Positions in Europe: Long Germany (EWG); Short Spain (EWP)

As we’ve been calling out in our European work, headline risk has been hot and heavy in recent weeks in European capital markets as European leaders and market participants sift through solutions for and the implications of Greece’s fiscal imbalances. Comments yesterday from Eurogroup head Jean-Claude Juncker that a total restructuring of Greece’s debt is out of the question and that EU leaders will decide on a new aid package for Greece by the end of June bulled up equity markets today (Greece’s Athex closed up +6%), boosted the EUR-USD, and depressed peripheral bond yields and CDS spreads (see charts below).

We remain grounded in our position that EU officials will continue to socialize the region’s fiscal ills in order to preserve the Eurozone, support the common currency, and limit cross-country banking exposure losses by granting additional bailout packages and potentially moderating the yield and/or maturity demanded on debt repayments to the bailout facilities by the periphery, a form of “soft” restructuring.

In any case, while we think that these support measures and subsidies could potentially bolster European markets and the common currency over the near to intermediate term, longer term fiscal health will not be attained unless a country like Greece is allowed to default and other peripherals are forced to adhere to their deficit reduction targets without concessions.

For now, given that EU leadership is content with a policy on debt of Extend and Pretend, our models suggest the EUR-USD has an immediate term TRADE range of $1.41-1.44, with a significant intermediate term TREND support level at $1.41. Should $1.41 break, we see a roughly 4% downside to $1.35 (See chart below).

Given Juncker’s statements yesterday and announcements last week from the Greek government of a fifth austerity package, including selling €50 billion of state assets over the next 3 years to help pay down its bloated deficit, the region could see mild respite over the next days and weeks. However, we caution on the precarious nature of headline risk. Just late last week Juncker was insinuating that Greece may not receive the IMF’s next bailout tranche, which sent markets tumbling!

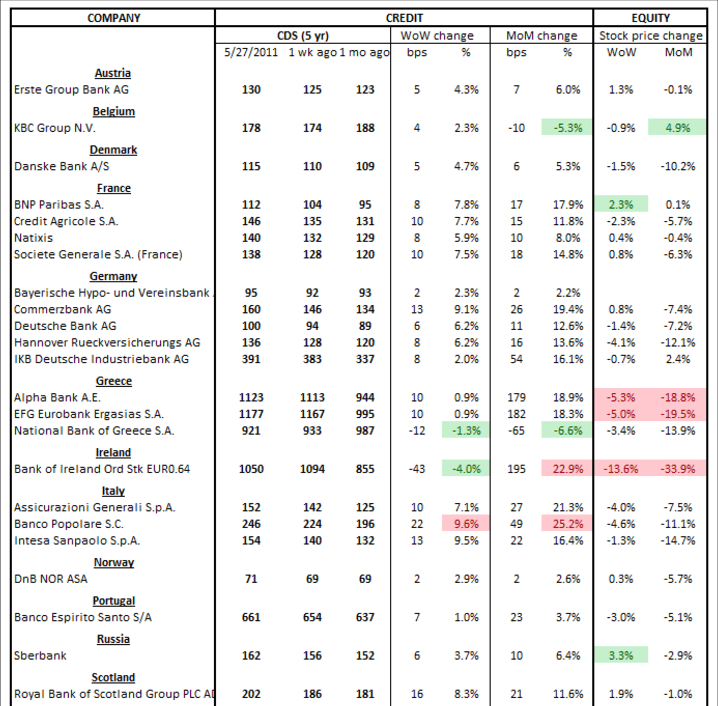

As is typical for the start of the week, below we show our European Financials CDS Monitor. It shows that bank swaps in Europe widened for 34 of the 38 banks monitored week-over-week, while 4 tightened (see below). No big surprises here.

We’re currently short Spain via the etf EWP and long Germany (EWG) in the Hedgeye Virtual Portfolio. Spain’s fundamentals continue to be overshadowed by political uncertainty (Zapatero’s party lost major support in recent elections), ragingly high unemployment (20.7%), the persistent slide in housing prices, and in our assessment a high probability that Spain misses its deficit reduction target, which currently stands at 9.3% of GDP.

On the margin, and despite positive data out of Germany today (Retail Sales +3.6% in April Y/Y and Unemployment down 10bps to 7.0%), we're less bullish on Germany as the high frequency data has slowed in recent months and the Euro region remains mired in sovereign debt contagion.

Be vigil or steer clear,

Matthew Hedrick

Analyst