Conclusion: We do not see a buying opportunity of Turkey’s equity market given looming energy uncertainty.

Positions: Short Emerging Markets via the etf EEM and Brazil (EWZ)

Turkey’s main equity index, the ISE 100 got crushed yesterday, falling -4.2%, while the etf TUR fell -5.5%. Today the ISE is trading flat, however we caution that one main factor that may significantly influence Turkey’s overall equity performance is its dependence on foreign energy.

To meet its consumption needs, the country imports ~ 93% of its oil and ~ 97% of natural gas, according to the EIA. While Turkey receives economic benefit as an important energy transit state (with supplies originating in Russia, the Caspian Sea region, and the Middle East for delivery primarily in Europe), the fact remains that given the present uncertainty in the oil producing nations of the Middle East and North Africa (MENA) and Turkey’s extreme foreign energy dependence, Turkish stocks should continue to underperform so long as global supply and production remain uncertain.

A look under the hood (and as the charts below present), recent Turkish fundamentals show:

1.) Growth Slowing - GDP has slowed sequentially over the last 3 quarters, with difficult year-over-year comps from here on out. Turkey is clearly one country that has been the recipient of the pullback in the emerging market trade over the 6 last months. We’re explicitly short the emerging market via the etf EEM and Brazil (EWZ) in the Hedgeye Virtual Portfolio.

2.) Inflation Slowing – bucking the trend of most global economies, inflation (as reported by the CPI) has slowed in Turkey over the last 4 months on a year-over-year basis. As the chart below shows, comps will remain difficult for much of 2011, so CPI may decline over the next months. However, our focus is on the country’s primary tax, energy, especially given the prospect for further unrest from its suppliers, and therefore higher prices. We’re less concerned about possible declines in the headline CPI number, for now.

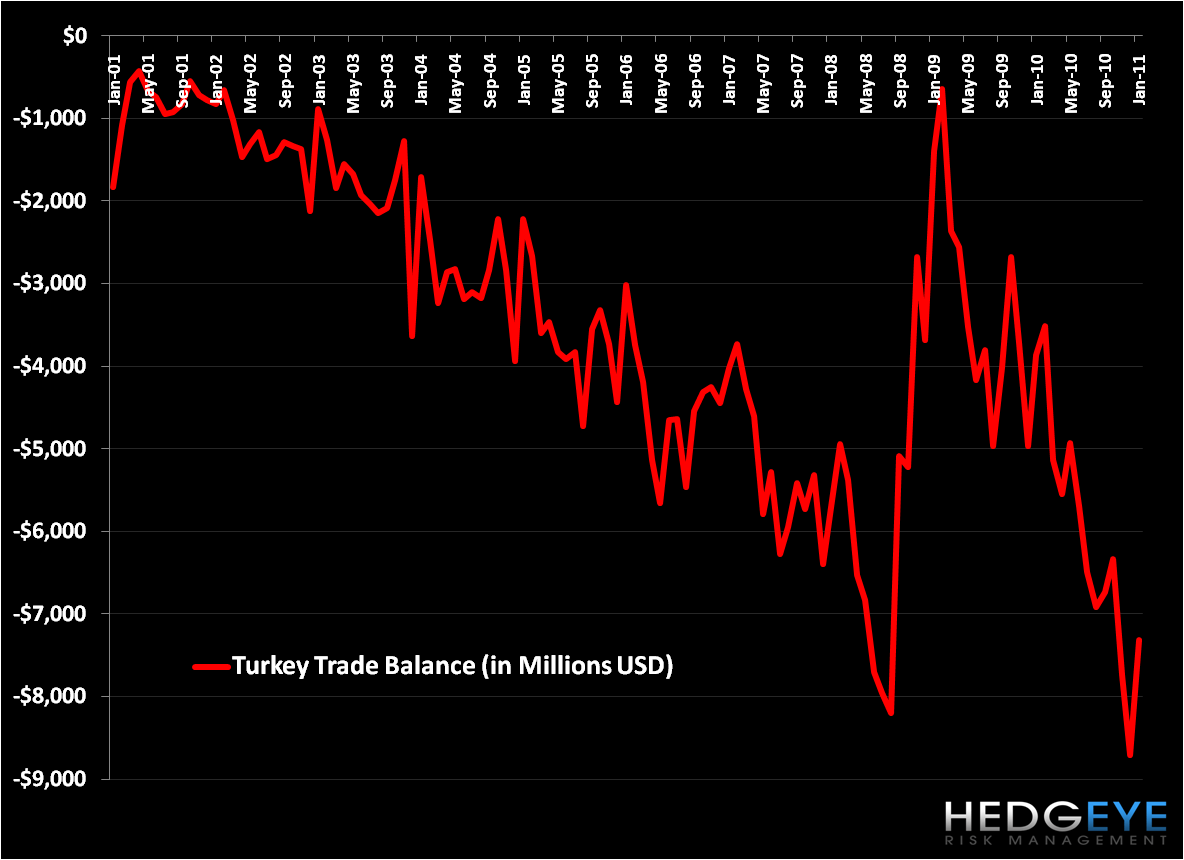

3.) Trade Deficit Widening – The country ran a trade deficit of -$7.3 Billion in January. While the country has consistently run a trade deficit over the last 10 years, the trend is widening, and is certainly one macro factor that will eat into overall growth. 50% of its exports are destine for Europe (in particular Germany, France, Italy), arguably a relatively stable market. However almost 30% are destine for MENA, and obviously the demand from this region is a huge unknown. [For reference, manufacturing is the country’s largest component at 91.7% of total exports].

In reference to today’s Early Look penned by my colleague Daryl Jones, Turkey also has a relatively young population, with median age of 28.5 years (World median = 28.4 years), according to the CIA Factbook. Currently, total unemployment in Turkey is 11% and local purchasing power is down with the Turkish Lira down -16% vs the USD or -15% vs the EUR since a high on 11/4/10. Surely it could be argued that Turkey has a more stable government than many in MENA and therefore is less likely to see uprisings. That withstanding, from a market perspective we think Turkey has more downside risk than upside potential so long as the fate of rulers and governments throughout MENA remain uncertain.

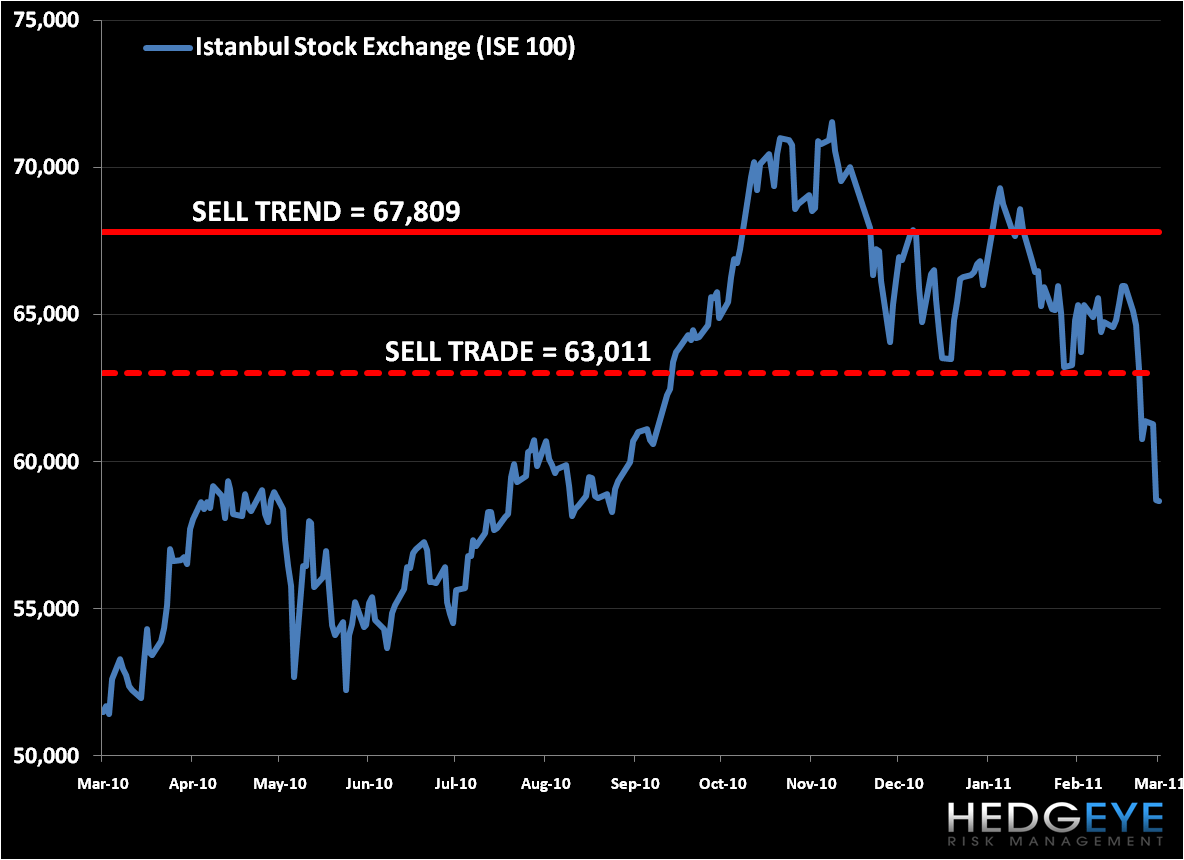

Therefore, we do not see yesterday’s pullback in the ISE as a buying opportunity, and think the index, which is down -18% from its top on 11/9/10, could fall further. We’re also taking risk management cues from rising CDS spreads (Turkish CDS is on a steady rise since Oct. 2010 and currently at 175bps) and rising yields (Turkey’s 10YR government bond yield has blown out since the beginning of the year, currently at 9.5%) . In the last chart below we show our resistance levels on the ISE.

Matthew Hedrick

Analyst