“It’s choice not chance that determines your destiny.”

-Jean Nidetch

Interestingly this quote comes from a one-time overweight housewife with a self-confessed obsession for eating cookies—a woman who eventually kicked her weight and went on to start a peer group to support her overweight friends, which expanded and in 1963 was incorporated as the Weight Watchers organization.

The quote also seemed appropriate for it reminded me of the vaulted status of global central bankers and their choice (along with a committee vote) to act or not (in what sometimes seems like chance) to direct a country’s monetary policy, and therefore economic health. In the recent era, central bankers have attained a sort of rockstar status typically reserved for celebrities and athletes, and just this week Ben Bernanke joined the club of celebrated central bankers (notably the ECB’s Jean-Claude Trichet) with a live press conference following his policy announcement—trappings that must clearly enhance his “cult” status.

Yet, with today being the Royal wedding day, and with my role being European analyst on the Macro Team, we thought we’d give The Bernank a needed rest and focus on the actions across the pond at the Bank of England, namely the hefty choice that CB Governor Mervyn King faces with the UK stuck between stagnant growth as inflation accelerates.

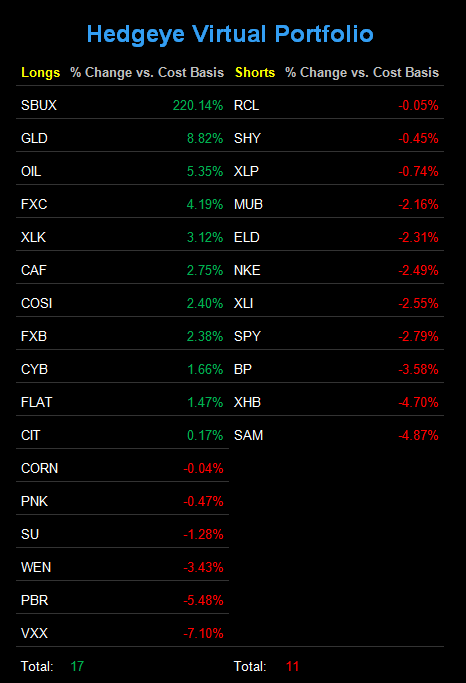

In particular, we’d like to call out the strength of the British Pound versus the USD, in our opinion an out-of-consensus call that we’ve been long of via the etf FXB in the Hedgeye Virtual Portfolio since 3/23 due to the following positive factors:

- The BoE’s increasingly hawkish lean on inflation and evidence that suggests the positive currency impact of an interest rate hike (examples include ECB and Riksbank decisions)

- The announcement of austerity by the UK Government in the fall of last year to proactively cut public spending and boost revenue, versus the US’s passiveness in addressing its rising debt and deficits, a position that has perpetuating a weak USD versus most major currencies (US Dollar Index down for 14 of last 18 weeks)

- Bernanke’s commitment to keep rates near zero percent and his indication that some form of QE-lite will follow QE2’s expiration in June = continued USD weakness

- The flight to safety of Sterling as Eurozone debt contagion remains at large (also bullish for the CHF and SEK)

The Proof is in the Pudding

While the above points have been supportive of the GBP-USD trade to some degree this year, the prospect of high inflation with slow growth in the UK is the pressing threat facing policy makers. And while there are numerous ways to spin the headline data out of the island nation, in our mind it’s hard to argue against the inflation data, which has charged higher for the last 18-22 months. The current inflation readings include:

- Consumer Price Index (CPI) +4.0% in March Y/Y

- Producer Price Index (PPI) for Input +14.6% in March Y/Y

- PPI Output +5.4% in March Y/Y

While the BoE drew a sigh of relief with the March CPI number 40bps below the February reading, current levels are a full 2% higher than the BoE’s target, and 1.5-2.5% above European peers, as rising energy costs continue to fuel high readings this year.

While the BoE has maintained its 0.50% benchmark rate since March ‘09, the lowest level in over 300 years of the history of the BoE, we’re of the camp of Andrew Sentance, one of the nine voting members of the BoE’s Monetary Policy Committee, and affectionately known as the ueber inflation hawk due to his very vocal stance for an interest rate hike since June 2010. We’re now seeing in the last few BoE meetings that fellow members Spencer Dale and Martin Weale have joined ranks for a rate rise of 25bps, while Sentance has upped his rate hike call from 25bps to 50bps, leaving the committee a 6-3 vote against interest rate action, but marginally more hawkish.

Below are a few key drivers that Sentance notes to justify a rate hike, which he’s included in this speaking tours:

- The UK’s need to strengthen its currency with its trading partners, particularly against the EUR as the Eurozone accounts for about half of total exports and half of total imports.

- A stronger domestic currency will help to combat imported inflation. The renewed surge of energy and commodity prices only adds to the imported inflation driven by a weak Sterling versus the EUR since 2007.

- The squeeze on disposable income is already a factor holding back the growth of consumer spending in the short term.

- Ergo, a rate hike is essential to boost the Sterling versus the EUR and other major trading partners to mitigate inflation and therefore improve consumer spending.

Not so Fast – Austerity’s Bite and Growth Fears

While Sentance makes some very convincing points supportive of a rate hike, others remain convinced that excess capacity in the economy will slow/drive down prices and that a rate hike would only create a further shock to the consumer.

Rightfully, this camp also points out the negative impact of the government’s austerity program, which broadly calls public job cuts of ~500K and ~£81 Billion in public spending cuts over the next 4 years, and an increase in VAT (from 17.5% to 20%) that began in the beginning of this year. Their position is that weaker consumer and business surveys are indicative of the strain of public sector deleveraging and expectations for slower growth. Additionally, it is argued that the negative impact on the housing mortgage market from a rate hike—with the housing sector mired in an anemic state—would be an additional blow to the consumer’s wallet.

Boiling it Down

As we’ve said from the outset, there are any number of ways to interpret the data. Arguably the BoE and UK government are left in a tough spot, trying to head off inflation while not pinching growth prospects. For reference real annual GDP was +1.4% last year, with the final quarter of 2010 showing a -0.5% hit Q/Q, while 1Q2011 rebounded to +0.5% Q/Q.

While the jury is still out on whether or not Q1 can be a sustained inflection, our call is focused on the implication of the Pound versus the USD, in particular, but also the EUR. We continue to applaud PM David Cameron’s forceful strategy to reduce fiscal debt and deficits, which according to the UK statistical office were 59.6% of GDP in 2010 and 10.4%, respectively (see chart below). Notably, the chart of cumulative public sector net borrowing shows improvement across annual compares, an indication that austerity may, in fact, be working.

Further, compared to the US administration, Obama and Company are just now coming to terms with the budget ceiling debate and the great issue on shaving down the budget deficit that is expected to rise well over 10% next year, according to our calculations, with the US debt as a % of GDP expected to reach 96% this year and over 100% next.

On these metrics, we think the UK’s proactive attention to reduce fiscal imbalance, coupled with the increased likelihood of an interest rate rise, should boost the GBP versus the USD. Should we get a rate hike, it should help alleviate inflation pressures, which will improve consumer and business optimism and therefore encourage growth prospects over the intermediate to longer term. Given the likelihood that elevated input cost pressures are here (globally) to stay over at least the medium term, we think there’s prudence in a rate hike.

Increasingly we’re seeing the bifurcation in economic performance on the basis of policy decisions to cut fiscal imbalances and increase interest rates off historical lows. So long as the US continues to fuel its monetary policy of extend and pretend and promote the fiscal printing press, we’d expect the USD to suffer versus major currencies. Getting long the GBP-USD is but one way we’ve chosen to express this bifurcation.

Matthew Hedrick

Analyst