THE HEDGEYE DAILY OUTLOOK

Sovereign debt concerns in Europe are mounting, once again, as Greek two- and ten-year government bonds slumped, driving yields to the highest level since before the inception of the Euro. Oil has declined as Saudi Arabia’s oil minister says that markets are “oversupplied”.

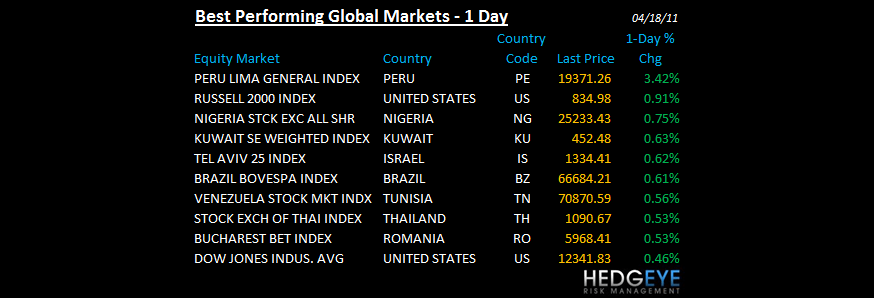

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1105 (+878)

- VOLUME: NYSE 1040.22 (+16%)

- VIX: 15.32 -5.84% YTD PERFORMANCE: -13.69%

- SPX PUT/CALL RATIO: 2.11 from 1.50 (40.67%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 21.32 -0.075 (-0.351%)

- 3-MONTH T-BILL YIELD: 0.07%

- 10-YEAR: 3.43 from 3.51

- YIELD CURVE: 2.72 from 2.74

MACRO DATA POINTS:

- 08:30 a.m.: Housing Starts: est. 520k, prior 479k

- 08:30 a.m.: Building Permits: est. 540k, prior 517k

- 08:30 a.m.: Housing Starts MoM % Chg: est. 8.6%, prior -22.5%

- 08:30 a.m.: Building Permits MoM% Chg: est. 1.1%, prior -8.2%

- 10:00 a.m.: Fed’s Fisher, Lockhart to discuss globalization in Atlanta

- 11:00 a.m.: Export Inspections (corn, wheat, soybeans)

- 11:30 a.m.: U.S. to sell $30b in 3-mo., $28b in 6-mo. bills.

- 12:30 p.m.: Fed’s Bullard to speak on banking rules in Kentucky

- 04:00 p.m.: Crop progress report

WHAT TO WATCH:

- U.S. 2yr yield falls to 3-week low before housing data at 10 a.m, median est. 17 by 39 analysts:

- Pulitzer Prize winners announced, 3 p.m.

- ECB’s Bonello urges caution against rate hikes at the expense of economic growth

- Deutsche Telekom, France Telecom agree on JV to save EU1.3b

- Ferrari IPO should be worth $7.3b, Marchionne says

COMMODITY/GROWTH EXPECTATIONS:

COMMODITY HEADLINES FROM BLOOMBERG:

- Snickers-to-Noodles Surge Drives Cooking Oil Supplies to Three-Decade Low

- China Said to Limit Industrial Corn Use to Meet Demand For Livestock Feed

- Oil Declines in New York After Saudi Arabia Says Market Is `Oversupplied'

- Hedge Funds Raise Bearish Gas Bets After ‘Dead Cat Bounce’: Energy Market

- Corn Falls for Second Day as China Raises Reserve Ratios to Cool Inflation

- Coffee Climbs as Rains May Delay Colombian Harvest; Cocoa Prices Advance

- Gold Falls as Some Investors Sell Following Advance to Record-High Price

- Copper for Three-Month Delivery Declines 0.5% to $9,360 a Ton in London

- Minmetals Will Raise Up to $864 Million in Share Sale to Fund Zinc Project

- China Has ‘Pent-Up Demand’ for Sugar, May Buy 1.8 Million Tons, ANZ Says

- Palm Oil Gains After Drop to Lowest Price in Four Months Lures Some Buyers

- Corn, Soybeans May Rise as Wet, Cool Weather Stalls Planting, Survey Shows

- Singamas May Raise Container Prices 11% on Higher Steel Cost, Japan Quake

- Gold-Shortage Threat Drives Texas Schools Hoarding 664,000 Ounces at HSBC

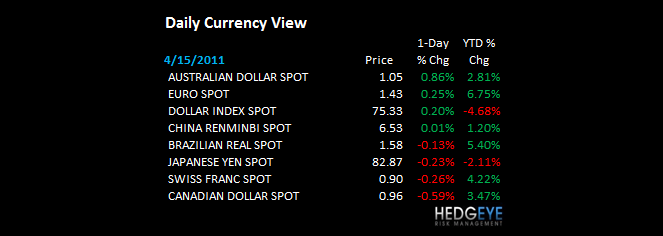

CURRENCIES:

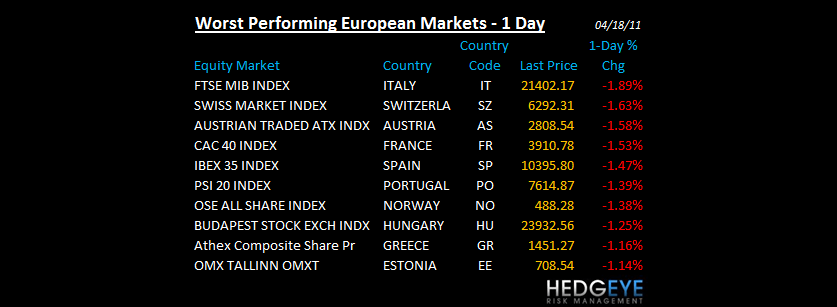

EUROPEAN MARKETS

- Bonello Urges ECB Caution in Raising Rates as Most-Indebted Nations Trail

- European Stocks, U.S. Futures Slide as Banks, Insurance Companies Retreat

- Greek, Portuguese Government Yields Surge to Records on Default Concerns

- Ferrari Should Be Valued at $7.3 Billion in IPO, Marchionne Tells Bankers

- Czech Central Bank Governor Says Mixed ‘Signals’ Are Clouding Rate Outlook

- Allied Irish Swaps Decline on Concern Payout at Risk in Any Restructuring

- France Telecom to Make Joint Purchases With Deutsche Telekom to Save Money

- London Homes' Asking Prices Rise to Record Amid Shortage, Rightmove Says

- Sberbank Joins Credit Suisse to Set Up $1 Billion Investment Russia Fund

- Czech Central Banker Says Preventing Crises by Regulation Is ‘Nonsense’

- BOE Should Maintain Key Rate at Record Low as Recovery Struggles, E&Y Says

- Ruble Eurobond Yield Lowest to Domestic Spurs Second Sale: Russia Credit

ASIA PACIFIC MARKETS:

- China Raises Reserve Ratio to Curb Inflation as Zhou Pledges More to Come

- Most Asian Stocks Retreat on China Policy Tightening Concern; AIA Surges

- BOJ Said to Forecast Inflation Accelerating to 0.5% for Year to March 2012

- G-20 Targets ‘Too Big to Ignore’ Economies as Growth Will Outweigh Shocks

- Hysan Says Causeway Bay Rents to Narrow Price Gap With Hong Kong’s Central

- ‘Ugly’ Inflation Drives Biggest Bond Selloff Since January: India Credit

- China's Huawei Closes In on Ericsson After Revenue Triples Over Five Years

- Kissinger’s ‘Basket Case’ Bangladesh Targets Record Growth in Three Years

- Pimco ‘Open to Adding’ Investments Across Asia as Gross Shuns Treasuries

- Temasek's Mapletree Commercial Raises $718 Million in Singapore Share Sale

- Hong Kong's Home Prices to Drop When Fed Policy Shifts: Chart of the Day

- Hong Kong Canary Singing Commodities Boom Peaking in Aussie Mine: Real M&A

MIDDLE EAST:

Howard Penney

Managing Director