TODAY’S S&P 500 SET-UP - May 17 2011

As we look at today’s set up for the S&P 500, the range is 9 points or -0.19% downside to 1327 and 0.49% upside to 1336.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1607 (+252)

- VOLUME: NYSE 907.30 (+0.99%)

- VIX: 18.24 +6.85% YTD PERFORMANCE: +2.76%

- SPX PUT/CALL RATIO: 1.88 from 1.81 (+3.76%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 24.02

- 3-MONTH T-BILL YIELD: 0.04% +0.01%

- 10-Year: 3.15 from 3.18

- YIELD CURVE: 2.61 from 2.61

MACRO DATA POINTS:

- 8:30 a.m.: Housing starts, est. 569k, up 3.6%; prior 549k, up 0.8%

- 8:30 a.m.: Building permits, est. 590k, up 0.9%, prior 594k, up 11.2%

- 9:15 a.m.: Industrial production, up 0.4%, prior up 0.8%

- 9:15 a.m.: Capacity utilization, est. 77.6%, prior 77.4%

- 11:30 a.m.: U.S. to sell $28b in 4-week bills

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- WSJ notes that Department of Justice is stepping up its merger opposition

- Luxembourg PM Jean-Claude Juncker raises issue of 'reprofiling' of Greek debt for first time - Bloomberg

- Goldman, BofA and Morgan Stanley to meet with N.Y. Attorney General Eric Schneiderman as part of an investigation into mortgage securitization

- Greece may delay payments under EU proposal to extend $156 bailout

- International finance ministers discuss IMF managing director successorship after Strauss-Kahn arrest

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Global Food Prices Extending Gains Set to Raise Costs for Tyson, Kellogg

- Crude Recovers in New York as European Ministers Endorse Aid to Portugal

- Copper Rises for Fourth Day Before U.S. Housing-Starts, Production Reports

- Gold Climbs as Physical Purchases, European Debt Concern Increase Demand

- Corn Advances for Fourth Day as Wet Weather Delays Spring Planting in U.S.

- Sugar Rises for Fourth Day on Speculation Surplus May Shrink; Coffee Gains

- Wheat Damage Claims on Dry Weather May Signal Worse Harvest Than Forecast

- Mississippi River Diversion Greatly Reduces Threat to Cities, Refineries

- Cotton Moving Average Signals 21% Drop, Infinity Says: Technical Analysis

- Soros Sheds Gold ETPs as Paulson Keeps Bet on Bullion Extending Record Run

- Xstrata Record Profit Seen as Coal Cargoes Gain Amid Rout: Freight Markets

- Petrobras Yield Gap Over Sovereign Debt Is a Buy Indication: Brazil Credit

- Fonterra’s New Zealand Milk Production May Reach Record After Mild Autumn

- Australia Canola Output May Reach Decade High, Matching Record, Group Says

CURRENCIES

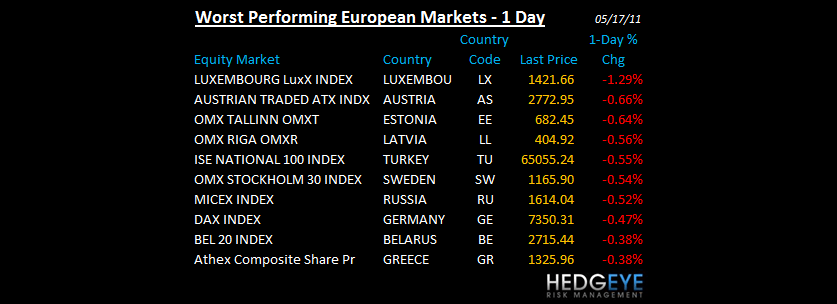

EUROPEAN MARKETS

- European equity markets trade mixed to lower

- Germany May ZEW 91.5 vs consensus 87.5 and prior 87.1; Germany May ZEW economic sentiment +3.1 vs consensus +5.0 and prior +7.6

- UK Apr RPI +5.2% y/y vs consensus +5.2% and prior +5.3%; UK Apr RPI +0.8% m/m vs consensus +0.8% and prior +0.5%

- UK Apr CPI +4.5% y/y vs consensus +4.2% and prior +4.0%; UK Apr CPI +1.0% m/m vs consensus +0.7% and prior +0.3%

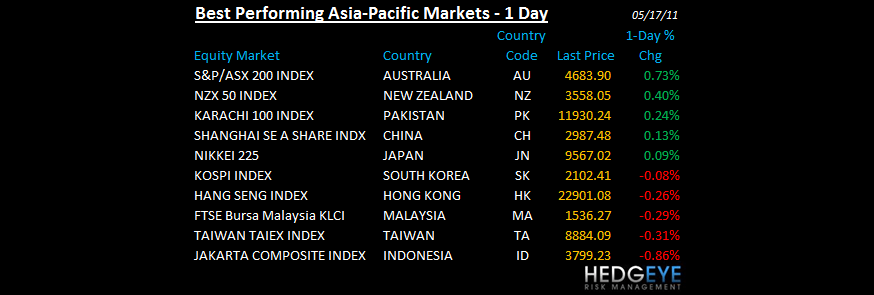

ASIAN MARKETS

- Thailand was closed for Visakha Bucha Day

- Singapore was closed for Vesak Day

- Indonesia was closed for Waisak.

- Asian markets were mixed to unchanged on the day.

MIDDLE EAST

Howard Penney

Managing Director