Notable news items and price action from the past twenty-four hours.

- Goldman’s 2011 GLOBAL PROTEIN CONFERENCE (8:00am TSN, 8:45 SFD, 9:45 PPC, 10:30 SAFM)

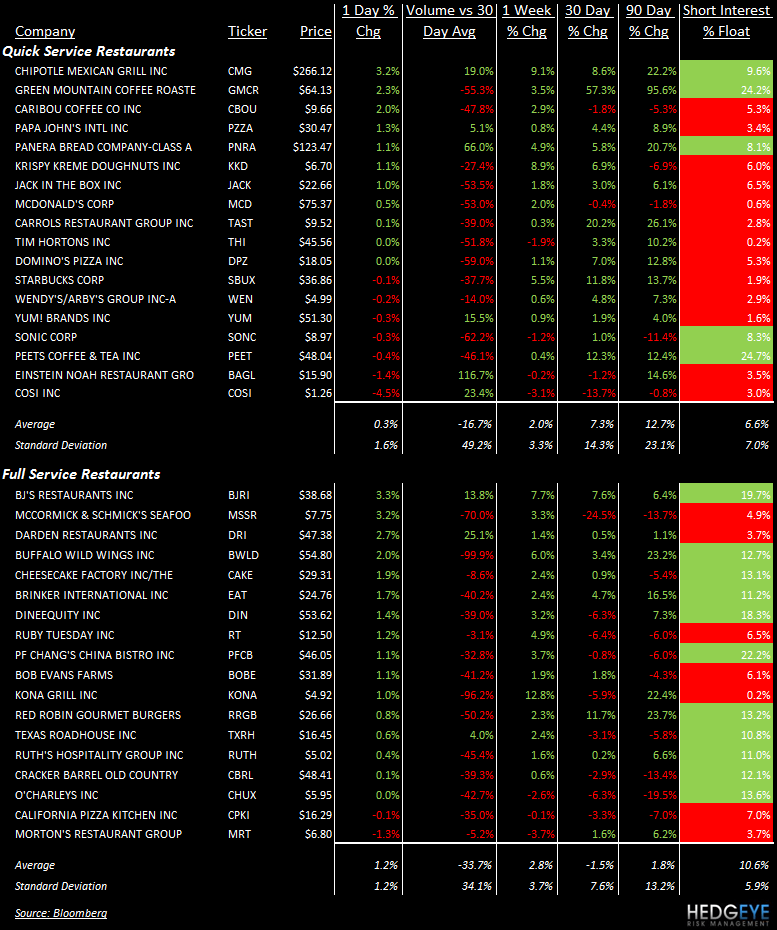

- PEET was raised to neutral from sell at Janney Capital.

- DPZ UK - Sales +11.2% y/y to £132.3M; SSS +4.2% - company notes that total SSS is impacted by the performance of the Republic of Ireland stores where trading conditions have continued to deteriorate during the period; Ireland comps are (10.5%), while UK comps are +5.5% (7.8% excluding VAT increase).

- DRI - The slowdown in The Olive Garden sales trends appear to more secular that the company may have suggested on last week’s conference call. DRI announced today that 700 Olive Gardens will be remodeled by June 2013. Is the company playing offence or defense?

- DIN has seen 40 of its IHOP restaurants change hands from Quantum Management to private investment firm Argonne Capital Group.

- The number of announced job cuts fell in March to 41,528, down from 50,702 in February. Cuts during the first quarter of 130,749 were at their lowest since 1995.

Howard Penney

Managing Director