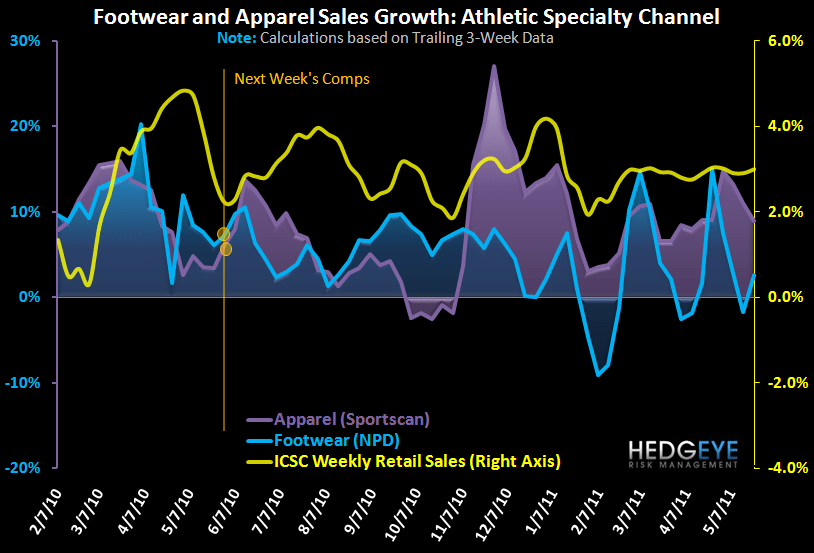

Athletic apparel sales remain healthy posting a sequential acceleration in the athletic specialty channel while footwear slowed. Volatility remains high in footwear consistent with recent weeks. However, in taking a closer look at footwear ASPs it’s important to keep in mind just how disruptive toning has been and how significantly it can mask underlying core trends. Take a look at the first two charts below. The recent weakness in footwear ASPs is almost as noteworthy as the strength we’re seeing in apparel. Yet, when we strip out the dilutive impact of toning ASPs, core athletic footwear trends reflect not only solid low-to-mid single digit growth, but on a more consistent basis than apparel. Additionally, it’s worth highlighting that toning has represented a 4%-5% drag on core athletic footwear sales growth on average YTD. Back to callouts from the week:

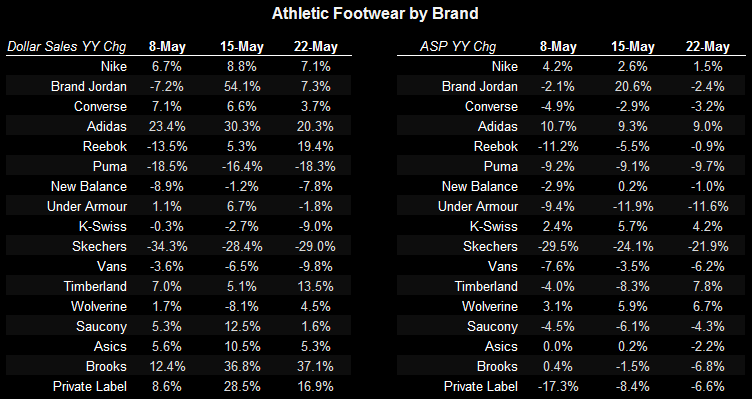

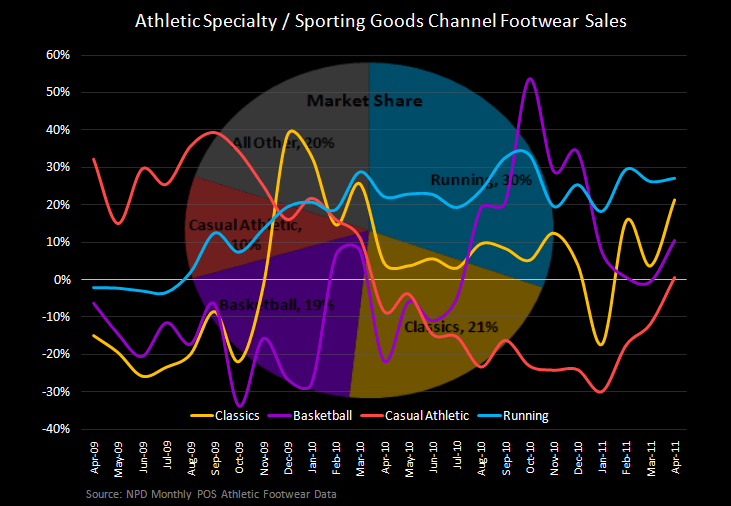

- In footwear, running continues to be a pocket of strength lead by Brooks up +37% followed by Adidas up +20% due to the new Climacool introduction and Reebok up +19% reflecting the introductions of Zig Pulse and RealFlex. Nike and Adi remain the top share gainers at the expense of Skechers, Puma, and New Balance. This is consistent with monthly trends that reflect running is not only the largest, but also fastest growing category within the athletic specialty channel for the fourth month in a row.

- In apparel, VF (The North Face) (+30%) edged out Adidas (+28%) as the top performing brand last week reflecting an uncharacteristically strong week in outdoor outerwear perhaps due to more inclement weather. In addition, Under Armour (+20%) continues to post consistently solid sales driven by the success of its charged cotton program. Adidas and Under Armour remain top share gainers while Columbia was the only brand to lose share maintaining a streak of twenty consecutive weeks.

- The broad-based strength across all channels is also worth noting with both unit volume and ASPs up and sequential sales improvement across the board.

- Lastly, on a regional basis New England was the clear negative standout as the only region to report a sales decline for the second consecutive week with the Mid-Atlantic and South Central outperforming again up +23% and +28% respectively – not good for DKS (which we’re short in the Hedgeye Virtual Portfolio) and better on the margin for HIBB.

Casey Flavin

Director