Data from the BLS today a positive data point for restaurants.

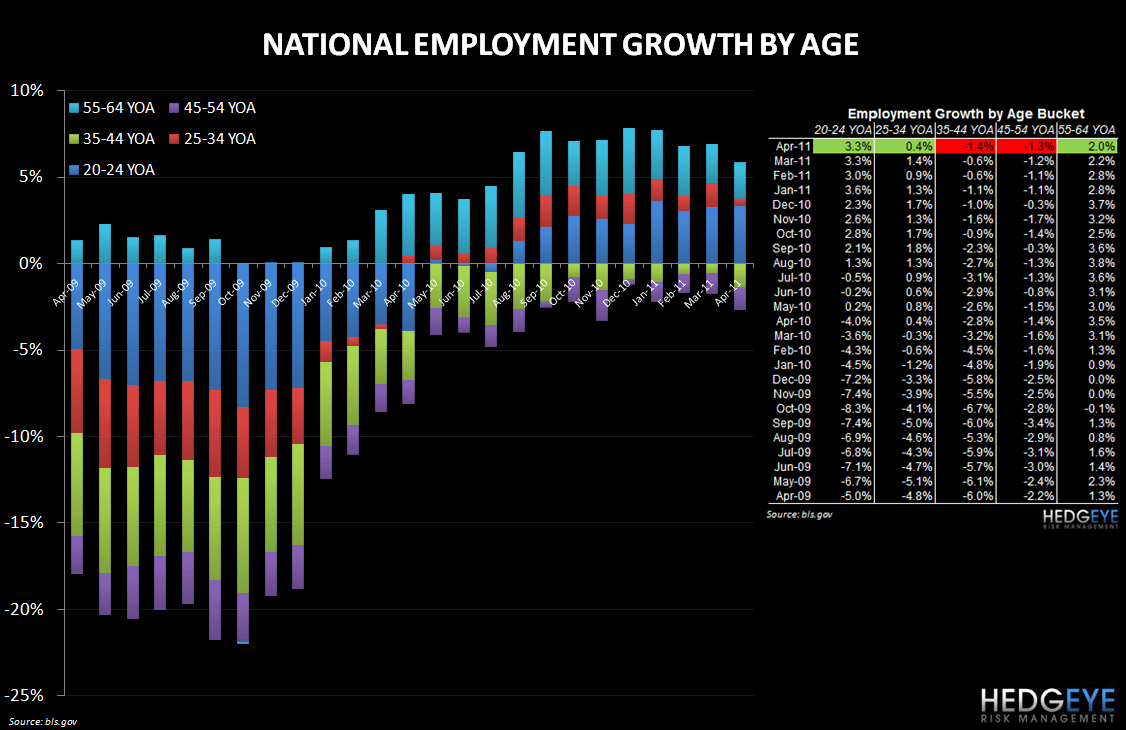

April employment data was released today by the Bureau of Labor Statistics. As our Healthcare team pointed out this morning in their daily Healthcaster piece, the employment recovery “continues to be a barbell recovery with younger demographics, who don’t consume much healthcare, and older workers.” The 20-24 years-of-age and the 55 years-and-higher age cohorts continue to gain while the 34-54 years-of age cohort continues to slide. For restaurants, the recovering in employment levels among younger people is a positive for quick service restaurants, as I have written over the last number of months in these updates. Interestingly, looking at employment trends in the full-service and limited-service sub-sectors of the food service industry also strikes a positive tone for the industry.

I am aware that many big corporations, as the saying goes, hire at the top and fire at the bottom. However, as long as the employment growth in the younger age cohort continues to trend in the right direction, employment will continue to be a positive driver for QSR. The chart below also shows a sustained growth, since early 2009, in hiring by full-service restaurants. For eating out, as a whole, it is important to pay attention to the soft employment trends in the 34-54 years-of-age bracket. This is an important group for restaurants and the continued slide in employment levels is a negative for casual dining.

Howard Penney

Managing Director