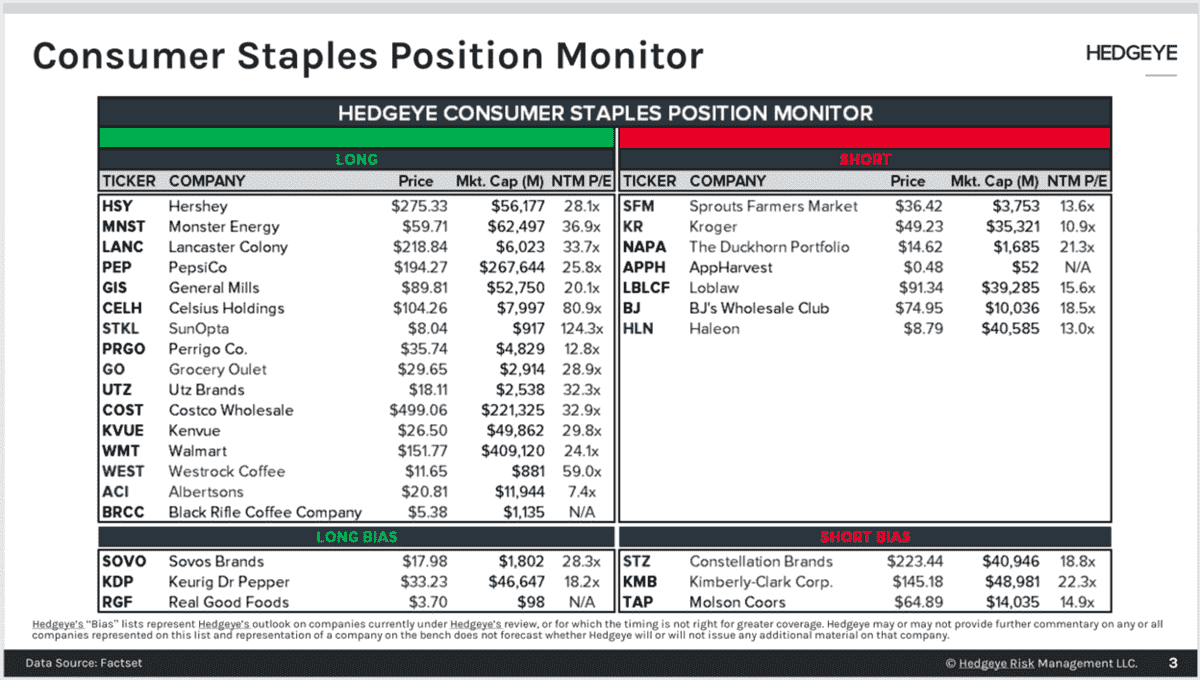

Position Monitor Changes (WMT, COST, TAP)

We are making several changes to our position monitor reflecting our Macro team’s Quad projections for the next three quarters. Consumer Staples historically has outperformed in Quad 4 and with more Quad 4 projected ahead we are adding to our Long list. We are also making some ranking changes to reflect the style factors that have the highest expected values in Quad 4. We have filtered our long list with the filters of low beta, dividend yield, quality of earnings, secular growth, and value. Consumer Staples is one of three sectors with positive returns so far for Q2.

HSY - Hershey moves to the top of our Best Idea long list. Hershey stands out in CPG in 2023 with volume growth visibility as well as new price increases still being added. Management only went to the high end of the range after Q1 due to Q2 having the most difficult comparisons combined with the earlier shipments. Our estimates continue to be above consensus expectations. Management appears conservative on gross margins in the 2H based on current trends.

PRGO – Perrigo moves lower on the list due to leverage and quality of earnings style factor considerations. The FDA released the briefing materials ahead of the advisory meeting for Opill on May 9-10. The briefing materials read critically about the benefit for consumers to purchase Opill OTC compared to the risk of not taking the pill daily and discussing any issues with a healthcare provider. Opill’s approval is not in the share price. Should it be approved the $100-200M in revenue upside would lead to positive EPS revisions for the first time in years.

COST – We are adding Costco back to our long list after being on the long bias list. April sales results give us more confidence the company’s consumables mix can continue to drive overall SSS of +LSD%. A membership fee increase seems less likely in a weakening consumer, but more of a surprise for expectations. Costco’s membership is unlikely to see a meaningful change as a result of an increase with inflation so prevalent.

WMT – We are adding Walmart back to our long list after being on the long bias list. Walmart’s food sales mix will underpin positive SSS growth. We had removed Walmart from the long list previously because there was less upside in our estimate vs. consensus expectations. In a longer Quad 4 regime we are less concerned about the amount of upside and just that there is upside.

TAP – AB InBev potentially discounting in the U.S. is a risk to be monitored. We are moving it to the short bias list as it benefits from its largest competitor shedding share in the U.S. The benefit to Molson Coors is more than the detriment to AB InBev for now.

Competition at the low end (WMT)

Aldi said it plans to open 120 stores in 2023, bringing its total to 2,400 in the U.S. Last year the company opened and remodeled 139 stores. Aldi is opening in new markets in Southeast and Midwest. While Walmart closed four Chicago stores recently, Aldi is opening up stores in the area. According to placer.ai traffic to Aldi’s stores increased 7.3% in Q4. The traffic gains have slowed in 2023 as seen in the chart below, but it is not changing the store opening plans. Of course, Aldi is not the only discount food retailer opening stores. Dollar General and Dollar Tree are expected to open a combined 1,500 stores this year. Exacerbated by elevated food inflation food retail remains the most competitive sector of retail. We have been in a period of low competitive intensity brought on by supply chain challenges, but that is changing.

Plant-based labeling (STKL)

The FDA is reopening the comment period for the draft guidance on plant-based milk labels. Several key stakeholders have requested more time to comment. The deadline has been pushed out to July 31 at the behest of the Plant Based Products Association, the Good Food Institute, the International Dairy Foods Association, among others. The draft guidance, which was introduced in February, proposed to allow plant-based milk to continue to use the term “milk,” but to also voluntarily compare it to the nutritional value of dairy milk. Both the plant-based industry and the dairy industry disagreed with the draft guidance but for different reasons. The FDA has made few labeling requirements for the plant-based milk industry, angering the dairy industry. Requiring the plant-based milk industry to no longer use the term “milk” is much like shutting the barn door after the horses had bolted.

The plant-based milk industry has benefited from being featured in food stores adjacent to dairy milk. Plant-based creamers are seeing a similar benefit currently. The plant-based creamer category grew 24% in 2022 with unit growth of 12% compared to a 1.4% decline in animal-based creamers. That compares to 9% growth for plant-based milk with a 2% unit decline in 2022 and 12% growth for dairy milk with a 2% unit decline. Creamers are the third largest plant-based category after milk and meat. Coffee creamers are a natural extension for plant-based milk and especially oat milk. Oatly targeted baristas when it entered the U.S. market and Starbucks is SunOpta’s largest customer.