“Things may come to those who wait... but only the things left by those who hustle”

– Abraham Lincoln

It was exactly one month ago that our anxiety meter hit an all-time high. Which would indicate the anxiety of the bears. Today, that anxiety has come well off the highs and is approaching a neutral rating. Although, with lower anxiety can sometimes come comfortability with positioning.

This comfortability, or over confidence, can create a lack of process and focus that is needed within bear markets. So don’t forget the reasons for your anxiety last month and continue to treat the tickers as pieces of inventory. Operating at the tops and bottoms of the risk ranges.

The macro data never stops and continues evolve. Especially within a go anywhere strategy there are always next moves to make.

Back to the Global Macro Grind…

This is a lighter week for economic data and is all about employment. ADP and JOLTS are on Wednesday and the Employment report is on Friday. Next week we get CPI, PPI, Retail Sales, and Industrial Production.

Looking at CPI, part of the process is to look at February CPI reports around the world to see how they are trending. We currently have 22 of 47 countries we track which have reported YoY CPI in February. 8 of 22 accelerated, 2 of 22 held flat and 12 of 22 decelerated. Although the decelerations remain very modest and with the largest decelerations coming from Asian countries (Taiwan and Thailand). While the accelerations and flat readings are coming from Europe (Eurozone reported +8.5% YoY in Feb from +8.6% YoY). The conclusion from this data set would be for a continued slow trend downwards as our nowcast points to. This is while the market has implied rate hikes of 25 bps over the next 3 meetings (until June).

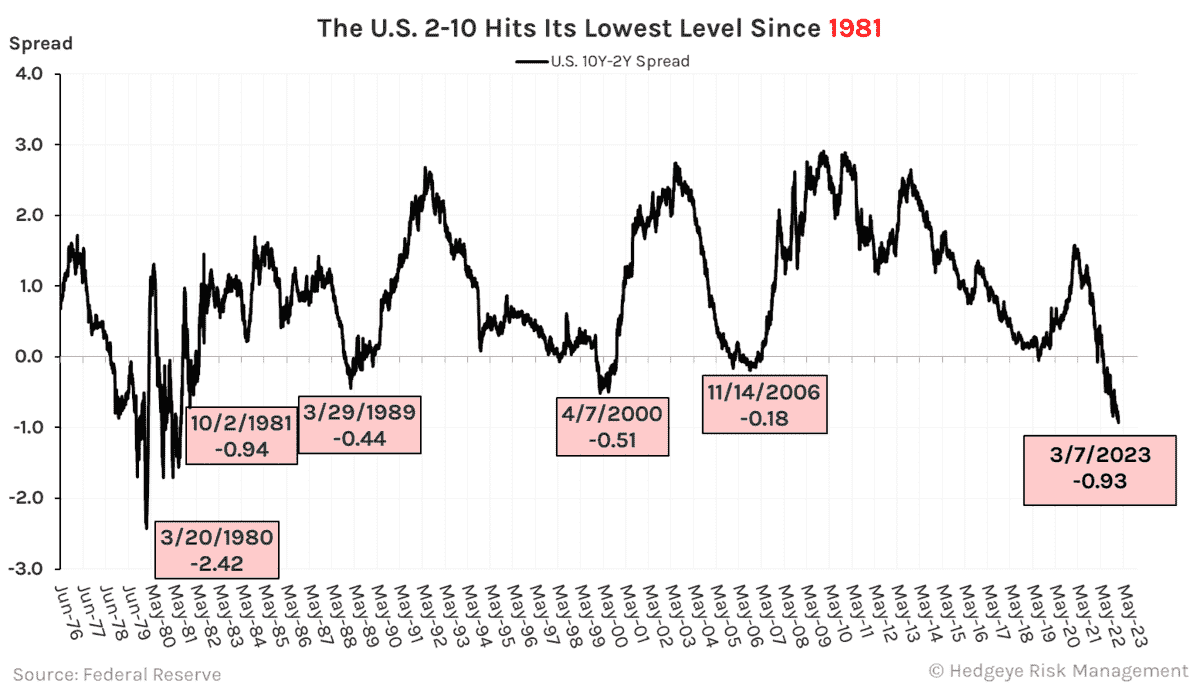

Moving to 2-10 spreads, we are waking up to continued cycle lows with a bone chilling -93 bps on the US 2-10 Spread (lowest since Oct 1981). On top of this the 1yr Forward 2-10 Spread that is implied is at -62 bps which is 5 bps points off of the cycle low set in April of -67 bps. This is implying a lower current 2-10 spread for longer.

While the US 2-10 spread hits cycle lows we are seeing a similar story around the world with Germany’s 2-10 spread hitting a cycle low of -60 bps its lowest level since 1991. Switzerland’s 2-10 spread inverted for the first time this cycle at -4 bps which is an all time low (data going back to 1994). This is a trend we are seeing across Europe, although equities continue to diverge from the bond market signal (Germany went bullish trend yesterday). This is not something we are going to fight, making money and being right are two different things (a Mike Taylor ism).

Now for the more immediate term data. After being at the top end of the risk range for a week, Natural Gas was the worst performing asset yesterday (down -12.5% DoD $UNG), although it is currently sitting in the middle of the risk range with downside potential of 22.4% and upside potential of 23.7%.

Yesterday U.S. energy related equites diverged from Crude Oil (+0.98% DoD) as both $XOP (-1.95% DoD) and $PSCE (-2.19% DoD) declined. In terms of global energy related equities $KSA, $QAT, and $UAE also remained elevated. $QAT is in Real Time Alerts with $UAE being in ETF Pro.

Moving to the bongo board, 6 of 11 sectors were down with the sectors we are short leading the way ($XLB -1.6% and $XLY -0.73%). The S&P 500 was up (+0.07%) on down volume (-6% vs the 1M average). Currently $GOOGL, $APPL, $MSFT, and $XLK are approaching the top ends of the risk range (within a bearish trend). With the VIX approaching the low end of its risk range as the market has created another ball under water probability (VIX at 18.6). But even with this Real Time Alerts remained silent so let’s see what 0DTE does today and react from there.

Crypto was flat yesterday and is in the lower part of its range, upside potential of 8.8% and downside potential of 3.4%. $TSLA is the same story with upside potential of 8.4% and downside potential of 5.9%.

In terms of next moves that I will ask Keith on the Macro Show the next time I’m on is Israel $EIS. We are finally seeing it come off the low end of its Risk Range while sovereign CDS spreads are remaining near cycle highs.

Lastly, looking at international economic data that came out in the last 24 hours the biggest change I saw was China Export and Import numbers. Headline Exports were up sequentially to -6.8% YoY (Feb) from -9.9% YoY (exports to: US (-21.8%), EU (-12.2%), ASEAN (+9%), and Russia (+19.8%)).

Headline Imports were down sequentially to -10.2% YoY (Feb) from -7.5% YoY (imports from: US (-5%), the EU (-5.5%), ASEAN countries (-8.3%), and Russia (+31.3%)). This is a trend we have been continuing to monitor where the reopening has remained within the local markets (the opposite of the headlines telling you that China is going to fuel the world’s economy with its opening).

Australia $EWA raised its cash rate by 25 bps to 3.6%, in line with expectations. The central bank’s target is 2-3% with current inflation at +7.8%. The RBA’s expectations are for 3% inflation by mid-2025 and also provided the following commentary: the RBA will “keep the economy on an even keel but the path to achieving a soft landing remains a narrow one.” The market is implying peak rates of 4.016% by September 2023 and a 40% probability of another 25-bps rate hike in April.

Lastly Norway $NORW Industrial production (Jan) decelerated to -6.6% YoY from 0.0% YoY, the 2nd sequential deceleration and the first contractionary number since November 2020. Leading the drop was electricity gas & steam (-5.8% YoY vs -7.4% YoY) and manufacturing, mining & quarrying (-0.8% YoY vs +0.3% YoY), mainly from wood and wood products (-17.2% YoY).

- IVOL Discount Callouts: Turkey $TUR, Self Driving Car $IDRV

- IVOL Premium Callouts: UK $EWU, France $EWQ, Germany $EWG, Malaysia $EWM, Singapore $EWS, Australia $EWA, New Zealand $ENZL, Solar $TAN, Clean Energy $PBD, Defense $ITA, Cannabis $YOLO, Pharma $PJP, Health care equipment $PSCH, Lithium $LIT, Soybean $SOYB, Rare Earth Metal $REMX, Canadian Dollar $FXC, US Govt ($TLT, $IEF, $TIP), 10+yr Corp $IGLB, EM Bond $EMB, Muni $TFI, Convertible $CWB

Immediate-term Risk Range™ Signal with @Hedgeye TREND signal in brackets

UST 30yr Yield 3.87-4.04% (bullish)

UST 10yr Yield 3.84-4.08% (bullish)

UST 2yr Yield 4.61-5.00% (bullish)

High Yield (HYG) 72.90-74.99 (bearish)

SPX 3 (bearish)

NASDAQ 11,239-11,747 (bearish)

RUT 1 (bearish)

Tech (XLK) 133-141 (bearish)

Defense (ITA) 115-119 (bullish)

Utilities (XLU) 63.80-67.75 (bearish)

Shanghai Comp 3 (bullish)

DAX 15,160-15,698 (bullish)

VIX 18.10-23.51 (bullish)

USD 103.77-105.50 (bullish)

EUR/USD 1.051-1.069 (bearish)

Oil (WTI) 73.20-80.99 (bearish)

Nat Gas 2.18-3.16 (bearish)

Gold 1811-1872 (bullish)

Copper 3.92-4.22 (bullish)

Silver 20.33-22.01 (neutral)

TSLA 183-212 (bearish)

Ryan Ricci