TODAY’S S&P 500 SET-UP - June 2, 2011

Nothing in the last week has changed our Global Macro risk management view.

- Growth is slowing

- Inflation (reported) is sticky

- Stagflation is bad for asset prices (commodities and equities in particular)

Growth Slowing is bullish for UST bonds (TLT) and Compression in the Yield Curve (FLAT). Those 2 positions remain Hedgeye’s highest conviction macro longs alongside Gold (GLD). Although, all 3 of them are getting overbought in the immediate-term. As we look at today’s set up for the S&P 500, the range is 18 points or -0.73% downside to 1305 and 0.64% upside to 1323.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1943 (-3520)

- VOLUME: NYSE 1189.94 (-21.46%)

- VIX: 18.30 +18.45% YTD PERFORMANCE: +3.10%

- SPX PUT/CALL RATIO: 2.19 from 1.61 (+35.79%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 21.22

- 3-MONTH T-BILL YIELD: 0.05%

- 10-Year: 2.96 from 3.05

- YIELD CURVE: 2.52 from 2.60

MACRO DATA POINTS:

- 8:30 a.m.: Jobless claims, est. 417k, prior 424k

- 8:30 a.m.: Nonfarm Productivity, 1Q final, est. 1.7% from 1.6%

- 9:45 a.m. Bloomberg consumer comfort, est. (-47.0), prior (-48.4)

- 10 a.m.: Factory orders, est. (-1.0%)

- 10:30 a.m.: Natural gas storage change, est. 93

- 11 a.m.: DOE Inventories

WHAT TO WATCH:

- Japan Prime Minister Naoto Kan survives no-confidence vote - Nikkei

- European bank stress test results to be delayed until July - WSJ

- Greece’s risk of default was raised to 50% by Moody’s as European officials rushed to put together the second bailout plan in two years to stave off renewed financial turmoil in the region.

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Billionaire Deripaska Joins Russia Grain Rush as Export Sales Ban Ends

- Rice Soaring 50% in Thailand as Thaksin Seeks Votes in World’s Top Shipper

- Wool Rallies to Highest Since 1995 as Flock Shrinks, Stockpile Replenished

- Drought in China’s Yangtze May Be Relieved by Rains, Helping Rice, Cotton

- Wheat Gains in Chicago on Speculation of Increased Livestock Feeder Demand

- Copper, Aluminum Drop as Weaker Data Drive Speculation Recovery May Falter

- Gold May Advance as Economic Slowdown, Greece’s Debt Turmoil Spur Demand

- Cooking Oil Imports May Climb as Indian Farmers Dump Soybeans for Cotton

- Japan Steel Works to Target Non-Atomic Energy Sales After Nuclear Disaster

- Rubber Declines to One-Week Low as U.S. Data Raises Concern Demand to Slow

- Oil Falls to Lowest in Week as Manufacturing Slows; U.S. Supplies Increase

- BHP Facing First Strike in 10 Years at World’s Biggest Steel Coal Supplier

- N.Z. Proposes Agency to Regulate Exploration, Mining in Its Offshore Zone

- Goldman, Major Banks See 55% Average Rise in Commodities Income, WSJ Says

CURRENCIES

EUROPEAN MARKETS

- Spain's treasury sells €2.75B of 2014 bond, bid-to-cover ratio 2.5 vs 1.8 at previous auction, bond average yield 4.037% vs 3.568% at previous auction

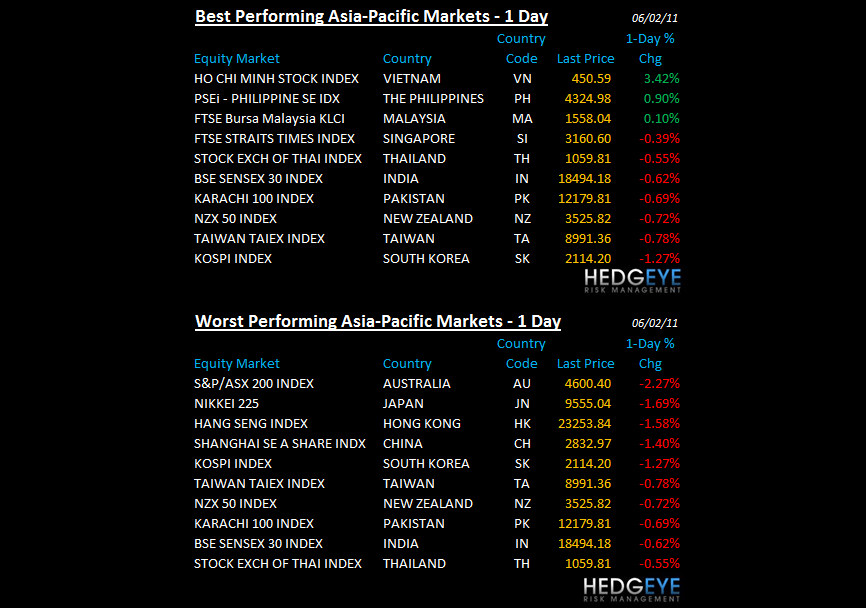

ASIAN MARKETS

- Indonesia was closed for Ascension Day.

- Will China raise rates over the weekend?

- Japan Q1 manufacturing capex +27.7% y/y, corporate capex +3.3% y/y. Monetary base +16.2% y/y vs +23.9% seq.

- Australia April trade surplus A$1.60 vs A$1.69B seq. April retail sales +1.1% m/m vs revised (0.3%) seq

MIDDLE EAST

Howard Penney

Managing Director