"The rotten tree-trunk, until the very moment when the storm-blast breaks it in two, has all the appearance of might it ever had."

– Isaac Asimov

I recently traveled to Alaska with the family and had the opportunity to ride the White Pass & Yukon Route Railway in Skagway. If you’re ever up that way, I would highly recommend it. The scenery truly is breathtaking.

Interestingly, the entire train ride is narrated, and you learn about the history of the Klondike Gold Rush, the arduousness of the trek (pre-railroad) just to get to the “gold fields”, what ultimately became of most prospectors, and, most interestingly for me at least, what prompted it all (aside from the gold).

Built in 1898 to enable Klondike prospectors an easier trip up the White Pass, the Railway is a seemingly simple 20-mile up, 20-mile down trip (with 3,000 feet of elevation gain along the way). While it only took our train an hour and a half to make the 20-mile climb, it took pre-railroad prospectors carrying all their gear fully 1-2 months to traverse the same terrain. This was in part because of the difficulty of the terrain and in part because the Canadian authorities (the Klondike was in the Yukon) required them to bring one year of food with them to prevent starvation. This resulted in the gear each prospector needed to carry weighing close to one ton, and thus being carried over multiple stages/trips. Once prospectors reached the summit, another 20-mile hike awaited them, followed by a 500-mile Yukon River trip through numerous rapids before finally arriving at the Klondike gold fields. Once there, things only got tougher.

Sadly, of the ~100,000 would-be Klondike Gold Rushers, only around 10% ever even reached the gold fields – the trip was thousands of miles for most, with just 10% of those ever discovering any gold at all, and just a small fraction of those finding enough gold to call the endeavor a success. Finally, just a handful of those prospectors ever left the gold fields with enough gold/money to invest in businesses back in the lower-48. In other words, the odds of striking it rich in the Klondike Gold Rush and returning home with the spoils were only moderately better than hitting Powerball, but the cost of buying the ticket was far greater. By the time of the Railway’s completion in 1898, the Klondike gold rush was nearly over as a new gold field had been discovered on Alaska’s West Coast.

One part of the story I didn’t understand was why. Why would so many people trek so far for such a low probability outcome? The answer was that the discovery of gold in the Klondike in 1896 coincided with the third year of the ongoing Great Depression (1) sparked by the Panic of 1893 – the worst Industrial Depression of the 19th Century. While national records were sparse, it is estimated that unemployment reached 20-25% and in New York over 35%. The Depression lasted a full four years, ultimately prompting many able-bodied individuals to pack up and leave when they heard about the new Gold Rush, choosing a low probability high-payoff over a high probability low-payoff (unemployment with no light at the end of the tunnel).

Back to the Global Macro Grind…

There was no Federal Reserve in the 19th century – it didn’t come along until 1913 in the wake of the Panic of 1907. Prior to the Panic of 1893, there was the Panic of 1873, which was called the Great Depression. The Panic of 1893 was far greater than that of 1873, and so it became known as the Great Depression. Ultimately, the Panic of 1907 dwarfed even the Panic of 1893 and then it became the Great Depression …. until the 1930s came along and became the Great Depression we think of today. Prior to the Fed’s creation, there were regular and frequent bank runs and panics. In addition to there being no central bank, there was no deposit insurance – not until 1933. So, when banks failed – a frequent occurrence during the Panics of the 19th and early 20th century – savers frequently lost their life savings. It makes sense – there’s no safety net, so the first ones to get their money out of the bank won. Classic reflexivity.

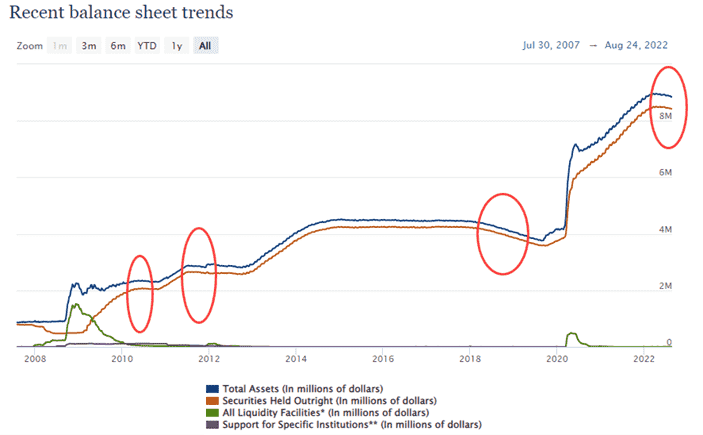

Today, we have the Fed and we have the FDIC. That makes the game different, but different in a different way. The reason I bring up the Federal Reserve is that tomorrow will bring us into a new phase in the Fed’s Quantitative Tightening program. Specifically, beginning in September, the Fed will begin running down its securities holdings by ~$95B/month, or double the pace of that which began in June (but really began in November 2021 at the start of the QE Tapering). It’s worth noting, however, that in the eleven weeks since the start of the June, the Fed has only reduced its holdings by $52B in total, or roughly $17B/month. In other words, the pace of runoff from here is going to climb not by twofold, but by roughly five-to-six-fold beginning tomorrow.

Why should we care? Because today the game is different.

Consider the following:

- The high watermark in risk assets occurred in early-to-mid November last year. What else happened around that timeframe? The first step-down in Fed purchases from $120B/mo to $105B/mo. In fact, the timing coincidence was uncanny. The Nasdaq Composite peaked on November 18th and the first step-down in purchases occurred on November 15th.

- QE1 concluded on March 31, 2010. The S&P 500 and Nasdaq Composite peaked on April 23, 2010, just three weeks later.

- QE2 concluded at the end of June 2011. Both the S&P 500 and Nasdaq Composite peaked over the following two weeks.

- Post QE3, from Fall-2014 through Mid-2016, the Fed’s security holdings remained largely unchanged. Over that same timeframe, the S&P 500 remained largely unchanged.

- QT – Oct 2017 – Dec 2018 saw a not insubstantial wind-down on the Fed’s securities holdings – a decline of around 15% all told. Over that comparable time, the S&P 500 was largely sideways and only resumed it uptrend over 2019 once the Fed announced it was ending its QT.

So, as a reminder, the Fed has QT’d to the tune of $52B in total over the last 3 months (a ~60bps reduction in its securities holdings) and the S&P 500 is down ~4.1% over that timeframe. In the four months between now and year-end the Fed is supposed to QT by $380B, a roughly 450bps reduction in securities holdings.

Still feeling bullish?

Immediate-term Risk Range™ Signal with @Hedgeye TREND signal in brackets:

UST 10yr Yield 2.83-3.17% (neutral)

UST 2yr Yield 3.18-3.49% (bullish)

High Yield (HYG) 74.44-77.90 (bearish)

SPX 3 (bearish)

NASDAQ 11,653-12,594 (bearish)

RUT 1 (bearish)

Tech (XLK) 133-144 (bearish)

Utilities (XLU) 74.49-78.20 (bullish)

Healthcare (PINK) 24.50-26.60 (bullish) `

Shanghai Comp 3175-3270 (bearish)

Nikkei 27,707-29,200 (bullish)

DAX 12,701-13,504 (bearish)

VIX 20.35-28.26 (bullish)

USD 106.60-109.87 (bullish)

EUR/USD 0.989-1.014 (bearish)

Oil (WTI) 87.27-97.11 (bearish)

Nat Gas 8.68-9.82 (bullish)

Gold 1 (bullish)

To your continued Success,

Josh Steiner

Managing Director

Source: Federal Reserve