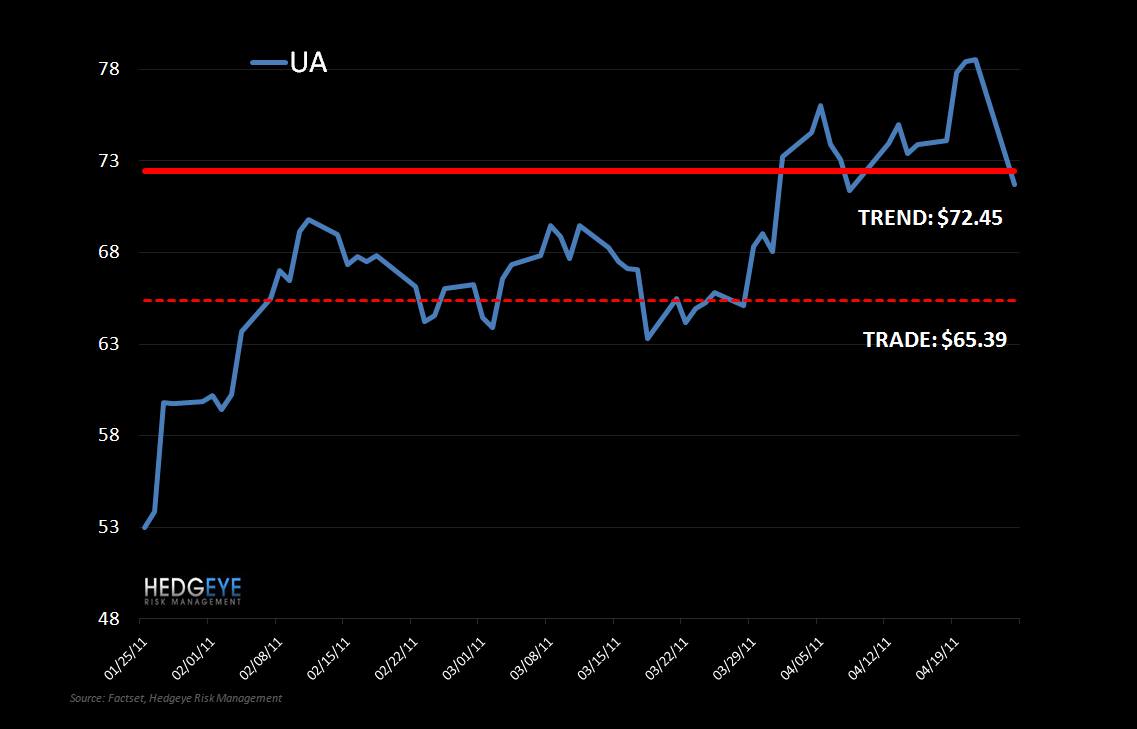

We’ve had several folks ask this morning for Keith’s levels on UnderArmour. Here you have it…

Just broke through significant TREND.

If you’re short the name, I wouldn’t rush to cover.

We’ve had several folks ask this morning for Keith’s levels on UnderArmour. Here you have it…

Just broke through significant TREND.

If you’re short the name, I wouldn’t rush to cover.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.