We’ve spoken ad-nauseam about how the spread between supply and demand would start to buckle in May/June and take margins lower. Gap pretty much confirmed this last night. The call from here, however, is not on Gap. But it’s to press the JC Penney short. On the flip side, we’re changing our tune, and are getting positive on Target after being bearish there all year. This is the TREND and TAIL call. And as always, Keith will manage the TRADE.

The fact that we’re already seeing some people come out and defend their perma-faves by saying that the GPS blow-up is ‘company-specific’ is just flat out intellectually irresponsible. We weren’t shocked by the magnitude of this miss by any means – as outlined in our “4.5 Below” thematic piece from earlier this year where we quantified a 4.5 point margin hit for the industry – and don’t necessarily think it will be the last for GPS. Fortunately, they have the good grace of Eddie Lampert to financial engineer their way out of the worst operating environment in decades.

We’re not making a call on Gap here.

We think that there’s much more money to be made in shorting JC Penney, and (gasp!) going long Target. What?!? We can hear the feedback already…”You guys have been so negative on Target all year, and you turn positive just as the industry thesis is starting to work?”

The short answer is ‘Yes’ and for very good reason.

TARGET

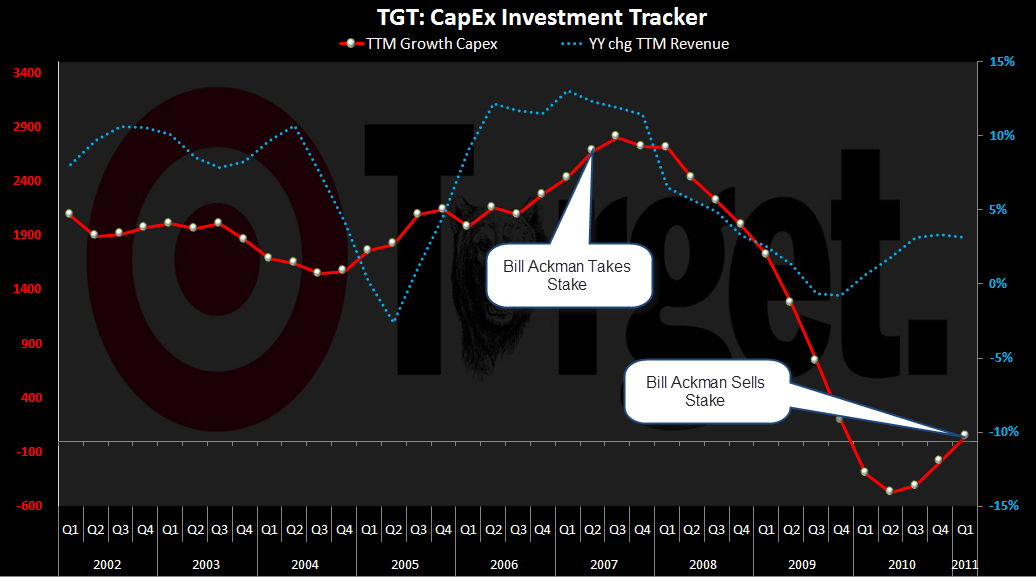

We hate to point to Ackman as being the main factor – but the reality is that it is the fallout/windfall that we expect to see at JCP/TGT, respectively as the heavy hand of activism spanks the other cheek will create opportunity for real investors to make money here. We didn’t believe in the half-baked financial engineering story with Target in 2008, and we certainly won’t believe it now that Ackman has blown out of his TGT and shifted his focus to JCP.

One consideration here is that Target is actually a solid company. The concept is a winner, management is proven, it has square footage growth ahead, and has the benefit of the incremental shift towards its Membership Rewards model and P-Fresh rollout. More loyal customers and more consumables = more traffic.

While that’s all fine and good, our prior problem with it dates back to that fateful turn of events that started in 4Q07 when Ackman started his ‘assault’ in ultimately owning 3.55% of the company by the end of 2009. The proxy battle begins!

Then on Target’s May 7 sales release in 2009, comps were in-line, but more importantly TGT noted that tight expense controls and better gross margins will lead EPS to be “well above estimates". Credit quality also came in line vs. a trend of coming in slightly below plans. Then, four days later, TGT issued a press release titled “Questions That Attendees May Want To Ask At The Pershing Town Hall.’ In other words, TGT started to pull out all the stops to make Billy go away. Ultimately, Billy took it on the chin, and lost his proxy battle on May 28 of 2009 after it was clear that the momentum of the business was going against him.

The ‘strong cost control’ is particularly notable to us. Being cost-conscious is something most great companies have embedded in their DNA. But this is a company that has added $1.5bn in revenue (2.5% over 2 years) since The Ackman Assault, but has held SG&A dead even. And yes, that’s despite 9.5% square footage growth over that same period. Last we checked, a new store requires a few bucks.

Similarly, let’s look at capex. TGT had its precipitous decline in capex over that same exact time period. Any way you cut it, relative to prior trends, growth capex was cut by over a half such that total capex actually ran below D&A for three quarters.

Now it’s clearly headed higher. So at the same time the activist thorn in TGT’s side is removed, it starts to behave rationally again and invest to reaccelerate share gain. One thing we’ll give TGT credit for is being good stewards of capital – at least when they don’t have an activist dog barking in their ear.

We’re still concerned with near-term earnings quality (i.e. credit accounting for an outsized portion of the latest qtr eps) and will be watching that accordingly. But ultimately, our issue with TGT had been that lack of reinvestment around all this noise would preclude the company from hitting both sales AND margin goals. We’d give ‘em one or the other. But not both. That call has proven to be the right one.

Now, we’re approaching a point where the lag from TGT’s reinvestment and revenue growth has caught up. We think that numbers have stopped going down, and we’ll see a reacceleration in top line over the next 12 months.

JC PENNEY

In nearly every way that Target is a good company, JC Penney is not. It has a poor legacy real estate profile, over-exposure to apparel (in the worst apparel environment in decades), and over 50% private label/exclusive mid-tier brands that most consumers would not notice if they simply went away. One of the keys there is that JCP’s more vertical model relative to most other department stores (where it sources directly in Asia) means that it has fewer touch points between manufacturing and final retail sale to share cost pressures with partners. In times of excessive stress, JCP bears the pain.

On the flip side, to be fair, it also garners the upside as the environment improves. But in this space, the soonest we’ll see that will be 2013.

Keep in mind that when we see events like Gap missing plan/blowing up, this has a ripple effect. Was Gap planning on this? No. Nor were their vendors, the competitor down the hall in the mall that sells similar product, etc… this is where the chain reaction begins. JC Penney does not have a whole lot to stand on. Liz Claiborne might be great – but is really just a splash in the bucket for JCP (it’s much more meaningful for LIZ). Also keep in mind that JCP has been serially in and out of restructuring mode for the past decade. The ‘low hanging fruit’ has been largely picked.

As was the case with Target, we think that the diversion of management’s attention – especially at a time when industry and Macro factors will demand it most – will also hurt on the margin.

Our industry call all along had been that we’d start to see the dominoes fall relative to expectations in May/June – and we’re sticking to our guns. We do not – by any means – think that GPS is one-off. It is just the beginning.