“Human behavior, not monetary behavior, is the key…”

-Warren Buffett (May 1977)

“And when very human politicians choose between the next election and the next generation, it’s clear what usually happens.”

That’s clear, Mr. Buffett. Crystal.

I wrote my senior thesis on Warren Buffett while I was banging away on a typewriter here in New Haven, CT almost 15 years ago. Time flies. But history’s lessons don’t.

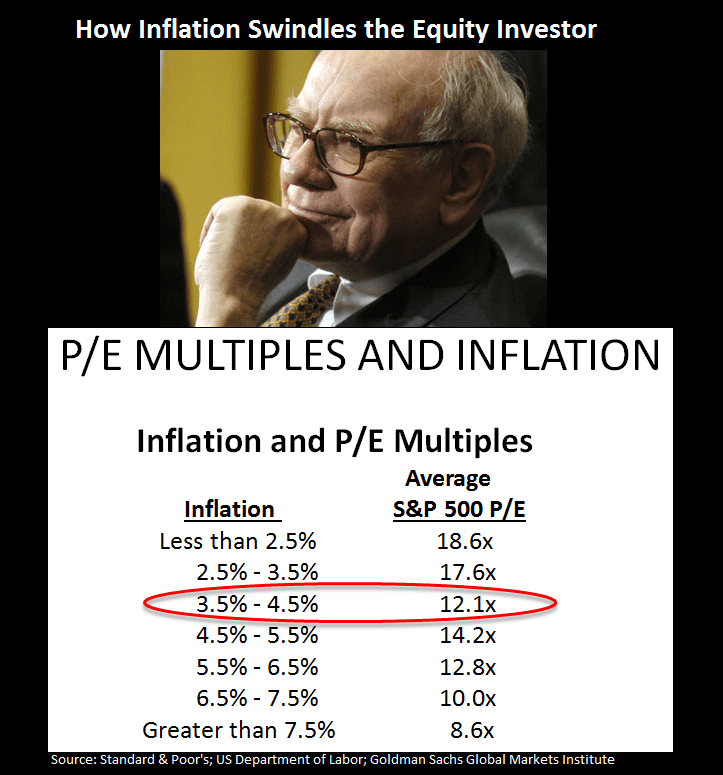

The aforementioned quotes come from a Fortune article Buffett wrote in May of 1977 titled “How Inflation Swindles The Equity Investor.” This was during the post Arthur Burns (last Fed Chief to attempt to monetize the US Debt) and Richard Nixon period, when Jimmy Carter promised to carry on the dual Fed/Presidential office mandate to attempt to inflate their way to prosperity.

The problem, of course, is that too much inflation slows growth… And Growth Slowing As Inflation Accelerates perpetuates The Jobless Stagflation… And the stock market pays a lower multiple for The Stagflation.

Back to our very human Keynesian politician …

Tonight, Le Bernank will be speaking in Atlanta where he’ll talk around A) cutting his GROWTH forecast and B) raising his INFLATION forecast (again, after the fact). While being a lagging indicator isn’t a new position for the Fed’s Chief, it’s important for Risk Managers to focus on Gaming His Almighty Policy. Across asset classes in the US, here’s how we think the market will respond:

- UST Bonds – Indefinitely Dovish (Q2 Macro Theme); upside in long-term bonds to 4.16% on the 30 year yield (immediate-term)

- US Stocks – Jobless Stagflation (1-1.5% GDP growth w/ 3.5% headline CPI; markets pay a lower multiple for The Stagflation)

- US Dollar – Indefinitely Dovish; should equate to further downside pressure in USD to 73.76 (a higher-low)

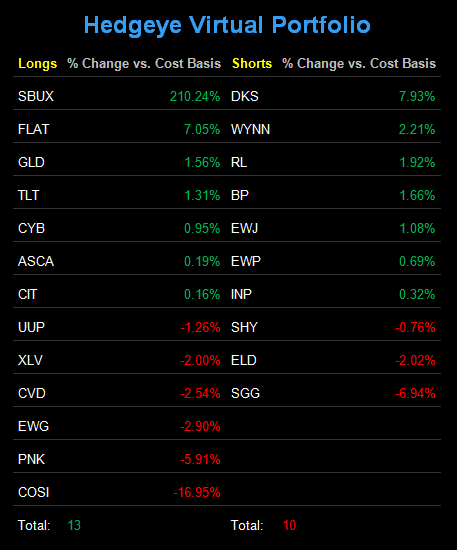

My lowest conviction Global Macro position is long USD into and out of this political pandering. I still like long-term bonds (TLT), UST Flattener (FLAT), and Gold (GLD).

On the short side, I covered some shorts yesterday and will look to re-short strength opportunistically today/tomorrow. So far, the best proxy product I can produce to express my risk management view of a traditional hedge fund’s NET EXPOSURE (longs minus shorts) is the LONGS minus SHORTS component of the Hedgeye Virtual Portfolio (chart below).

I know that’s not a perfect proxy, but I also know it’s a lot better than whatever the sell-side is still using to communicate their pre-2008 horse-and-buggy-whip research. With the SP500 being down now for 4 consecutive-days and 6 consecutive weeks, at Hedgeye we called yesterday a “short covering opportunity”, moving from net neutral in the Hedgeye Virtual Portfolio to 13 LONGS and 10 SHORTS.

That doesn’t make me wild and crazy long. It just means that I won’t lose an eyebrow as the machines fire up this morning’s S&P Futures. If you want to survive The Stagflation, you need to manage risk, real-time – and yes, that does include trading.

Managing risk (or trading) around the aforementioned Stock, Bond, and Currency market catalysts isn’t easy. Neither is attempting to justify being long the US Financials (XLF) with “valuation” as your backboard. Valuation isn’t a catalyst when stock prices are falling. The Financials (XLF) are down -13.1% since their YTD high on February 18th, 2011. “Cheap” stocks get cheaper.

In the same 1977 Fortune article, in asking Buffett “why does a man who is gloomy about stocks own so much stock?”… Buffett said: “Partly, it’s a habit…”

He’s partly human too. And “human behavior, not monetary behavior, is the key…”

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1, $98.46-102.47, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer