The Gasoline tailwind (BJ, KR, COST)

Several food retailers benefited from an unusual source in 2022, their gasoline retail businesses. Many food retail chains operate a gasoline retail business to drive traffic to their stores, treating the business as low margin marketing. The margins are particularly low because the retail sales price is set to be below the nearby competition in order to drive traffic. Gasoline prices surged as the economy recovered from the pandemic. Consumers reacted by purchasing more of their gasoline from discount retailers like food retailers.

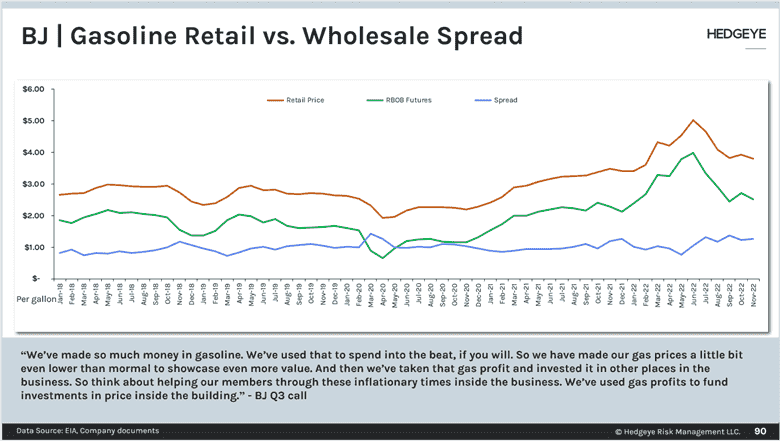

Due to several factors in oil refining, the spread between wholesale and retail prices widened providing another boost to the gasoline retail business.

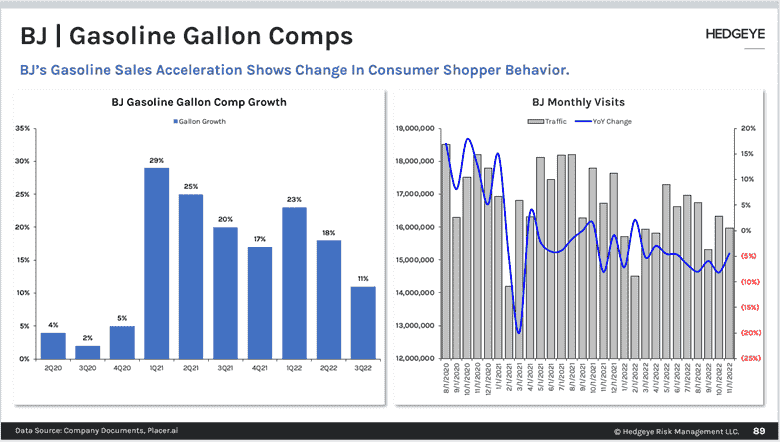

We added BJ’s Wholesale Club to the short side because our calculations suggest its gasoline business accounted for more than half of the company’s gross profit growth over the past year. BJ’s was not the only food retailer to benefit. Kroger’s fuel margin per gallon increased 33% through the first three quarters of this year compared to the first three quarters of the prior year. The profitability of the gasoline business tends to revert over time as it is a competitive commodity business. The gasoline business is also not a core segment that the food retailers even try to improve profitability, accepting its commodity nature. The business is run to generate traffic making it likely that the profitability will revert in the near future. We hosted our 2023 outlook call for the food retailers yesterday. We went into more detail about the benefit that the gasoline business had in 2022 and what that means for growth rates in 2023.

|

For the Food Retailers 2023 Outlook Call Replay & Slides CLICK HERE |

High bar or bad pets? (GIS)

General Mills reported FQ2 EPS of $1.10, above consensus expectations of $1.07. Sales grew 4% with a 1% headwind from Fx and a 5% headwind from divestitures. Organic revenue grew 11%, exceeding consensus expectations of 9.6%. Organic price/mix increased by 17% while organic volumes decreased by 6%. North American FoodService grew 17% leading all segments while the Pet segment was flat. The Pet segment was negatively impacted by inventory reductions at key retailers. Retail sales grew HSD% while retailers targeted lower inventory levels. North America Retail drove FQ2 results with organic sales growth of 13% and operating profit growth of 24%. Cereal lapped difficult comparisons against Kellogg’s labor strike last year. International organic sales grew 5% while operating profit decreased 68% due to higher input costs, weakness in China, divestitures, and an ice cream recall.

Each segment exceeded expectations except for Pet, which saw operating profits fall 34% due to lower shipments, higher input costs, supply chain disruptions, and increased marketing. Management expressed confidence in Pet recovering in the 2H as retail orders stabilize.

Gross margins expanded 100bps YOY and were 60bps above expectations. Price increases and a higher product mix offset mid-teens input cost inflation and supply chain deleverage. Input cost inflation is expected to be +DD% in the 2H. Input costs are seeing disinflationary trends, but management has not signaled a hesitation to pass on price increases. Operating margins expanded 60bps YOY.

Management raised guidance for organic revenue, EBIT, and EPS. Organic revenue is now expected to grow 8-9% from 6-7% previously. EBIT is now expected to grow 3-5% from flat to +3% previously. EPS is now expected to grow 4-6% in constant currencies from 2-5% previously. Over the past year, General Mills’ quarterly beats did not lead to sell-offs, but we do not expect the FQ2 results to mark a change in trend despite the recent share outperformance. General Mills has been a Best Idea Long for us during much of Quad 4. FQ2’s beat and raise and the recent challenges in the pet business do not change our positioning.

Oat milk brand purchase (STKL)

AG Barr acquired the remaining 38.2% of Moma Foods for €3.4M. It purchased the other 61.8% last year with a three year option to purchase the remaining shares. Moma Foods offers a range of oat-based porridge and drinks. The brand's products are available in supermarkets throughout the U.K. This year Moma’s Whole Oat Drink won the Grocer New Product Award for the dairy-free category. Moma’s founder said, “We’re 100% focused on crafting oats into the tastiest food and drink products we can, and I’m looking forward to the next leg of our journey.” Oat milk continues to be a category of non-dairy milk that attracts new investment. The investment and innovation have helped oat milk gain share at the expense of dairy milk which is at a disadvantage in marketing and innovation. SunOpta is a supplier to numerous plant-based milk brands. It is in the process of opening new capacity to keep up with the category’s growth.