TODAY’S S&P 500 SET-UP - April 20, 2011

As we look at today’s set up for the S&P 500, the range is 25 points or -0.20% downside to 1310 and 1.70% upside to 1335.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1026 (+2908)

- VOLUME: NYSE 836.38 (-19.8%)

- VIX: 15.83 -6.7% YTD PERFORMANCE: -4.45%

- SPX PUT/CALL RATIO: 1.80 from 2.11 (-10.82%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 21.291 22.305

- 3-MONTH T-BILL YIELD: 0.06%

- 10-Year: 3.39 from 3.40

- YIELD CURVE: 2.71 from 2.71

MACRO DATA POINTS:

- 07:00a.m.: MBA Mortgage Applications, Apr 15, 5.3% actual

- 10:00 a.m.: Existing Home Sales, est 5.0m, 4.88m prior

WHAT TO WATCH:

- DoJ said to query market participants about how takeover of NYSE would affect competition in equity listings

- Chi-X Global said to be in advanced talks with four banks, trading firms to sell minority stake: FT

- Berkshire Partners in talks to buy Husky Injection Molding Systems in deal that could be worth up to $2b: Globe and Mail

- EBay may announce as soon as today purchase of WHERE, service that lets mobile-phone users get info. on nearby businesses

- AES agreed to buy DPL Inc. for $3.5b in cash, adding more than 500k customers in Ohio, AES said earlier today

- Panasonic set to announce plans to move its North American HQ to Newark, New Jersey, later today

COMMODITY/GROWTH EXPECTATIONS:

COMMODITY HEADLINES FROM BLOOMBERG:

- Gold Exceeds $1,500 as Dollar Drops on Concern About U.S., European Debts

- Sugar Exports From Thailand to Climb 36% as Yields Surge on La Nina Rains

- Copper Rises as Dollar Weakens; Aluminum Reaches Highest Price Since 2008

- Tepco's LNG Imports to Jump 50% as Japan Rewrites Policy: Energy Markets

- Wheat Set for Longest Advance in Three Months on Dry Weather; Corn Climbs

- Sugar Rises for Second Day as Brazil Supply May Be Delayed; Coffee Climbs

- Cotton Farmers in China Fail to Boost Crop, Top Agency Says; Prices Climb

- India May Ease Sugar, Wheat Export Bans Amid Predictions for Normal Rains

- China Issues Emergency Notice to Curb Aluminum Projects Amid Overcapacity

- Cotton Moving Average Signals 12% Drop, FCStone Says: Technical Analysis

- Cut Diamonds Outpacing Gold Still `Grossly Undervalued': Chart of the Day

- Rusal May Reach Agreement on $4 Billion Syndicated Loan as Early as May

- Corn, Cotton Rallies May Weaken as U.S. Output Shifts, Deere's Allen Says

- Hindalco, Sterlite Said to Have Doubled Copper Refining Fees After Quake

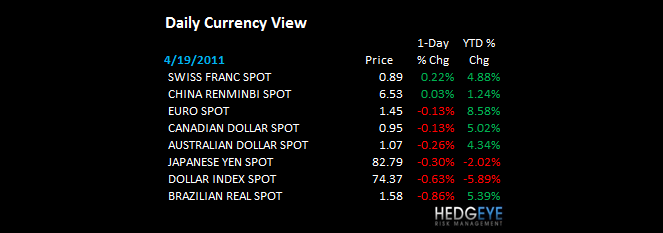

CURRENCIES:

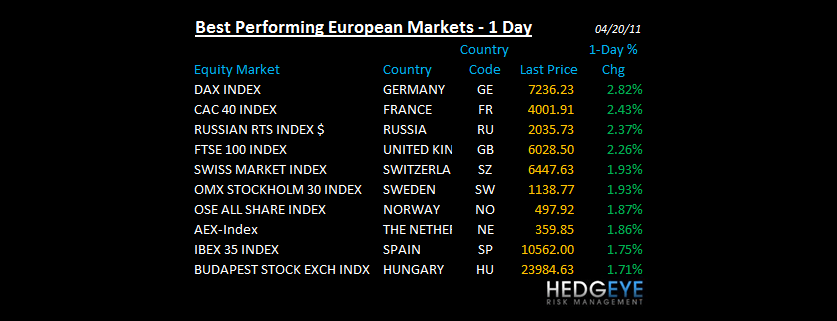

EUROPEAN MARKETS:

- European Stocks Rise as Peugeot, L’Oreal Sales Spur Confidence in Recovery

- Bank of England Voted 6-3 to Hold Rate as Majority Highlighted ‘Downside’

- Company Refinancing, Sovereign Debt Hurt European Recovery, Moody’s Says

- Peugeot First-Quarter Sales Rise 10% on New Models, Emerging Market Demand

- Vodafone May Consider IPO of Indian Joint Venture After 2011, Colao Says

- ECB Raising Rates May Turn Into Mistake Weakening Euro, Standard Life Says

- Cat Bonds Find Bottom After Quake Triggers Biggest Losses: Credit Markets

- Long Bond Scrapped as Yield Gap Nears Widest Since January: Russia Credit

- Farmers Get Rich as Wheat Trade Gives Deere Record Profit: Freight Markets

- Yen, Dollar Decline as Stocks Gain; Euro Advances on Interest-Rate Outlook

- Audi Targets ‘Suburban Mommies’ With Compact SUV Rivaling BMW’s X1 Model

- Skyscraper Boom Reaches End as City of London Goes 'From Vanity to Sanity'

ASIA PACIFIC MARKETS:

- Asian Stocks Rise as U.S. Housing, Earnings Boost Confidence; BHP Advances

- Li’s ‘Superman’ Status Tested in Hong Kong as Yuan IPO Meets Tepid Demand

- China Mobile First-Quarter Profit Rises, Helped by Wireless Internet Usage

- Thailand Raises Benchmark Interest Rate to 2.75% as Inflation Accelerates

- Power Bonds Rally Before First Global Bond Offering of 2011: India Credit

- China Issues Emergency Notice to Restrict Aluminum Projects; Prices Jump

- Indonesian Millionaire Uno Sees More Buyouts as Conglomerates Sell Units

- Vedanta May Use $1.5 Billion Cairn India Purchase as Hedge for Open Offer

- Acer Declines to Lowest in Two Years After Cutting Forecast for Shipments

- Tepco's LNG Imports to Jump 50% as Japan Rewrites Policy: Energy Markets

- New York Loses to Shanghai as Toyoda, Ghosn Head to China’s Top Auto Show

- Christchurch Banker Exodus After Quake is Aftershock For Property Market

MIDDLE EAST:

Howard Penney

Managing Director