“A good player plays where the puck is. A great hockey player plays where the puck is going to be.”

-Wayne Gretzky

Just over three years ago, we started Hedgeye with the philosophy that the research business should be transparent, accountable and trustworthy. At the time, many of our Old School Wall Street critics derided us for naively entering the investment research business with a simple philosophy. Needless to say, three years, forty five employees, and hundreds of clients later, Hedgeye isn’t such a novelty. Neither are our core values.

We’ve made a few enemies amongst the Old School Wall Street crowd over the course of the past few years, but we’ve made many more new friends, some of whom we are now honored to count as subscribers to our research. Yesterday, it seems, we made a new enemy in Peter Boockvar, the Sales Trader /Equity Strategist from Miller Tabak. Boockvar, it seems, is not so crazy about transparency.

At Hedgeye, we are fond of an expression called “YouTubing”. This expression means to analyze and, sometimes, critique, the public comments of politicians, executives, and market commentators. “YouTubing” is not meant to be a personal attack, but rather a critique related to the substance of those views articulated. In the Web 2.0 world, if you make public comments, you should expect to be “YouTubed”. As a firm, we make many public comments, and fully expect to be held accountable to them.

Intraday yesterday Keith tweeted the following via @KeithMcCullough:

“If Boockvar is long Nikkei and short Yen here, now he knows why no one will ever give him money to manage”

This was in response to an appearance by Boockvar on CNBC yesterday, where he discussed his case for Japan. That video is here:

http://www.cnbc.com/id/15840232?video=3000010657&play=1 (if the link doesn’t open, copy and paste it into your browser)

A paraphrase from his appearance was:

“Japan is going to want to print their way out of this. Therefore you want to be long their equities, and short their currencies and short their bonds.”

It seems Boockvar’s thesis is that printing money will lead to increasing interest rates in Japan, which will lead to an increase in Japanese equities. In fact, he also made a bullish call on Japanese equities on December 31st, 2010 on CNBC, which he articulated in this clip:

http://seekingalpha.com/article/244389-peter-boockvar-says-buy-japanese-equities (if the link doesn’t open, copy and paste it into your browser)

Thesis drift, anyone?

Needless to say, Boockvar’s response to Keith’s public critique was less than hospitable and was topped off by calling Keith some not so nice names in a private communication. Boockvar’s use of schoolyard epithets does nothing to enhance his professional standing in our eyes. Now, we don’t mean to pick on Boockvar, he just typifies a gang we call Old School Wall Street, and this is just the latest example of how rattled they get by real-time accountability. Twitter on!

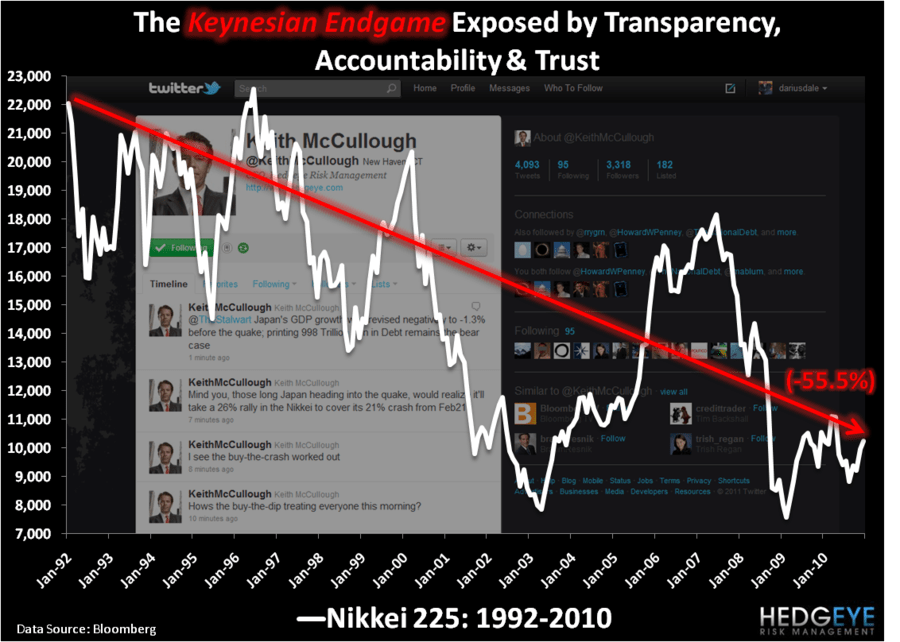

Since articulating a coherent view in 140 letters on Twitter can be challenging, we want to restate our position on Japan. Our bearish view on Japan is something we began articulating in Q4 of 2010, in a thesis called Japan’s Jugular. A key highlight of this thesis is, in contrast to Boockvar’s view, that printing money will have just the opposite impact. It will lead to increased debt, slowing growth, and declining equity prices. In fact, in 18 years of Keynesian experimentation, from 1992 to 2010, Japan had on average +0.85% year-over-year GDP growth. Over the same period, the Nikkei 225 returned -55% No, Mr. Boockvar, this time is not different . . .

Naturally any good contrarian is looking for a buying opportunity given the dramatic sell off in Japan over the past few days. We would caution against this, despite the relief rally this morning, for two reasons:

- Unknown unknowns – The derivative impact of the earthquake has been damage to the nuclear power infrastructure in Japan. At this point, there is limited information from which to evaluate the real impact of this damage, in particular at the Fukushima Dai-Ichi plant, where this morning it was reported that a second reactor may have ruptured. The point is, we have no idea how this will end and be resolved.

- Known knowns: The Japanese economy reached a negative inflection point last year when its pension plan began selling assets to fund pension obligations. This highlights two key components of our negative thesis on Japan: demographics and debt. Japan has both the oldest population in the world, with ~22.7% of the population 65 years of age or older, and is the most indebted developed nation, with a debt-to-GDP ratio of 205%+. The risk is that this tragedy only accelerates negative growth in Japan due to an inflexibility created from almost two decades of Keynesian policies.

Of course, there will be an opportunity to get long the Japanese recovery trade eventually. As always, duration matters; however, after the January 17, 1995 Kobe earthquake, Japanese equities lost (-24.7%) before bottoming out nearly six months later on July 3. The Nikkei 225 did not break even until nearly 11 months later on December 7 of that year.

Now a public service message to Peter Boockvar and Friends:

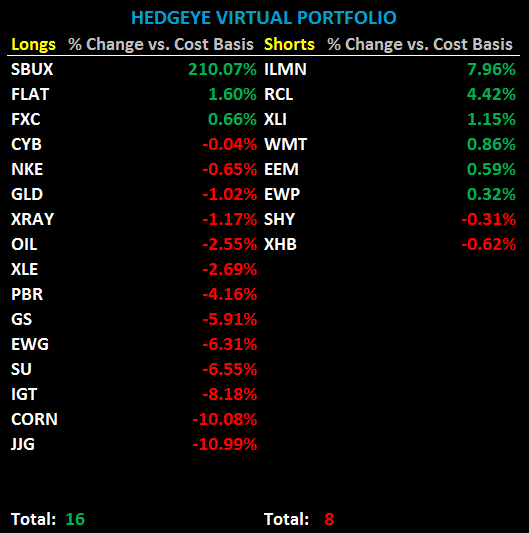

This is the new Wall Street where accountability and transparency matters. While your long term track record is cool, let’s just start with the last three years. For the record, every single position we’ve take in the Hedgeye Portfolio since inception is on our website for the world to see. We encourage you to do the same.

Next time you want to challenge someone to head down to the schoolyard for disagreeing with your thesis, add me to that list. My email is . My friends call me Big Alberta, and I’ll be waiting at the puck for you.

Keep your head up and stick on the ice,

Daryl G. Jones