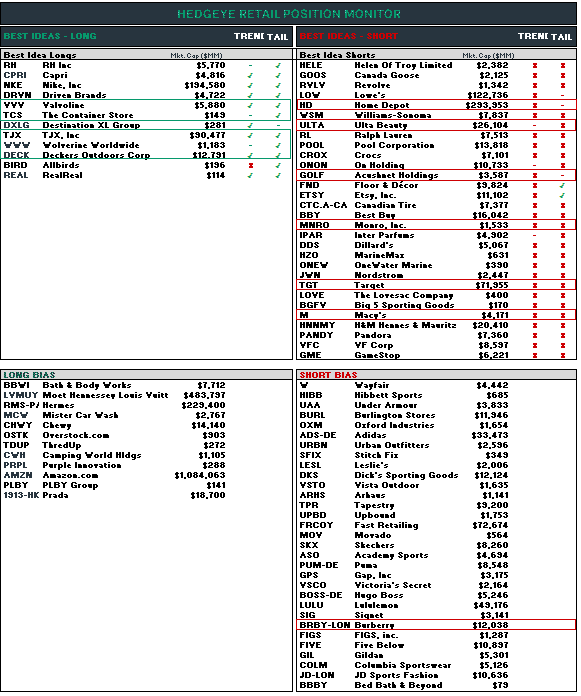

We’re hosting our weekly “The Retail Show” tomorrow, Monday at 11am. We’ll ‘speed date’ through our Position Monitor changes, upcoming earnings for the week, and any other questions that viewers (including you) put into the queue. Live Video Link CLICK HERE

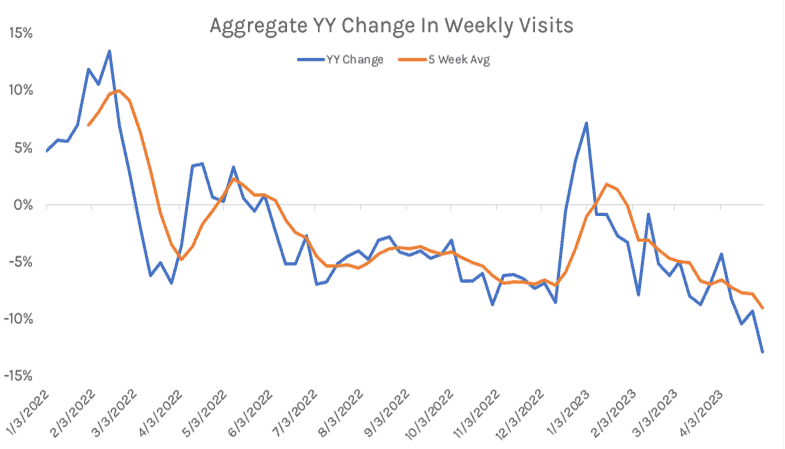

Mind the Exit Rate in EPS Guides…This week kicks off 1Q Retail earnings season with several bellwethers reporting. Keep in mind that these companies will be giving guidance while experiencing meaningfully deteriorating comp exit rates in recent weeks. Traffic is hitting new lows – even for winners like ULTA (Best Idea Short) – while sales trends are coming in anemic at just over 1% (Redbook). Mind you that includes grocery, which is up mid-high single digits, while we’re arguably seeing unit demand down 5-10% in consumer goods (inflation helping by MSD rates on reported sales). These guides ain’t gonna be good. Potentially an opportunity to get more bullish on names on our Long list – and add new ones – where expectations get washed out. Stay tuned…

Home Depot (HD) | Reports Earnings Tuesday. Traffic trends look slightly worse than in 4Q, with Feb and March weakening then April improving, the Q trended down around 12% with May to date seeing improvement. One of the most important data points we have seen came from SHW commentary a few weeks back. We think home improvement has been satisfying a backlog of elevated demand from the 20/21 pandemic home boom. SHW management highlighted how the labor backlog in paint professionals has just recently normalized. “the bidding activity as having returned to a more normalized bidding market, where in the past 12 months to 18 months, maybe 24 months, it was difficult to get a painter to even come out and give you a bid because they were so busy and so backlogged, I would say that it's likely best described as a more level or more normalized bidding activity.” That means now sales/comps will match the underlying demand trends, which we think are much worse than what has been seen in recent home improvement comps. Meaning we could see comps trend to down mid to high single digits vs the expectation of barely negative. We have heard recent anecdotes around credit card data showing big ticket purchases slowing, which would be supportive of this backlog satisfaction and Pro demand slowing. Tack on the continued consumer goods consumption risk and we remain decidedly bearish on HD here in 2023. We’re coming in below on HD EPS at $3.65 in 1Q with comps below expectations and SG&A deleveraging. HD is a Best Idea Short with downside to $160 to $200. For details see our Home Retail Scenario Call Video Replay Link CLICK HERE

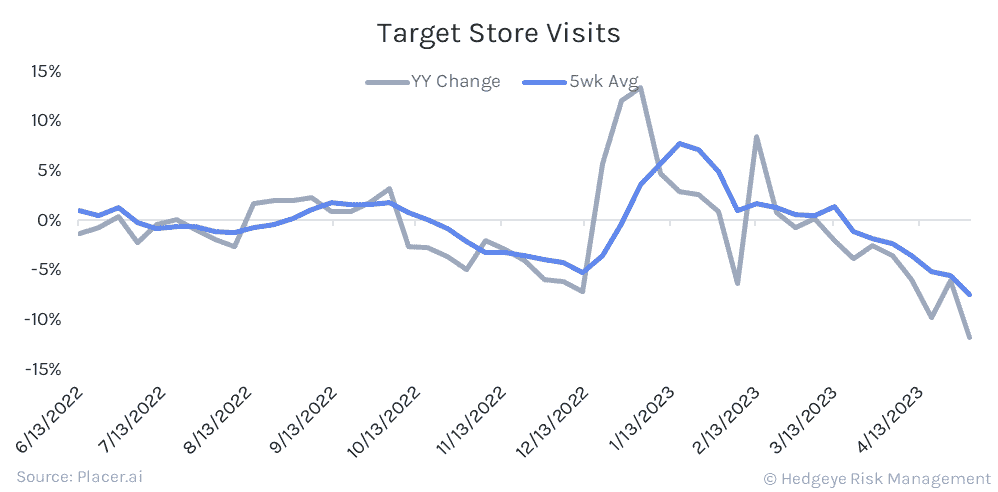

Target (TGT) | Reports Earnings Wednesday. Traffic trends at TGT have looked ugly. Our short call has been that demand would continue to deteriorate and comps would disappoint with SG&A deleveraging for further earnings downside. We’ve seen guide down after guide down here, and EPS for 2023 has gone from $12 at the end of October to now $8.25 at the guide midpoint. It still carries a high teens multiple. We think there is another guide down this year, though earnings are getting closer to where we think EPS will actually be. The market is excited about cost cut potential, but the company will have to reinvest in other areas, there won’t be much flow through especially with demand continuing to be under pressure. We’re coming in around $8 in EPS in 2023 and see much less upside than consensus in 2024, that makes for stock downside risk to $100 to $125. Consumer discretionary spend is getting worse, as is the employment situation. With BBBY going away, TGT should win some share, but that won’t come for another 6 months down the road or more, meanwhile BBBY is running its liquidation of inventory and the soft side of home continues to be under pressure making for further comp risk to TGT. TGT is expensive with slowing trends and still further earnings risk. We remain short TGT. For our TGT short Black Book Replay Link CLICK HERE

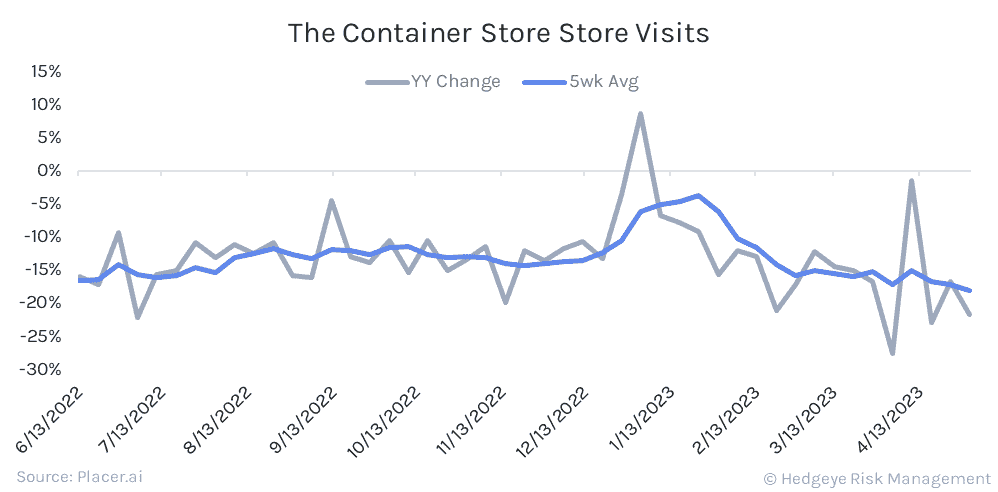

The Container Store (TCS) | Reports Earnings Tuesday. The stock call has been dead wrong, home consumption has come under pressure (which we expected), and earnings have come down, but we didn’t appreciate how low the multiple would go on this emerging square footage growth story. Stock is now at 4x consensus forward EPS. Traffic trends have been slowing slightly in recent months, down around mid to high teens. Beyond the fundamentals, the style factors are killing this stock. Small cap, private equity ownership overhang, with some leverage, all making for further underperformance. The leases put the optical leverage way out of whack. The company only has ~$190mm in debt with maturities in late 2025 to early 2026, so it’s a little less than 2x levered, not ~5x levered as it appears with the leases on balance sheet. TCS has nearly $100mm in liquidity as well. We still think you have TAIL earnings power in the $2 to $3 range with unit growth and comp potential. This is another one where share can be won from BBBY liquidating, but things will get worse before they get better in that context. TCS is increasingly looking like a go private candidate trading at a LSD PE multiple.

Monro (MNRO) | Reports Earnings Thursday. This is the worst house on a good street. The trends in the auto aftermarket and auto service space have looked pretty good. VVV and DRVN maintenance are delivering low teens comps. Meanwhile, MNRO is expected to print just 3% comps, it’s clearly a relative share loser, one we think does not deserve a 12x EBITDA and 27x PE multiple. Are earnings about to collapse here? Probably not, and compares are going to ease. Still, when we dive into the results, we think the setup here remains net bearish. Last Q comps adjusted for calendar impact of Christmas were up only 4.4%. Gross margin was down 150bps as the company cited that it “did not want to fully pass through inflationary pressures” on an already pressured consumer. Yet competitors are taking up price as needed so relative price trends would mean MNRO is promoting on price, yet not growing as fast as core competitors on a transaction basis. The most bullish data point was improved balance sheet positioning, which doesn’t mean too much at a high 20s PE, when net income was down 20% YY. On the last call the company was bullish on near term sales commentary noting accelerating growth to 8% comps, but recall last year same store sales went from up 14% in 3Q, to up 1% in January as of the comparable earnings report. So compares were much easier near term and we’re not sure there is a bullish underlying acceleration to get excited about. We are still short this as we think it’s a share loser in auto maintenance with weak growth and labor cost pressure meaning little to no earnings growth while carrying a big multiple. A short pair to our DRVN/VVV Longs.

Acushnet (GOLF) | Though this was the worst performer on our Short List last week, we’re taking a couple notches higher on our Best Idea Short list. Callaway outperformed last week in TopGolf, but missed materially in golf equipment ($444mm vs Street at $470mm) as the golf equipment space is finally starting crack. GOLF is a purer play on equipment, and is trading at a peak multiple on unsustainable earnings. We see 30-40% downside in this name, even after last week’s shellacking – likely sooner than later. Doesn’t hurt that the head of Titleist Golf Balls filed a 144 to sell ~1.5mm in stock.

Burberry (BRBY-LON) | Short Bias Idea BRBY announces Q4 and Full Year results Thursday. This past week it announced the new CFO Kate Ferry will start mid-July. Now there is effort here to revive the company and the brand with a new CFO starting soon and the new creative director, Daniel Lee, whose first line debuted in February. This company has had erratic sales growth for nearly 15 years, and had declining revenue going into the pandemic. Not to mention inconsistent margins over the same period. It is currently trading at 19x PE, which is relatively low for luxury, but KER is currently at 16x, which even though we took off our Long Bias list, we like as a company more than BRBY. BRBY is expected to end the year with revenues +10%, gross margins at 70.7% (nearing all time highs), and EBITDA margin of 30.8% (the highest its ever been). Its most recent revenue split is 25% Americas, 30% EMEIA, and 45% APAC, so if APAC and specifically China perform as well for BRBY as they have for other luxury companies, a 10% revenue growth is possible. But we still don’t think this is a strong company on a go forward basis. Too much inconsistency.

Farfetch (FTCH) | We have no skin in the game on this one, but are interested in it once the “POD”s turn. FTCH reports Thursday afternoon. The company provided guidance for FY23 of GMV +19% and EBITDA margin improvement of 590-790bps. Expectations for GMV are inline with guidance and EBITDA margin is at the low end of guidance. The company didn’t guide to sales, but expectations have growth in the mid-teens, following a 2% growth in FY22. Even with GMV down 4% this past year, the company saw MSD revenue growth, so given the guidance and expectation of high teens GMV growth, a mid-teens revenue growth seems reasonable. Expectations have Q1 minimally down in GMV and revenues and then recovering over the remainder of the year. Luxury ready-to-wear and accessories have been performing well based on the luxury names that have reported so far. FWRD, the more luxury brand at RVLV, put up 5% growth this past quarter, so FTCH could come in ahead of expectations in this print. We need to do more work before we pick a side on this one.

On Holdings (ONON) | Best Idea Short reports on Tuesday. This needs to be a MONSTER quarter out of ONON on the top and bottom line for the stock to not go down. Remember that 13-weeks ago the company ended the quarter with 190% inventory growth, the biggest of any retailer or brand by a long shot. We think that 80%+ of that inventory was planned to sell into the wholesale channel – which we think is a big mistake. As outlined in our deep dive Blackbook on ONON (link below) we think this company is growing at a reckless rate – which is not only unsustainable, but inclined to blow up sometime this year. The stock is up 52% since the last print, and expectations are justifyably high in the quarter. We think we’re likely to see lower gross margins due to the wholesale push, and then another crack in Gross Margins later this year when the company has to start sharing markdowns with the retail channel. Remember that 80% of sales come from one silhouette – albeit in dozens of different colorways. The company is not tiering its product appropriately by channel and by consumer – despite its claims. This is a management team that has never managed through either an economic or product cycle. Remember Olaplex? The beauty brand that lost half of its market cap in one tick due to overdistribution? That’s what we think happens with ONON in 2023. Check our deck for our full thesis. Black Book Video Replay Link CLICK HERE

Decker’s Outdoors (DECK) Taking Lower on Best Idea Long List – Partially Booking the Win. This stock has been on a tear. It’s up 92% off its May lows, and justifiably so. HOKA has been ripping, but unlike ONON, it has grown at a controlled rate while tiering its product by consumer and channel. It took a page right out of the Ugg playbook – which people expected to be dead a decade ago, and yet it’s still growing globally with its core boot now accounting for less than 10% of sales. This is one of the best management teams in retail. We went long around $300 in Jan 2022, and we still think that this is a $600-$700 stock over a TAIL duration. The risk here is that ONON is giving HOKA a ‘multiple halo’ and we can’t ignore the risk of that deflating sometime this year. Still a Best Idea but taking down a few notches in terms of conviction.

TJX Companies (TJX) | Best Idea Long. Unlike last quarter, we’re expecting TJX to use its balance sheet as an offensive weapon when it reports on Wednesday. Recall that despite having industry inventories at a generational high, TJX reported last quarter with inventories DOWN 5% instead of picking up inventory aggressively. Our sense is that the company knew things would get worse at retail and chose to wait to ‘corner’ the Ralph Lauren’s and Canada Goose’s of the world for the best buys it has seen in a generation. We’re looking for EPS of $0.75 vs the Street at $0.72, but will really be looking to the balance sheet before the P&L to what should be more elevated inventories (good in TJX’s case) in order to drive both comp and margin in 2H of this year. Usually off-price retailers have to choose between comp and margin, we think that TJX will get both. We put this long on at ~$60 and the stock is now at $78. We think that TAIL earnings power here approaches $5, which implies a stock ~$125.

Valvoline (VVV) | Taking a few notches lower on Best Idea Long List. We’ve gotten several catalysts out of the way – namely the sale of the Global Products (oil) business to Saudi Aramco, the announcement, and execution of a $1bn Dutch Auction for its stock. The stock is up 47% since October, and while we think that the next catalyst will be a change in coverage on both the sell side to retail analysts, and the buy side recognizing that Valvoline Instant Oil Change (VOIC) is one of the most defendable assets in retail. Greenfield growth, weak competition (Jiffy Lube and gas stations), superior service and technology, franchising opportunity, and fleet maintenance growth – all with ZERO Amazon competition. We still think this stock grinds higher to $50 over the course of a year, and $60 the year after that. But with the stock performing so well into this latest series of events, we’re simply taking it a few notches lower – most notable below Driven Brands (DRVN) which is now our top long in the auto services space.

Canada Goose (Best Idea Short) | Out with Earnings in a Seasonally weak quarter. Of the ~1bn in sales GOOS is likely to report this year, only about 5% occurs in this Quarter. If the company misses or beats (we suspect miss) we won’t declare victory or defeat. It’s simply meaningless. China re-opening should be a non event this quarter. Maybe a bigger deal in the fall, but that’s exactly when we’re expecting a big round of wholesale order cuts from retail partners who are loaded up on Canada Goose inventory. We think this company’s real earnings power is closer to $0.50, and MAYBE worth a low teens multiple. That’s good for 50% downside from current levels. If it’s up on a volatile low volume quarter, we’d press it hard. We’d press it anyway.

Foot Locker (FL) | No Position, but looking for a short entry point. We simply don’t believe this model, or Mary Dillon’s new plan to revitalize the chain. She’s a growth CEO, and there’s nothing growthy about Foot Locker – nor will there ever be. We think sneakers are a secular winner, but Foot Locker simply isn’t the ‘go-to’ place for limited edition drops anymore, and Nike will make sure of that (Nike DTC, SNKRS, GOAT, Stadium Goods (FTCH) and StockX). The narratives around ‘Nike and FL ties mending’ are a load of you know what. Nike won’t let that happen. The company’s margin goals are to get back to 2019 margins by 2026 – long time to wait. And the stock is sitting at $39. We don’t get it. This company HAS TO grow in order for the stock to work. We don’t see it. Will Dillon miss her first quarter out of the box after launching her plan? Almost certainly not, which is why we’re on the sidelines. But if this stock is up on this print, we’ll almost certainly short it again.

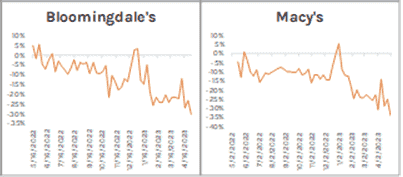

Macy’s (M) | We debated taking this name lower on our Best Idea List ahead of earnings on Thursday – but are sticking to our guns. It’s trading at 4x earnings, 3x EBITDA, and is the best run department store. But we can’t get around two factors. 1) Traffic trends at Macy’s look abysmal. And 2) about 50% of EBIT is credit income, which is likely to show sings of distress this week. Also, interestingly enough, it’s not heavily shorted – only 8% of the float held short, which is low for Macy’s. So the risk of a rip on a better (albeit unlikely) print is probably not in the cards.

Wolverine Worldwide (WWW) | Taking higher on Best Idea Long List. Aside from putting up a better than expected quarter (and the stock squeezed accordingly) management dropped a bombshell that it’s selling yet another asset – its Sperry business. Reminder that this is what we call a ‘POD 3 call’. In that the company sells assets, reduces complexity and working capital, de-levers the balance sheet, while simultaneously channeling capital into R&D and Marketing to reaccelerate revenue and margins. We think there’s better than $3 in EPS power here which we think gets a 12-15x multiple. This will take time, but we get to a $40-$45 stock – better than a double from current levels.