This note was originally published at 8am on March 08, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Tis one thing to be tempted, another thing to fail.”

-William Shakespeare

I sold my long positions in oil (OIL) and Brazilian oil giant Petrobras (PBR) on yesterday morning’s opening market strength. This doesn’t mean I am not bullish on either (in the Hedgeye Portfolio we are still long China National Offshore –CEO, and Suncor -SU). This simply means that my risk management model was calling them both out as immediate-term overbought.

Overbought is as overbought does. Sometimes my risk management signals are wrong. Most of the time they aren’t. Temptation is always there to violate my investment process. Most of my big mistakes are a direct function of giving in.

What if I gave into consensus on February the 18th and bought the SP500 at 1343? What if I gave into the Temptation of The Flows into US and Japanese Equities that peaked in the same week? What if I saw the hedge fund community’s highest net long position in bullish oil contracts yesterday (highest since 2006) and decided to ignore my risk management signal on the oil price?

“What if” may be an acceptable strategy for someone living in the theoretical. In this globally interconnected game of decision making however, there are no “what ifs.” There are players and pretenders. There are wins and losses.

Subliminally, I may have learned this risk management process from my Dad. Whether it was in his profession as a firefighter or in the game of life that he coached me – somewhere along the line I learned that we are all accountable for the decisions we make in this life and how those decisions affect others.

While I highly doubt that the US Federal Reserve is going to be sourcing risk management lessons from a few Canadian Bears on the topic of accountability, maybe they’ll re-read this quote about Temptation from their Maestro of ideological groupthink gone bad:

“The temptation is to step on the monetary accelerator or at least to avoid the monetary brake until after the next election… giving into such temptations is likely to impart an inflationary bias to the economy and could lead to instability, recession, and economic stagnation.”

-Alan Greenspan, 1993

Again, like any good Fire Chief or Global Macro Risk Manager, you should re-read that quote slowly. And read it again. While there is a Temptation to scan for headlines about some Libyan nut-job as opposed to understanding the long-term structural underpinnings of the The Inflation, it always pays to take the time to make the highest probability decisions based on the best information you have.

That Greenspan quote was highlighted by the late Austrian economist who I have cited recently - Murray Rothbard. Later on in his book, “The Case Against The Fed”, this is what Rothbard had to say in order to contextualize The Inflation that the Fed perpetuates:

“We are now so conditioned by permanent price inflation that the idea of prices falling every year is difficult to grasp. And yet, prices generally fell every year from the beginning of the Industrial Revolution in the latter part of the 18th century until 1940, with the exception of periods of major war.” (page 21)

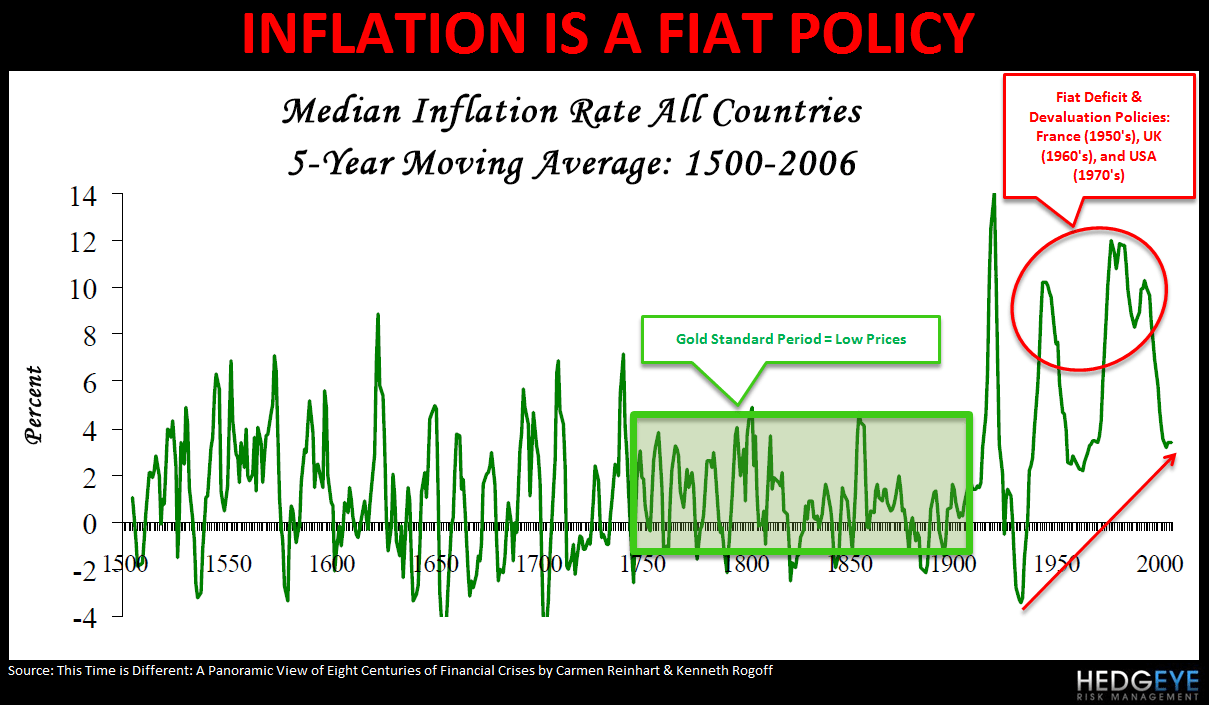

Interestingly, Rothbard published this book in 1994 and passed away in 1995. Since, the American financial system has learned virtually nothing from these types of risk management perspectives. That’s because the modern day US Empire of Fiat Finance is grounded in a policy to inflate the stock market (see the inflation chart below dating back to the year 1500).

Can our industry or America’s conflicted and compromised politicians handle a deflation of inflated prices? Can they handle a reflation of the price of a Debauched Dollar? I think the answer to those questions is as clear as Americans living on entitlement goodies - many have a patriotic answer about debts and deficits, but they lack a pragmatic plan; particularly if the plan hits them in the wallet.

To be crystal clear on this, if I was damned into the job of Chief Central Planner in this country, this is what I would do:

- Raise interest rates

- Cut entitlement spending

- Strengthen the US Dollar

Points 1 and 2 address both monetary and fiscal policy head on. Point 3 would be the effect. Going back to the following experiences:

- 1950’s-1960’s France and Britain

- 1970’s United States of America

- 1990’s Japan

There hasn’t been a modern economy that has devalued its way to prosperity by debt financed deficit spending.

The Temptation is to create massive US Dollar denominated correlation-risk (USD inverse correlation to the price of oil is currently -0.93) that all interested inflation policy parties can blame on the Middle East or “global supply and demand imbalances” if unwound.

But be careful on that Temptation because it creates expectations. We Expect Price Volatility, not Price Stability. That’s why small business owners like me won’t jump in with both feet and start hiring aggressively. Anyone who has to meet a payroll in this country gets it – our medical and employment costs are rising as economic growth slows. As Greenspan reminded the Keynesians in 1994, that’s what The Inflation does.

Thankfully, one voting member of the Federal Reserve had the political spine to call this like it is yesterday. Dallas Fed President Richard Fisher told the Institute of International Bankers in Washington, DC that “the liquidity tanks are full, if not brimming over.”

Indeed Mr. Fisher. Indeed. That’s what printing money with an inflation policy achieves. It’s time to get out of the way, let the US Dollar strengthen, and the price of oil deflate.

My immediate term support and resistance levels for WTI Crude Oil are $101 and 107, respectively. My immediate term support and resistance levels for the SP500 are now 1297 and 1315, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer