Positions in Europe: Long Germany (EWG); Sweden (EWD)

All eyes are back on Greece on the backdrop of increased European credit and political uncertainty over the last week. As we continue to press, piling debt upon debt doesn’t end well – now the question remains the timing and form of a Greek debt default, restructuring, or some combination or hybrid of the two. Last week Jean-Claude Juncker candy-coated the issue and called for a possible “re-profiling” of Greek debt. What’s apparent is that EU officials will continue to extend & pretend, by delaying and/or re-allocating funds over the near to intermediate term to make concessions for Greece’s fiscal shortfalls. This should ultimately add support in the EUR-USD trade (around $1.40), but by no means reduce volatility in the pair.

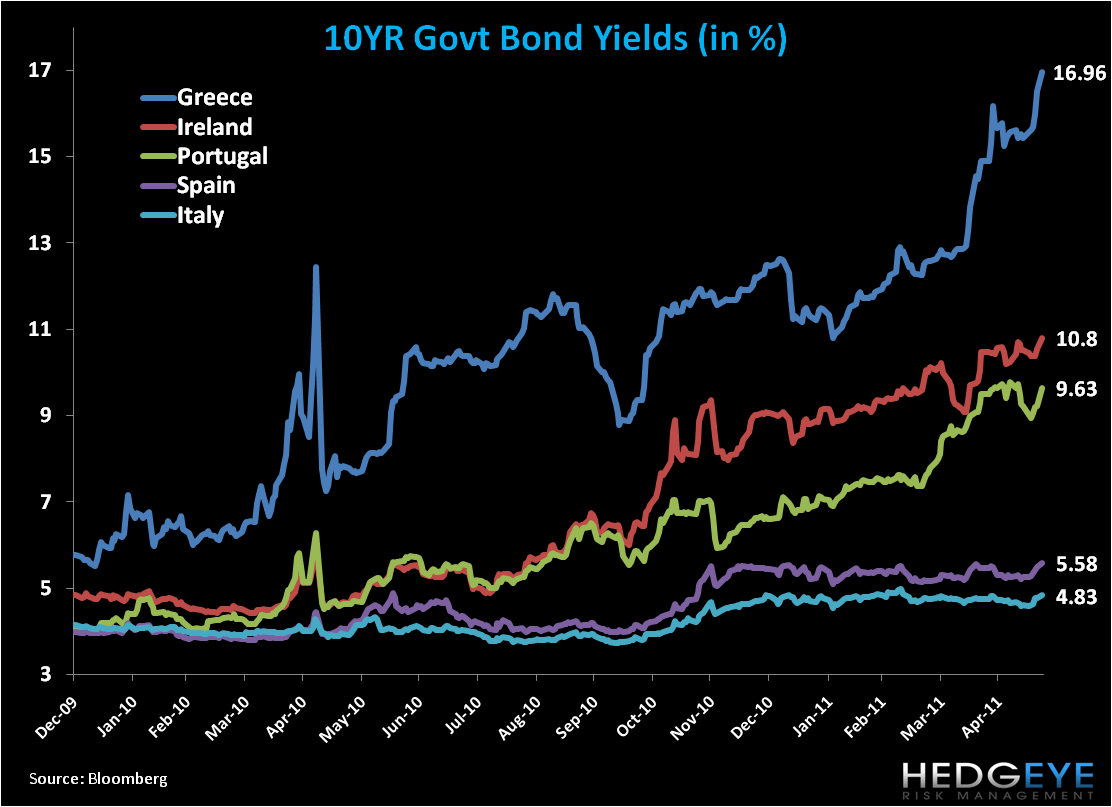

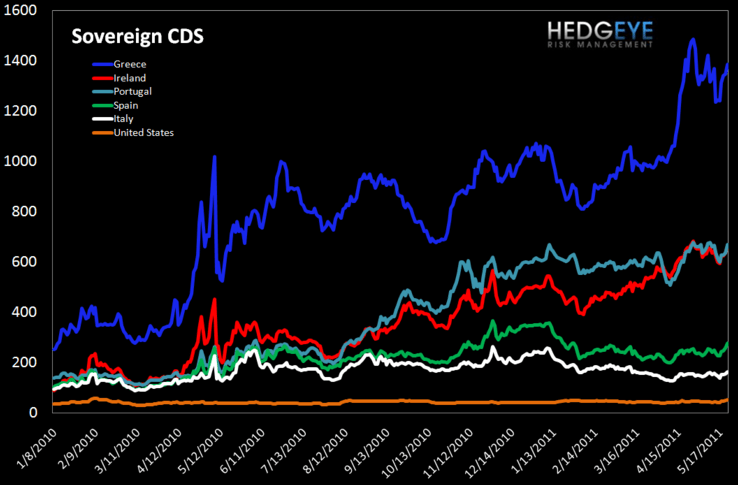

Through increased pressure from EU officials, the Greek government is meeting this week to discuss a fifth austerity package, with plans to sell €50 billion of state assets to help pay down its bloated deficit. The headline risk associated with the talks continues to punish the capital markets of Greece and the rest of the periphery. Last week the Greek Athex (equity) was down -4.3%, and is down a full -25% since its ytd high in mid February. This morning we see yields of 10YR bonds from the PIIGS jumping, with Greece rising a full 44bps to just short of 17%, while Portugal rose 41bps to 9.63%! A similar trend is seen with sovereign CDS, and the question remains just how much more likely a default of Greece is with CDS in the area code of 1400bps versus say 1300bps? After all, Lehman Brothers blew up around 600bps (see charts below).

Of the news and data causing consternation this morning (European equity indices are down 150-300 bps today):

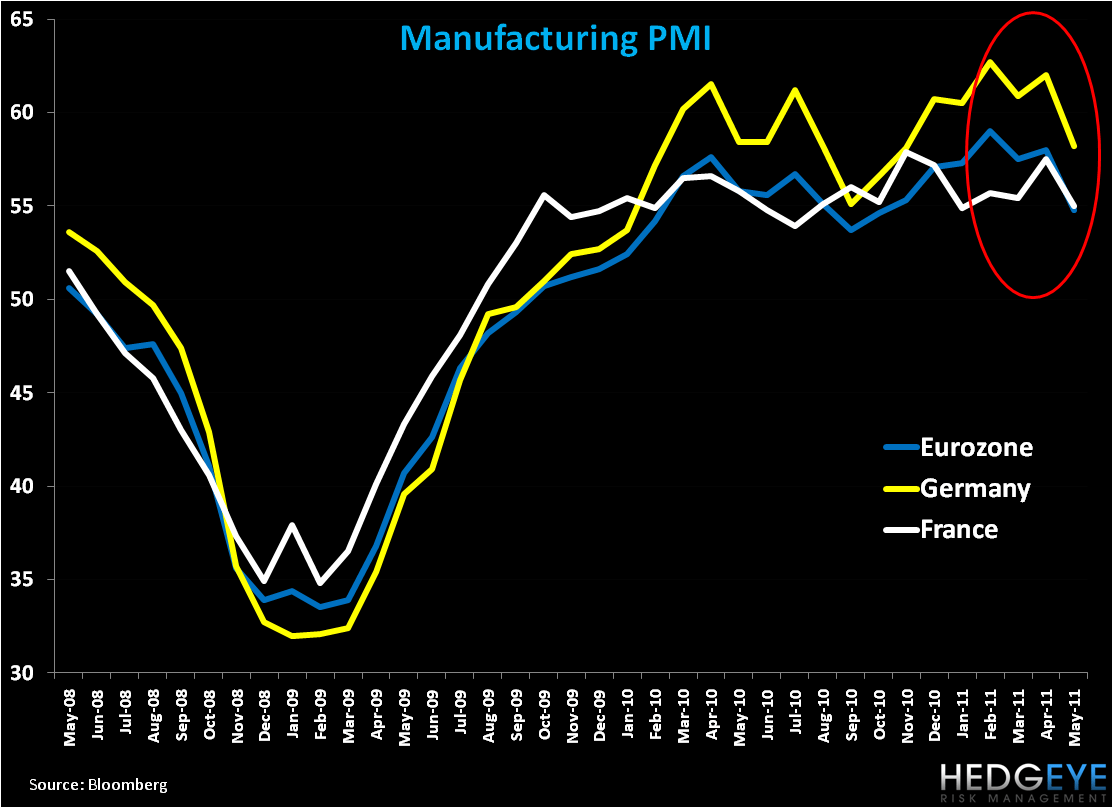

1.) Preliminary Services and Manufacturing PMI for May out for the Eurozone, Germany, and France, all fell considerably month-over-month (see chart below). As we’ve been highlighting over recent months, we’ve seen pockets of high frequency data slowing from the region’s largest countries. We remain bullish on Germany (currently in the Hedgeye Virtual Portfolio), but cautious as we monitor the data. Certainly Germany has not been immune to inflation (CPI stands at 2.4% Y/Y), however readings continue to come in under the EU average, and significantly below UK CPI at 4.5%.

2.) Standard & Poor’s revised Italy’s credit-rating outlook to negative from stable, citing the nation’s slowing economic growth and diminished prospects for reducing government debt. If you’ve been following our work you’d know we’ve taken this tact for months on Italy (and also Spain). S&P affirmed Italy’s A+ long-term rating.

3.) PM Jose Zapatero’s Socialist Party suffered a huge blow in state and municipal elections of the weekend, as expected. The opposition center-right Popular Party took share in virtually all 13 regional governments that were up for grabs. Zapatero conceded the defeat but ruled out early elections. The political fragility of his party’s rule make it all the more unlikely that the country will be able to pass further austerity measures to limit the budget deficit (9.3% of GDP). The protests being called on the streets over unemployment should remain a permanent fixture, as a coherent strategy for growth and reduction in joblessness is nonexistent.

4.) German Chancellor Angela Merkel’s Christian Democratic Union Party (CDU) suffered a blow in a state election in Bremen over the weekend. Voters re-elected the Social Democrats (SPD) with 38% approval, followed by the Green Party at 23%. Merkel’s CDU fell 5pp from last election to 20%. The set-back follows two other defeats in state election ytd (Hamburg and Baden-Wuerttemberg), and highlights the cracks forming in Merkel’s foundation. Importantly, voting shows Merkel’s popularity continues to be punished based on her flip-flop on nuclear power following Fukushima.

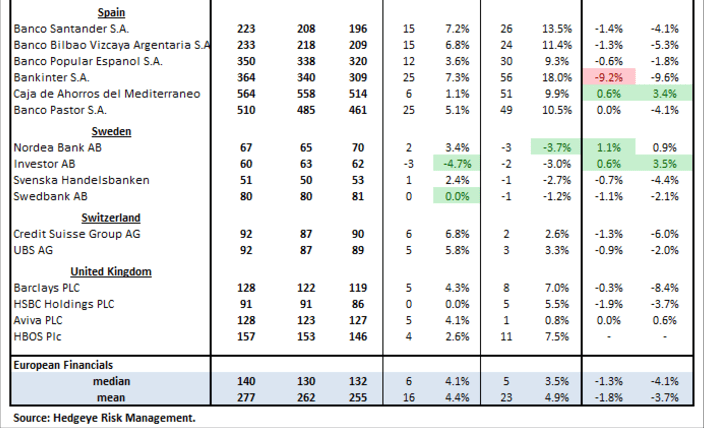

Our European Financial CDS Monitor shows that bank swaps in Europe widened last week, with 36 of the 38 swaps wider and only two tighter. A major inflection, as expected, was Greek banks.

We’ll get a number of confidence readings from Europe this week as well as second revisions of Q1 GDP. Today we added Sweden via the etf EWD on the long side to the Hedgeye Virtual Portfolio. Sweden remains a fiscally sober country (like Germany) with a strong growth profile of 4.5% this year. So long as the country continues to see demand for its goods from the EU, we like the country’s outlook given the Riksbank proactive rate hikes to head off inflation.

Matthew Hedrick

Analyst