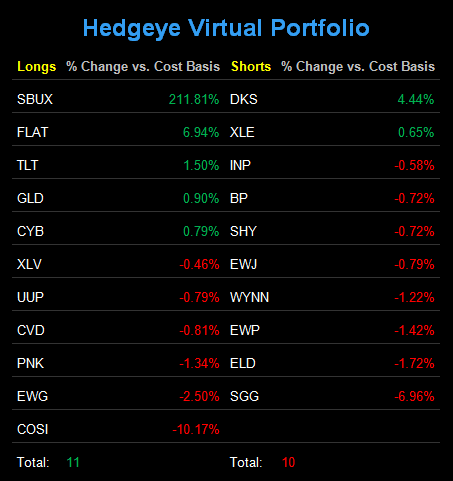

- US Monetary Policy – we have two views; what Le Bernank should have done (raised rates 6 months ago) and what he will do (nothing – he hasn’t raised rates since 2006 and he won’t start now). Our Q2 Macro Theme remains that the Fed will remain “Indefinitely Dovish” (no QG3 and no rate hikes), which is why we are long a UST Flattener (FLAT) and the long-bond (TLT).

- Western European Monetary Policy – we have one view; Les Eurocrats will remain socialist in their leanings even though they are pretending to be chicken hawks post their most recent rate hike (ECB raised rates before the Fed for the 1st time ever). Le Trichet will be gone by year-end and replaced by a left-leaning Italian (Mario Draghi). We think he could cut rates within his first 3-6 months.

- Eastern European and Asian Monetary Policy – they have one view; fight inflation with the weaponry allocated to the Fiat Fools. Russia shocked me early this week with another interest rate hike and obviously the Chinese and Australians have raised interest rates 6 times respectively since this short-cycle global “recovery” began.

More objective policy makers who use the blunt fiat instrument of interest rate decisions both ways (like yesteryear’s Bundesbank or today’s Reserve Bank of Australia), have learned over the years that there is one unique advantage to having the stones to raise interest rates – THEN YOU CAN CUT THEM!

Le Bernank et Les Japanonais… not so much. They have chosen to put their countries in de penalty box for many, many, time – deh will ultimately sit dere now… and feel shame…

Or maybe they won’t feel shame. Your run of the mill central planning groupthinker from the Keynesian Kingdom tends to think they’ve saved us from all of the problems that they’ve created with ZIRPS (ZERO interest rate policies). Have you ever seen an academic “economist” win his or her Nobel prize and have a change of heart?

Not so much…

“We are now on a trajectory to add nearly 40% more population by the year 2050, raising our number to around 9.2 billion. Who will we be in 2050? In that year, for every one hundred of our future children and grandchildren born, fifty-seven will open their eyes in Asia and twenty-two in Africa, and mostly in cities.” (Smith, page 35)

A few important words in Smith’s depiction of the Global Macro Markets in which interconnected factors will continue to collide: “our number”, “our future”, and “open their eyes”…

Do we really think that conflicted, compromised, and constrained monetary policies that serve 5-10% of Western populations’ compensation desires (never mind 1% of our world’s) are going to hold their dogmatic line?

That’s a mega question that I’d love to see Le Bernank host a Global Presser Conference on and answer in Chinese and Rusky, with a straight face. Particularly after this morning’s Jobless Stagflation report, which will continue to remind the world that the Greenspan-Bernanke era of cutting savers account returns to ZERO percent has equated to a decade of ZERO net jobs created in America.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1527-1546, $98.11-102.29, and 1303-1324, respectively.

Best of luck out there today and enjoy the weekend,

KM

Keith R. McCullough

Chief Executive Officer