“Governments everywhere are still trying to cure by public works the unemployment brought about by their own policies.”

-Henry Hazlitt (Economics In One Lesson, page 208)

I suppose it’s only fitting that Henry Hazlitt revised his million-plus copies sold of “Economics In One Lesson” in June of 1978 (originally penned in 1946). That’s when the Western world was swallowing stagflation whole. That was shortly after the French introduced the G-Fluff.

G-Fluff, formerly known as the G-6 Central Planning Board (created by France in 1975), is now affectionately referred to by professional politicians as the G-8.

The G stands for Groupthink. The G-8 currently consists of Canada, France, Germany, Italy, Japan, Russia, United Kingdom, and the United States. Not to be outdone, The EU also sends their commissioners for 3 hour lunches that serve up piping hot bs, with broccoli.

This year’s G-Fluff conference is being held in a hoity-toity town on the northwestern coastline de la belle Provence. Les Obamas et les Sarkozys (hearing there may be more than a few of them – with adjoining rooms)… La rencontre… et la culture… sans le DSK.

BREAKING HEADLINE (out of the G-8 conference this morning):

“THE GLOBAL RECOVERY IS GAINING STRENGTH… HOWEVER, DOWNSIDE RISKS REMAIN”

Mais, qu’est-ce que c’est Le Recovery? Que’est-ce qui se passe avec Le Downside?

(Before someone goes all French socialist on me – for the record, my Mom’s side of the family is French-Canadian, and I went to French school until the 5th grade, learning how to read, write, and count in French before the English pig stuff.)

Back to Le Recovery et Le Downside…

In Spain the socialists are running a 21.3% unemployment rate, so let’s not talk about that outcome of le debt financing les deficits – Spain isn’t allowed at the G-Fluff conference anyway.

Let’s talk about le USA.

- Yesterdays US jobless claims report rose 15,000 week-over-week to 424,000

- Ze rolling claim (the 4-week moving average) held at 439,000 – a new YTD high!

When considered on 1 of the 2 key measures of le success of Le Bernank (1. Full Employment, 2. Price stability), this is not good. Actually, it’s really bad – because our math suggests that for the unemployment rate in this country to recover, we’ll need to see weekly jobless claims consistently below 385,000.

Le Bernank et L’Obama get this. That’s why Le Bernank’s key statement less than a month ago at his Presser was:

“It’s not clear that we can get substantial improvements in payrolls without some additional inflation risk.”

-Ben Bernanke, April 27, 2011

In other words, without Le Quantitative Guessing (and ze Inflation born out of it) – we do not know what to do.

May I suggest two eggs, side by each, pour ton fluffy dejeuner Madame Obama?

This entire Keynesian experiment and my mockery of it is a much more serious joke than I can muster this morning. For the last 6 months Hedgeye has been warning that a policy to inflate will structurally impair (slow) economic growth.

I’m actually getting tired of hammering my hockey knuckles into my keyboard every morning – as de French-Canadian goalie from “Slapshot”, Dennis Lemieux, might say – SLOW-z… SLOW-zzz – de Inflation slow-ZZZ de growth!

Back to the Global Macro Grind…

The US Treasury Bond market is busting a move to the upside again this morning. US Treasury Bond yields are getting crushed. The 2-year is trading at 0.48% and 10’s are testing a breakdown of the 3% line. The Yield Spread (2-year yields minus 10’s) continues to compress (+258 basis points wide, down another 6 basis points week-over-week).

What does this mean?

- Growth expectations are slowing

- Inflation expectations are slowing

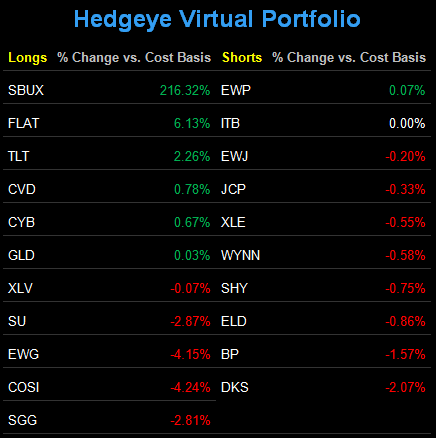

We call this Deflating The Inflation (Hedgeye Q2 Macro Theme), and we can send you the 50 page slide deck on how it works. The two long positions we have on to reflect this view are bullish on the long-end of the bond market (TLT) and long a US Treasury Flattener (FLAT).

Yes, we are aware that Le Bernank has to end le QG2 in 6 weeks. We are also aware that when this unprecedented Keynesian experiment ends, jobless claims in America could go a lot higher. I don’t have to wonder what Henry Hazlitt would say about that in June 2011.

My immediate-term ranges of support and resistance for Gold, Oil, and the SP500 are now $1511-1538, $96.89-101.57, and 1, respectively.

Have a great Memorial Day weekend. God Bless America. And best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer