Bumping our estimate up to HK$23-24BN for May

In the first week that includes Galaxy Macau, the market generated HK$775 million in gross table revenues per day, up from HK$528 last week and HK$640 million YTD. It’s too early to determine how much Galaxy has grown the market since we only have one week of data and don’t know what the hold percentage was. Given the strong opening of Galaxy, we are increasing the bottom end of our projection range for the full month of May from HK$22 billion to HK$23 billion and are now estimating a range of HK$23-24 billion.

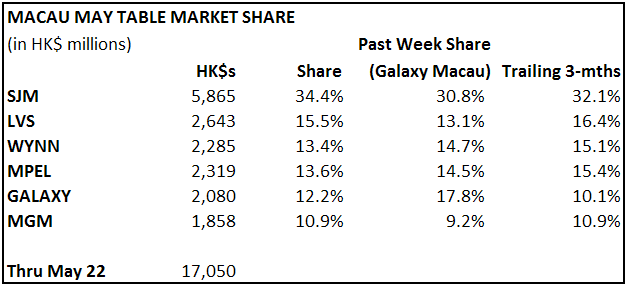

The opening of Galaxy Macau clearly had a positive impact on Galaxy’s overall market share. The company garnered 17.8% share in the past week, pushing Galaxy’s full share to 12.2% for May to date, versus a trailing 3 month share of 10.1%. The big market share loser in the past week was LVS, losing 330bps from its trailing share. Surprisingly, MPEL only lost 90bps following the opening of Galaxy despite being generally considered the biggest loser to the new property. MPEL’s share actually recovered a bit from last week’s month to date 13.2%, which was hurt by low hold, despite the opening of Galaxy.

The figures through May 22 are shown below:

The following table compares this past week’s average table revenue per day to the average for the past three months by property. Interestingly, despite the impact of Galaxy Macau, every company generated higher revenue per day post-Galaxy than pre-Galaxy, except for LVS. On limited data, it appears Galaxy has grown the market. The one caveat here is that we have heard that Galaxy has offered a lot of junket credit in conjunction with the opening and some of the other players may have followed suit. This may not be sustainable.