Positions in Europe: Long Germany (EWG)

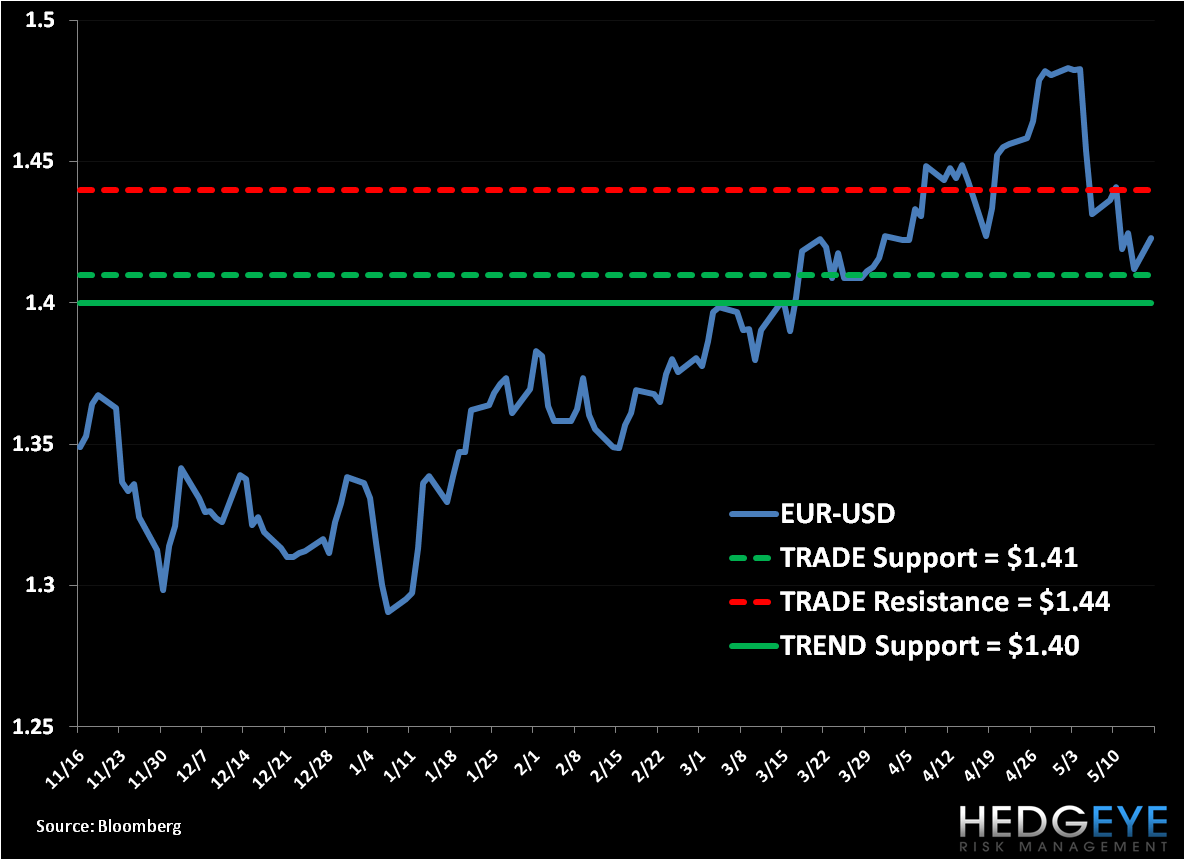

A court today denied IMF head Dominique Strauss-Kahn bail and remanded that he be placed in custody until the next grand jury hearing on May 20th under claims he sexually assaulted a chamber maid in a Manhattan hotel room over the weekend. The IMF preempted the court’s decision and replaced Strauss-Kahn with first deputy John Lipsky as acting Managing Director yesterday; however, the timing of the incident collides with the beginning of two day meetings of Eurozone finance ministers to discuss additional funding for Greece and existing loan terms for Ireland and Portugal. With the IMF funding around one-third of European bailout packages, the departure of Strauss-Kahn creates near-term consternation as the region’s periphery remains mired in sovereign debt contagion. We expect the EUR-USD to trade in a band of $1.41 to $1.44 over the immediate term TRADE, and maintain a support level around $1.40 over the intermediate term TREND as the European community continues to fiscally backstop the Eurozone (see chart below).

The EUR-USD declined -1.4% week-over-week in a week that showed increasing inflation readings and strong Q1 GDP reports versus expectations, particular in Germany and France, gaining 1.5% and 1.0% quarter-over-quarter, respectively. However, the common currency remains volatility against a backdrop of headline risk, including current negotiations that hint Greece could receive another €60 Billion on top of the €110 Billion bailout issued in May 2010. Our stance remains that kicking the can of debt down the road doesn’t end well, however that won’t spell decimation for the common currency over the near to intermediate term.

A few near-term catalysts to keep on your screen as it relates to the EUR-USD pair that may influence its movement within a band include:

- Any decision, if any, on additional Greek funding from the Eurozone finance ministers’ meeting beginning today

- State elections in Spain on May 22nd that could jeopardize PM Zapatero’s power

- The ongoing US debt ceiling debate (May 16 until the end of June = White hot political calendar for USD)

Our European Risk Monitors continue to reflect a significant risk premium to own Europe’s periphery, however risk has largely abated over the last week. Greek 10 year bond yields are hovering around 15.5%, and gained 14bps day-over-day, however sovereign Greek CDS backed off 165bps w/w (see chart below). Further, risk continued to fall into the announcement of Portugal’s €78 Billion bailout package and recent confirmation that the Finns will acquiesce to the bailout terms. The 10YR Portuguese government bond yield fell 74bps w/w.

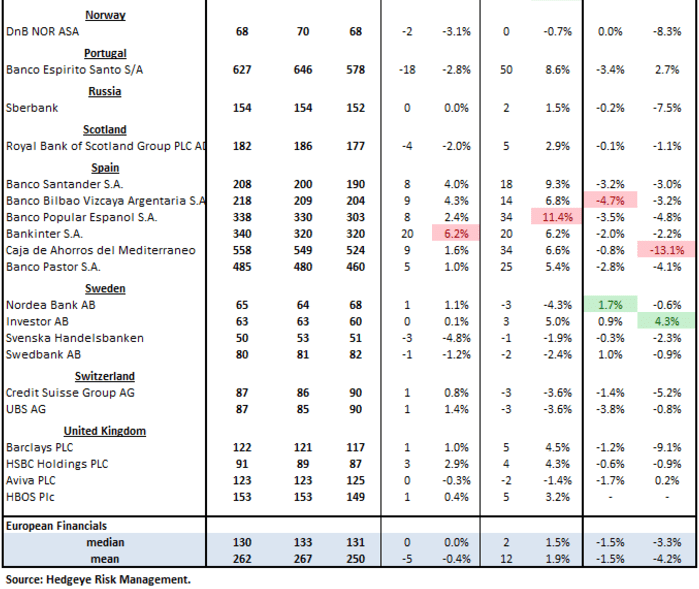

Our European Financials CDS Monitor shows that bank swaps in Europe were evenly split last week, widening for 19 of the 39 reference entities and tightening for 19, with one flat.

Strauss-Kahn’s ruling will also impact French politics, as he was expected to announce his presidential candidacy under the Socialist Party at the end of the month. Going into this weekend, Strauss-Kahn was the most popular candidate to challenge Sarkozy into April/May 2012 presidential elections, with approval polls suggesting he led Sarkozy by as much as 5%.

We remain constructive on German fundamentals and expect the country to lead the region. We’re long Germany in the Hedgeye Virtual Portfolio via the etf EWG and believe the country’s fiscal conservatism leaves it in a strong defensive position as sovereign debt contagion within the region persists. Over the last days we’ve seen Greece and Spain break their TRADE and TREND lines, with the UK’s FTSE breaking its TRADE and TREND lines just today. Our models show TREND support for the FTSE at 5,953 and TREND support for the DAX at 7,100. Stay tuned.

Matthew Hedrick

Analyst