“The liquidity gives us these crazy booms, which have many problems as well as virtues”

– Charlie Munger

It was just this time last year that we were preparing for Quad 4 by raising cash levels as we approached the uncompable comps that were created by/during the pandemic.

Now we have our Macro Themes deck next week and are expecting 2023 not to disappoint as the bear market continues to play out. Think, we still get to see the entire FTX situation play out while liquidity continues to be scarce.

I’m going to keep this Early Look shorter than normal, there simply isn’t much new data out there this week.

Although, as companies must go through the reality check that is their balance sheets, let’s focus on the balance sheets of US Commercial Banks and the Federal Reserve to see where the money is going.

Back to the Global Macro Grind…

11 of 11 sectors were down yesterday with Energy down the most. Volume was flat on the day and remains low during the holiday week. We got paid being short in the high yield market this week and broader equity volatility remains in the chop while FX vol accelerated.

Looking at the Risk Ranges in equities, we have both tech and small caps nearing the low end of the risk range. This morning Crude Oil is down -1.3% which will put it in the middle of its Risk Range with downside potential of 5.9% and upside potential of 4.4%.

IVOL Discount Callouts: Brazil $EWZ, Malaysia $EWM, Silver $SLV

IVOL Premium Callouts: S&P $VOO, Nasdaq $QQQ, Russell $IWM, Spain, $EWP, France $EWQ, Germany $EWG, Singapore $EWS, Australia $EWA, India $INDA, Solar $TAN, Defense $ITA, Jets $JETS, Leisure $PEJ, Semiconductor $PSI, Cybersecurity $CIBR, eSports $ESPO, Internet $PNQI, Cloud Computing $SKYY, Blockchain $BLOK, Healthcare Provider $IHF, Medical Devices $IHI, Health care Equipment $XHE, Broker Dealer $IAI, Small cap healthcare $PSCH, Corn $CORN, 5-10yr Corp $IGIB, Intl Bond $BNDX, Convertibles $CWB

That’s your set up for today, now to follow the money:

Starting with the MBS market, US Comm MBS Holdings are down -5% YoY and Fed MBS Holdings are up +2% YoY although down sequentially.

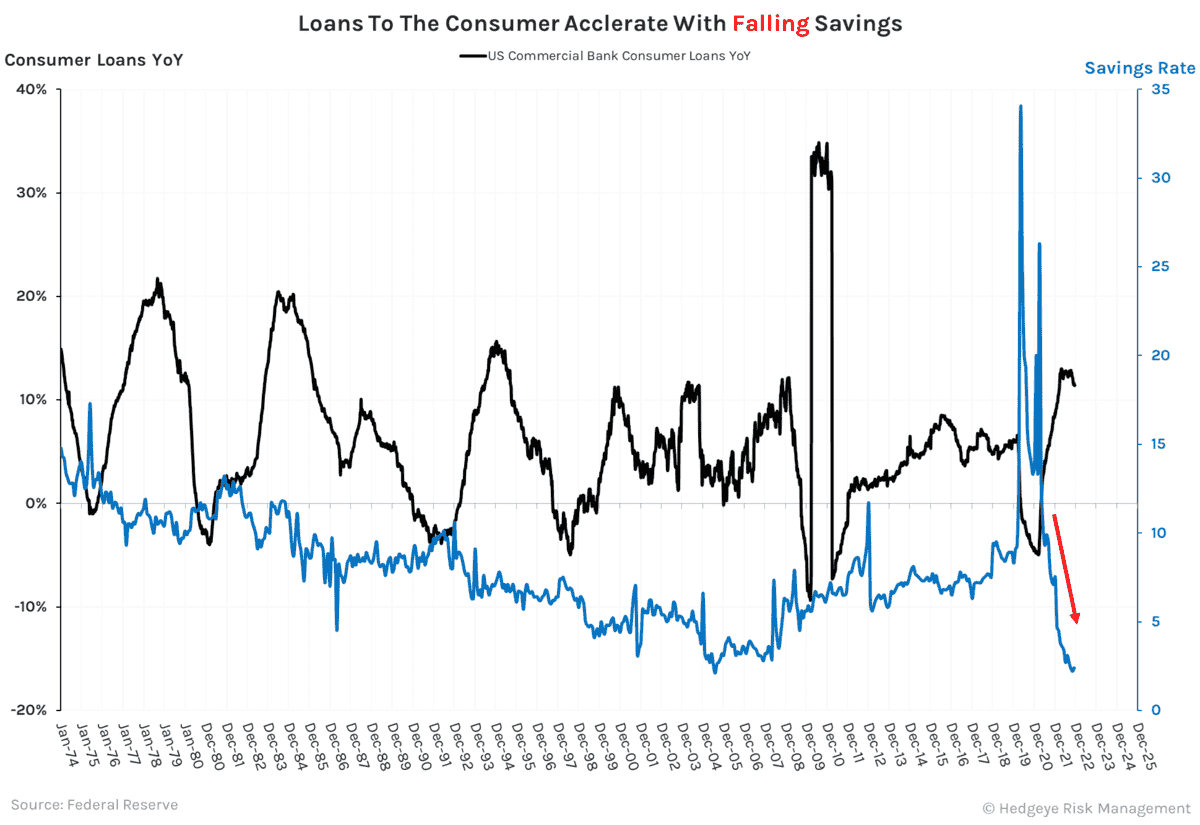

US commercial bank consumer loans remain high although the pace has begun to decrease. This is while your savings rate remains near all-time lows.

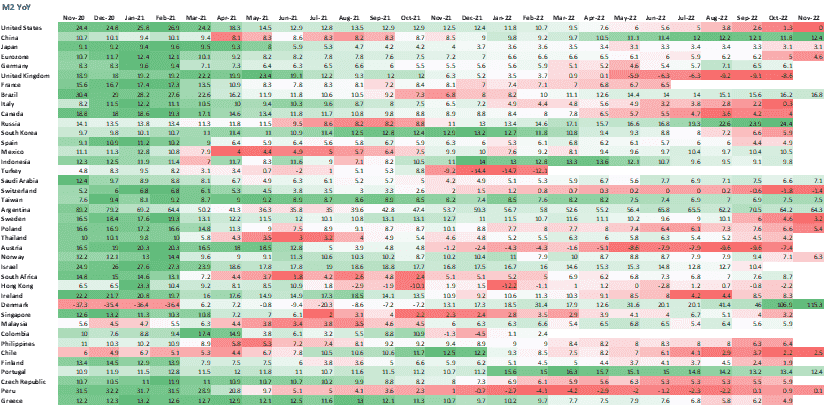

We talked about US M2 yesterday going to 0.0% YoY (an all-time low). Below I’m going to put every country’s M2. They are decelerating broadly with the exceptions being China, Russia, and Denmark.

US commercial bank commercial and industrial loan assets have started to come off its peak rate of change, which historically has meant increased pressure on the labor market.

US commercial bank deposit liabilities came in at -1.0% this week and ON RRP remains at historic levels as investors continue to prefer the overnight markets.

Lastly from the Chart of the Day, the Fed has begun lending. While the absolute amount is not large yet, this is very bearish with the stigma of the Fed being the lender of last resort.

I hope everyone has a fantastic end to their year and continues to risk manage the chop.

Immediate-term Risk Range™ Signal with @Hedgeye TREND signal in brackets

UST 30yr Yield 3.43-4.07% (bullish)

UST 10yr Yield 3.41-3.97% (bullish)

UST 2yr Yield 4.17-4.38% (bullish)

SPX 3 (bearish)

NASDAQ 10,115-10,817 (bearish)

RUT 1 (bearish)

Tech (XLK) 119-128 (bearish)

Consumer Staples (XLP) 73.60-76.01 (bullish)

Shanghai Comp 3006-3136 (bearish)

Nikkei 25,702-27,230 (bearish)

VIX 20.11-25.26 (bullish)

USD 103.41-107.06 (bullish)

EUR/USD 1.031-1.067 (bearish)

Oil (WTI) 72.97-80.77 (bearish)

Gold 1 (bullish)

Silver 22.89-24.76 (bullish)

TSLA 99-136 (bearish)

Bitcoin 16,121-17,198 (bearish)

Ryan Ricci