Position in Europe: Long British Pound (FXB)

As we noted in the European Risk Monitor yesterday, Europe’s sovereign debt issues continue to drag and perpetuate headline risk, however the EUR against most major currencies and most European equity indices continue to shake off these threats under the belief that the heavy hand of the EU and IMF will extend to any and every country that needs financial relief. If we add continued hawkish comments on inflation from the ECB and weak USD policy to this mix, we think these are the main catalyst driving the strength in the EUR-USD. Keith’s models suggest the EUR-USD has immediate term support at $1.44 and resistance at $1.46, so we’re currently at an overbought level.

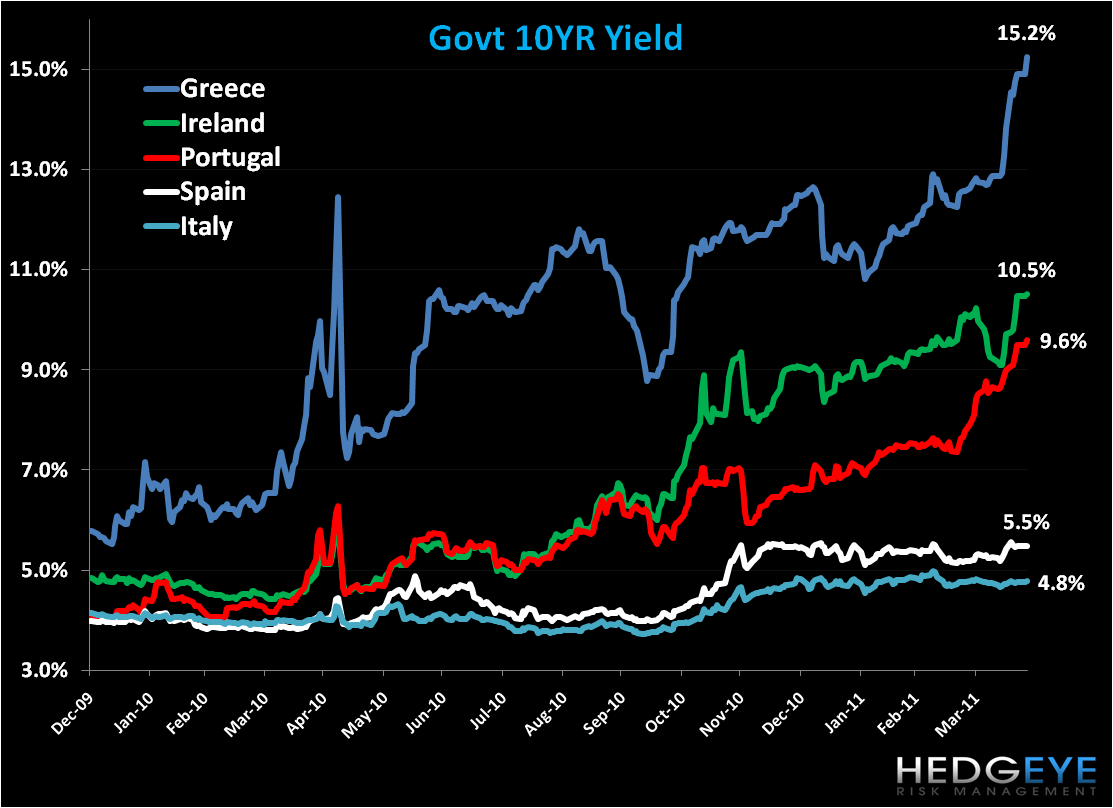

Risk in Greece and Portugal are the main focal points at the moment. Regarding Greece, discussions surround a potential restructuring of government debt, which we think is a foregone conclusion given the expedient rise in government yields and therefore the severe headwinds in store for future debt issuance and interest payments (see chart of 10YR Greek yields and the other PIIGS below).

As always, Greece’s fiscal imbalances are glaring and expanding. Debt as a % of GDP is expected to ramp to 159% in 2012, and PM Papandreou and Co. plan to reduce the country’s deficit from a high of 15.4% of GDP in 2009 to 3% by 2014. We’re of the camp that they’ll come up short.

A bailout of Portugal also lingers, with an estimated agreement to the tune of 50-80 Billion EUR set for mid-May. As we present in the chart below, catalysts for this deadline include getting ahead of a hefty payment of government debt (principal and interest) in June (~ 7.1 Billion EUR) and elections for the next government in June.

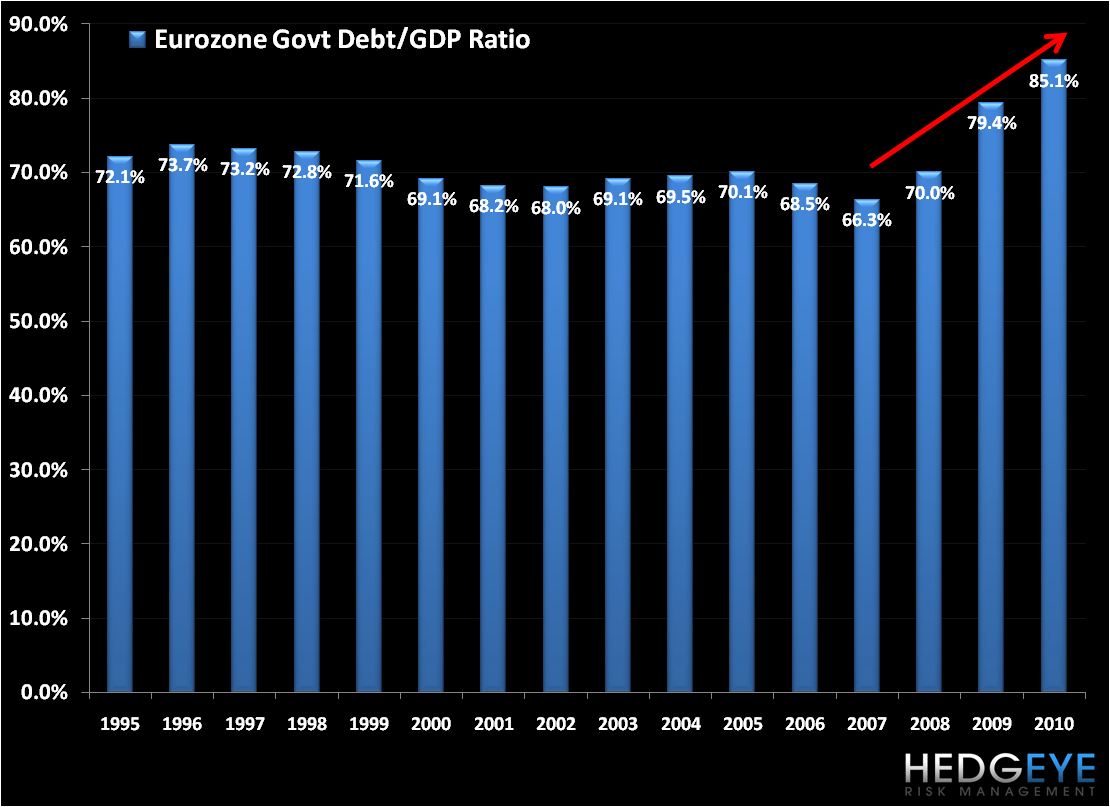

Not unlike in the US, aggregate public debt levels are increasing across Europe, despite such standouts as the UK that is actively tightening spending and enhancing revenue. Today, Eurozone debt as a % of GDP was released for 2010 at 85.1% versus 79.3% in 2009. We pulled the data back in the chart below. We think we could see a significant slope to the year-over-year change of outstanding debt over the next 3-5 years as the periphery struggles to reduce years of fiscal imbalances.

Matthew Hedrick

Analyst