THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - April 12, 2011

As we look at today’s set up for the S&P 500, the range is 17 points or -1.09% downside to 1310 and 0.19% upside to 1327.

SECTOR AND GLOBAL PERFORMANCE

Yesterday, the XLU broke TRADE leaving the Hedgeye Sector models with 8 of 9 sectors positive on TRADE and 9 of 9 sectors positive on TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1180 (-214)

- VOLUME: NYSE 818.71 (+0.36%)

- VIX: 16.59 -7.16% YTD PERFORMANCE: -6.54%

- SPX PUT/CALL RATIO: 1.37 from 1.73 (-20.74%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 23.71 -1.014 (-4.101%)

- 3-MONTH T-BILL YIELD: 0.05% +0.01%

- 10-Year: 3.59 from 3.59

- YIELD CURVE: 2.74 from 2.76

MACRO DATA POINTS:

- 6:15 a.m.: New York Fed’s Dudley to speak in Hong Kong

- 7:30 a.m.: NFIB Small Business Optimism, est. 95.0, prior 94.5

- 8:30 a.m.: Import Price Index, est. 2.1% (M/m), prior 1.4% (M/m)

- 8:30 a.m.: Trade balance, est. (-$44.0b), prior (-$46.3b)

- 9:15 a.m.: Kansas City Fed’s Hoenig speaks on “Too Big to Fail”

- 10 a.m.: IBD/TIPP Optimism, est. 45.0, prior 43.0

- 11:30 a.m.: Fed to sell $40b 4-week bills

- 12 noon: DoE monthly short-term outlook

- 1 p.m.: U.S. to sell $32b 3-year notes

- 2 p.m.: Monthly budget statement

- 2:45 p.m.: Fed’s Fisher moderates panel in Dallas on growth

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- Commodities drop after Alcoa earnings miss.

- Tokyo Electric Power Co. slumps 10% after saying the damaged Fukushima plant my release more radiation than Chernobyl.

- Greek banks fall on concern about the country’s ability to rebound from its crisis.

- IEA Says $100-Plus Oil Price May Be Incompatible With Recovery

- Sokol Spoke With Lubrizol Bankers on Dec. 17: WSJ

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Copper Declines a Second Day on IMF Growth Outlook, Alcoa Sales, Japan

- Japan Rice Buying May Outstrip Supply on Hoarding, Marubeni's Shibata Says

- Rio Tinto's '11 Profits Signal No Boon for Shipping Lines: Freight Markets

- Corn Drops as Feed Millers Seek Cheaper Grain Subsitutes; Soybeans Decline

- Gold May Advance as European Debt Crisis, Conflict in Libya Add to Demand

- Rising Railroad Shipments Reflect Increasing Momentum in U.S. Expansion

- Oil Falls a Second Day as IEA Says High Prices Hurting Economic Recovery

- Rubber Drops From Five-Week High in Tokyo on Oil’s Fall, Growth Concerns

- China May Reduce Export Rebates for Some Metals, Securities Journal Says

- Crop Insurance to Get Boost From New EU Subsidy Policies, Allianz Predicts

- Yellen Says Surge in Commodity Costs Doesn't Warrant Fed Stimulus Reversal

- Europe Commodity Day Ahead: Silver Options Show Bet on Price Drop by July

CURRENCIES

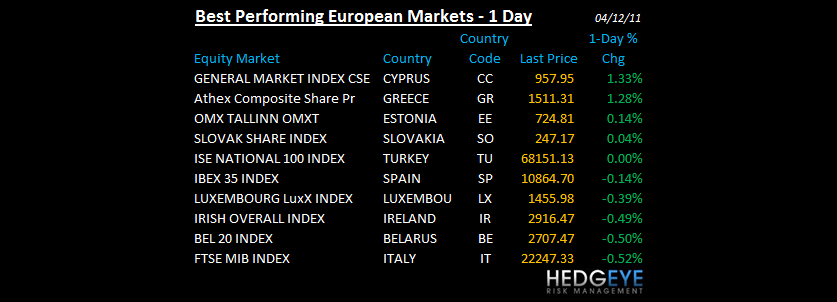

EUROPEAN MARKETS

- Europe markets are trading lower slowing growth and accelerating inflation concerns.

- Germany Mar final CPI +2.1% y/y vs prelim +2.1%

- UK Mar CPI +4.0% y/y vs consensus +4.4%; RPI +5.3% y/y vs consensus +5.5%

- British Retail Consortium March total sales (1.9%) y/y vs prior +1.1%,SSS (3.5%) vs prior (0.4%) worst since records began

- UK Mar house price survey (23) vs consensus (24) and prior (26)

- European Central Bank Governing Council member Michael Bonello says risks to growth outlook remain, in comments at press conference in Valletta, Malta. (1) ECB liquidity may reduce incentive to fix problems; need to embark on more fiscal consolidation; (2) “sovereign debt crisis still not behind us” (3) Oil surge has put pressure on inflation; (4) positive on Spain’s moves

- German investor confidence falls for a second month; German ZEW current conditions index 87.1, est. 85.2; Euro-zone ZEW investor confidence index 19.7, prior 31.0; ZEW says expectations didn’t change significantly after quake; ZEW says economy hasn’t much room for further improvement

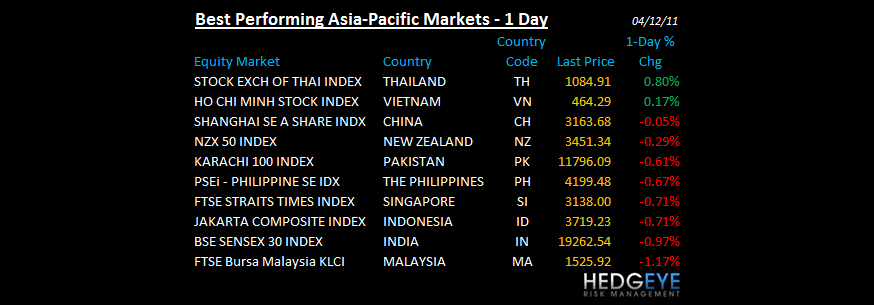

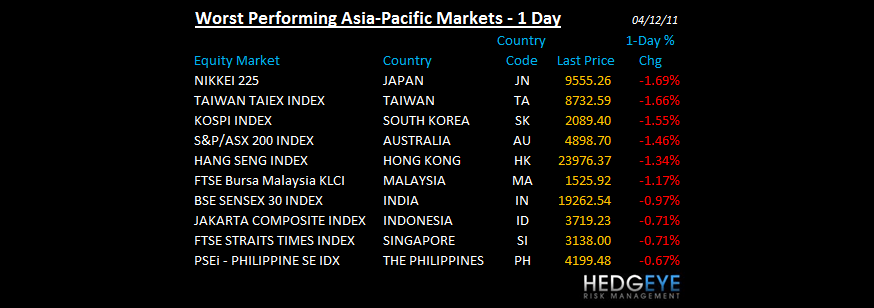

ASIA PACIFIC MARKTES:

- Asian markets went down today, with sentiment dulled by Alcoa’s (AA) unimpressive start to the earnings season.

- Japan raised the severity level of the Fukushima Daiichi nuclear accident to the highest gradation and was hit by two more earthquakes.

- China gave up morning gains and finished flat.

MIDDLE EAST

Howard Penney

Managing Director