We’re making some major positioning changes ahead of our Mid-Quarter Themes Presentation on Wed at 2:00pmET, where we’ll go through the state of the consumer, retail earnings revisions (reported and those to come in Aug), the setup into 4Q and 2023, and ultimately where to be long and short. Out of the 17 moves on our Position Monitor this weekend, only two of them are bullish – which is a pretty major statement as to how we’re looking at the recent market melt-up.

To access the event on Wed at 2:00pmET click the following link for video presentation details and accompanying slides.

Live Video Link CLICK HERE

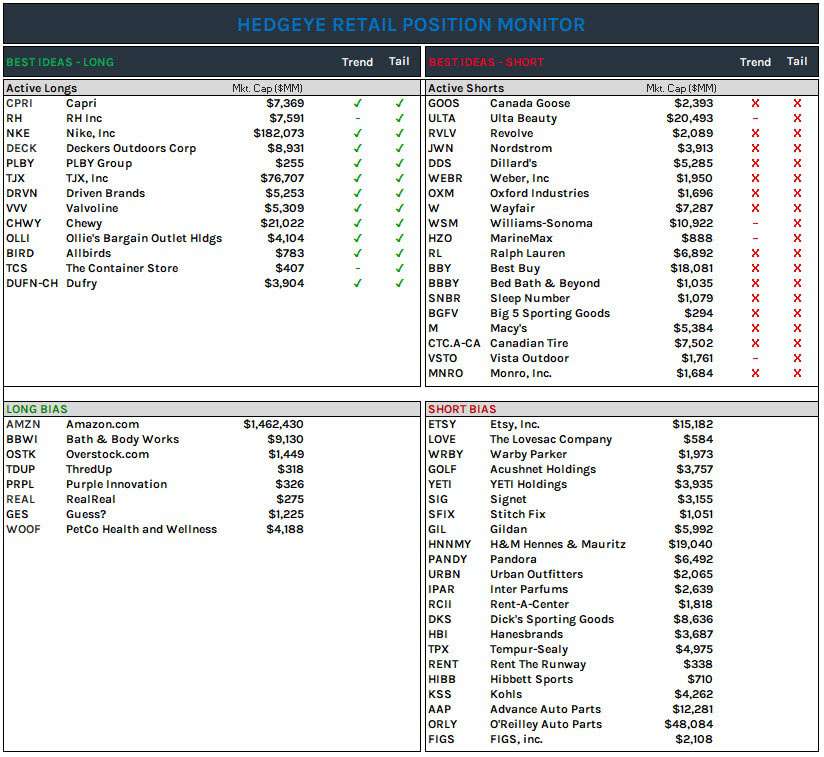

17 POSITION MONITOR CHANGES FOR THE WEEK

Caleres (CAL) | Coming off Best Idea Long list. We went long this name in March of last year at ~$17, and it’s now sitting 75% higher with the tape up 11%. Our call on this name was predicated upon our view that The Street’s models were asleep at the switch, looking for just $1.70 in EPS vs our model of $4.00+. Numbers have since raced up to $4.34 for FY23 (Jan) – so the Street has officially caught up – and then some. The stock is still cheap at 7x earnings and EBITDA – but we were looking at about a 3.5x multiple when we made the call – which was simply a lay up in the face of what we knew would be a massive positive earnings revision. Today, we’re at a point where the footwear category is slowing on the margin, and the retailers are going to have to take it on the chin with promotional activity – and CAL’s Famous Footwear is not immune. We’ll book the win, and revisit on a downward revision. We still think this company should be taken private…but it has a lot more competition in the ‘take-private’ arena today.

Nike, Inc (NKE) | Moving up to #3 on Best Idea Long list (behind CPRI and RH). Yes, the footwear category is slowing, but we don’t think that anyone sent that memo to Nike. It’s done pulling back wholesale distribution from ‘marginal’ retailers, and will begin to grow with those that ‘made the cut’ in 2H. Will those retailers have to promote product at a more ‘normal’ (ie less than last year) cadence? Yes. But Nike won’t share the promo pain, and should see a top line acceleration. Our sense is that its clearance event last quarter in China was the right move, and we should see an acceleration in that key Region in the September print. For the year we’re coming in at $4.25 to the Street’s $3.75, and build to near $7 in EPS power over a TAIL duration – suggesting a mid-teens multiple on underlying earnings on a name today that is trading at 29x the Street’s (wrong) numbers. We think this name is a 2-3 year double as margins go from 14% to near 20% on double digit annual sales growth. Our only concern is that it pulled back too much on wholesale – that helps near term – but could create a stronger competitive set (HOKA, Allbirds, On Running) 3-5 years down the road. We’ll cross that bridge when we come to it.

DUFRY (DUFN-SW, DUFRY) | Taking this name materially down on our Best Idea long list, for now. We still like the idea as an outstanding play on travel recovery, and a growth engine in Hainan. We’re also a fan of the Autogrill deal – but need to re-trench on the research effort on the real underlying earnings and cash flow characteristics of this new travel retail behemoth. If we were to isolate one reason we’re taking it lower it’s that the new CEO, by way of this deal and by putting his own mark on the company, appears to be backing away from the CH400mm in cost cuts – something that was one of the pillars of our call on stand-alone DUFRY. His company, his transformative plan, and his choice to seemingly ditch the cost promised by his predecessor. As we do the work, the synergies with airport operators appear to imply a 2-3x stock price over a TAIL duration. Translation – this is still a big idea. But if there’s one thing we won’t underwrite is ‘thesis morph’ – justifying a previously made call when a change in company strategy is so clearly altering the future of this company. We’re deep in the research today, and are likely to present a Black Book in September on where we stand on the merged company. We think there’s little risk to owning the name until then, so we’d continue to own it. We just need to assess how much upside we’re actually playing for. Stay tuned.

Decker’s Outdoor (DECK) | Moving Higher on Best Idea Long list. The latest DECK print was yet another sign on the road to up our confidence that this is a Best Idea Long with a view that it is a TAIL double. Impressive headline beat of $1.66 vs our estimate of $1.55 and the Street at $1.21. As we expected, the beat was entirely top-line driven, with total sales up 22% -- slightly better than our above-consensus model -- as HOKA put up a blistering top line growth rate of 55% -- on top of 100% growth in last year’s first quarter. Based on next year’s numbers, we get to a value of HOKA alone of $370 per share, compared to today’s price for the entire entity (including Ugg, Sanuk and Teva) of $300. Importantly, this is the first time that HOKA accounted for greater than 50% of the portfolio – notable given that HOKA deserves 2x the multiple as compared to Ugg. The offset is that Ugg was down 2% for the quarter, which was 1,000bp better than our model, keeping in mind that 1Q accounts for only 10% of Ugg’s annual sales and it went up against a 70% comp in last year’s first quarter. For what it’s worth, we could literally zero-out Ugg growth in our model in perpetuity, and still get to a double in this stock over a TAIL duration – though we think that Ugg is good for msd growth for the remainder of this year. Mind you, this is a brand that the market has been waiting to die for the better part of 10-years, and yet the company continues to gain market share by entering new categories and classifications. The company took inventory early (up 83% vs ly – when it was very much under-inventoried in Ugg) for both Ugg and HOKA to avoid air-freight charges, and gain share at wholesale – but was convincing on the call in that it will remain tight with discounting throughout its FY as the market’s promotional cadence returns to more normalized levels – something we fully expect to happen in the back half of this calendar year headed into 2023. Bears are latching on to the inventory increase and the fact that the company increased the year by only a dime on a $0.45ps beat. But we’re still coming in at $19.50 for the year vs the guide (and the Street) of about $18. We build to $30ps in 3-years for a company that has a bullet-proof balance sheet, and has authorization to buy $1.5bn worth of its stock (it repo’d $100mm in the quarter at ~$260). In the 28 years I (McGough) have been analyzing stocks and having looked at over a thousand companies, I’d put the DECK management team in the top 1% (behind only Nike in the footwear space) as it relates to having a defined and proven process to stratify its product across consumer classifications (age, gender and use), channels, price-points and geographies. That’s why the traditional Ugg boot, which was once 90% of sales, is now only 10% and yet the brand has doubled in size. We think that the company will take the same playbook and apply it to HOKA, leaving far more growth in the model than a $333 stock suggests.

Guess? (GES) | Taking off Best Idea Long list. Kind of pains us to do this, but the fact is that we’re so bearish on apparel in 2H and 2023, so we’re increasingly of the view that GES will be unable to sustain/grow its Gross Margin. We like the 40% SKU reduction (provides big downside support in markdowns), and simply love the incentive management has to get this to a $35 stock to get a big payout (management at GES is arguably better than a company the size of GES probably deserves). Numbers this year look doable – but we’re mildly uncomfortable with the Street modeling $3.42 for next year. Aside from TJX, if you have to own an apparel name, we’d make this the one. But with names like DDS, JWN, RL, OXM and RVLV likely to trade down sharply in consecutive Quad 4s and discount their product accordingly, we increasingly lack the confidence in our model to make the 40-50% threshold that we (need/self impose) for a Best Idea long over a 12 month time frame. This one will remain on our Long Bias list, as we think valuation at 6x EBITDA for a business that has positive momentum and is being managed so well is too low. But we’ll look to re-engage here on a sell-off in apparel in 2H at a price perhaps closer to the mid-teens.

Chewy (CHWY) | Moving lower on Best Idea Long list. The stock has more than doubled from the bottom a few months ago. It’s now entering the lower end of the 12 month value range we outlined in the note after 1Q earnings $50 to $75 (CHWY | Strong 1Q In Tough Ecom Market). In early 2022 we were getting more bullish on ecommerce given we thought we’d see the space in aggregate go from slowing to accelerating around springtime. Now ecommerce names have rallied fast after AMZN delivered a 2Q acceleration and guided to another acceleration in 3Q. As macro continues to weaken we are becoming increasingly concerned about a weakening rate of change around 4Q, especially for players other than Amazon who looks to be getting more aggressive in driving share gains. This is staying on the BI long list, it could easily head to $70 on a good quarter and business acceleration, especially with still elevated 25% short interest. But the risk/reward after the rally suggests taking it down relative to other consumer longs.

Academy Sports and Outdoors (ASO) | Removing from the Long Bias list. ASO has been a winner long side in consumer. Stock is up 7% YTD with the S&P down 12% and the XRT down 21%. It still looks cheap at ~6.5x PE, but big box sporting goods names in Quad 4 should be cheap. There is definitely demand and margin risk coming for this space, and could be coming relatively soon. At these prices the stock is not pricing in all of the risk like it was in the 30s. We likely come back to this name at a later date with either a lower price, lower earnings expectations, and/better macro setup as we like the potential for unit growth.

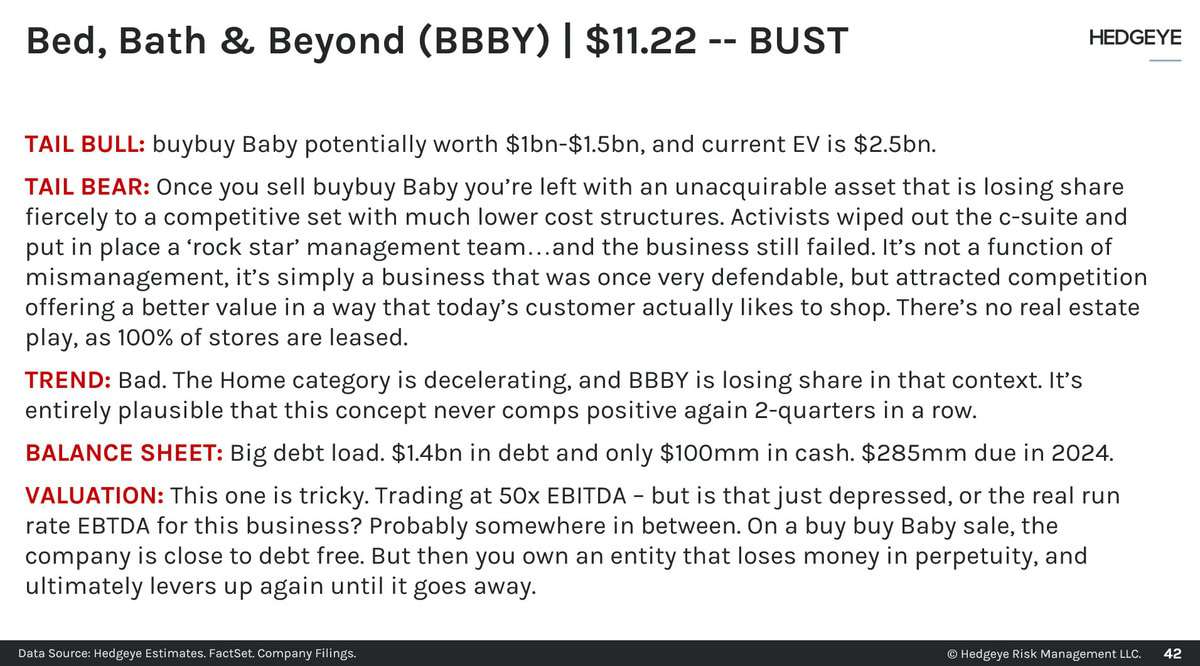

Bed, Bath & Beyond (BBBY) | Upping to Best Idea Short list. Ultimately a ZERO. This stock was up 173% over the past month. Was on our short Bias list, but now it’s a full blown Best Idea. We highlighted this name in our Bone, Bagger or Bust deck, and this is one name (or the 8 we flagged) that we think goes bust. The road to going bust is a volatile and sometimes painful one (short side), but on meme stock and market melt-ups like we’ve had over the past month, we think it’s a gift. Here’s what we said in our recent deck.

Weber (WEBR) | Moving Higher on Best Idea Short List. Will private equity take it out? Probably. But closer to the real earnings power at a reasonable (and potentially still lofty) hsd EBITDA multiple. The callouts on the category from Traeger (COOK) – a long term winner in the space, were downright depressing. WEBR is a fundamental ZERO, but practically one with 60-70% downside before it goes private – where it belongs.

StitchFix (SFIX) | Adding Back Short Side. This will go down as one of the best shorts we’ve had in recent years. Shorted at $76. Covered it too early near ~$10. Stock fell to $4.66 and then melted back up in this rally to $7.41. This company is unsavable. We think it’s headed to zero, without the take-out optionality it once had. Back up to $1bn cap. That’s about $1bn too high.

MarineMax (HZO) | Higher on Best Idea Short List. We think that the acquisition this past week of a luxury marina chain was a tell. Like, a bad one. Reminds us of CROX at $120 when it bought Hey Dude for $2.5bn, the core slowed, and management pulled a slight-of-hand to focus on a different initiative – and then the stock lost nearly half of its value. CROX is actually a name we’d own at a price – stay tuned there – but MarineMax caters to the ultra rich who will not fare well in multiple Quad 4s. This is the ultimate ‘negative wealth effect’ stock. Earning $8.50 this year, compared to $1.50 per share pre-pandemic. Successive Quad 4s won’t have people buying $3mm yachts, and which leaves less supply to fill the new marina acquisition – which cost 4.8x sales. This boating cycle collapsed FAST in 2009/10, and we expect the same this time around. 5x $3-4 in earnings gives us 50% downside from current levels.

Ralph Lauren (RL) | Moving Higher On Best Idea Short list. In the quarter last week, people got caught up in the headline beat vs the Street, but lost sight as to how lousy the quarter relative to last year, and on a trend-line basis. Let’s start with the positive – the company killed it in China. We were very impressed with that. The downshot – this is a company that grew sales by 8%, and saw a 8% lift in AUR (Average Unit Retail) – the very metric that we expect to implode in the fall (ie next month) and in 2023. If I could be locked in a room with only one statistic to show me a brand’s heat, it would be the e-comm growth. And it came in at a pitiful 2% in the US and 7% in Europe. The punchline is that the company is selling more product at high prices to existing customer and is OUTRIGHT FAILING to attract new customers to the brand. The real earnings power here is closer to $7 per share in the Quad 4 environment, while the Street has earnings marching up to $9 over a TAIL duration. That’s NOT going to be realized. We think that $7 TAIL earnings stream deserves a high single digit multiple. If you want to own something in this ‘class’, own PVH or GES – far better management, minimal key employee/succession risk, brands with much younger appeal, and meaningful upside to margins (espec PVH) over a TAIL duration. Don’t buy into the RL hype you see today. It can change VERY quickly.

Canadian Tire (CTC.A-TSE) | Moving from Short Bias to Best Idea Short list. The earnings crack that we saw last week – that the market looked right through – was largely from the company’s credit operations, which is about 25% of EBIT. But simultaneously we got negative date points about jobs and housing values in key cities in Canada. Canadian Tire is the ‘go to’ store for people to get work done on their cars, and while they wait, they shop for toasters, hockey sticks, and mid-market apparel (think Kohl’s). THAT’s the segment we’re concerned about today. The productivity rate exploded over the pandemic to over $405/ft from $320 in 2018/19 – with massive risk for mean reversion in spending. Probably worth noting that the company has about $1.75bn in petroleum revenue that’s been deflating over the past month. Nonetheless, we come out with TAIL earnings power of ~$15, with the street (all Canadian analysts jockeying for the next banking deal) who have nose bleed estimates pushing $25. The stock looks cheap at 7x EBITDA, but no reason why department stores (even Canadian ones) can’t trade at 3-5x EBITDA in a downward revision cycle. Short interest stands at only 2%. Think you have 40% downside in this name over a TAIL duration, with near term trends eroding on the margin.

Urban Outfitters (URBN) | Gaining Confidence in Short Ahead of Earnings, taking higher on short list. We have no beef with URBN’s concepts – Urban Outfitters and Anthropologie are well run, not overstored, and are more productive than most of their peers. The problem is that its inventories are way too high – particularly in the core Urban concept, and with inventories building in the channel we think that there’s gross margin pressure brewing in 2H. And then there’s Anthropologie (roughly 40% of cash flow), which put up a solid 1Q, and the Street seems to be assuming that this strength carries through to the back half of the year. That’s too optimistic given the promotional activity that we expect to be pervasive in 2H. Ultimately, we’re getting to about $1.80-$1.90 for the year with the Street at $2.25. Is that huge downside? No. But if our model is right, there’s no reason why this can’t be a low to mid-teens stock vs its current $22. URBN is the kind of business we’d like to own at a price – defendable concepts, solid management…but we’d only like to buy it when both the Urban and Anthro concepts are down and out. We think we’ll get that chance with 3-6 months.

Dick’s Sporting Goods (DKS) |Moving Higher on Short Bias list. Much like the position change for Academy, DKS in our view isn’t pricing in the earnings reversion risk with the stock up above $107 and trading back around 10x PE. The call in this space seems to be cheap stocks, with share repo, stronger LT demand, and lower competition. We don’t really disagree much with that take, except that cheap is likely to get cheaper at least until EPS is revised much lower and the stocks grind lower as well. The consumer is getting weaker and we think DKS will have to back away from its margins higher forever commentary. Stock is probably worth $80 to $90 but could see lower on bad Quad4 market days.

Best Buy (BBY) | Moving Higher on Best Idea Short list. We moved this lower on the short side a couple months back with the stock around $70 and the market becoming aware of the appliance/durables inventory problem from TGT’s signal. However now BBY is back up, and we think industry trends have gotten worse. BBY is trading at 12x earnings again after it guide down but we think there is further earnings risk to come. The company guided margins to just a little below 2019 level while we are heading into a US recession. Margins could easily be revised down another 75 to 100bps, and the stock will start to look very expensive in the $80s. Demand is slowing and inventories are high. Then the street is of course modeling sales and margin expansion in 2023, yet we could see a multi-year time period of reduced consumption in many of BBY’s core categories. We see earnings downside risk to ~$5.50 and a stock closer to $55 to $60.

ETSY (ETSY) |Taking Higher on Short Bias list. ETSY has seen a rally in recent weeks after reporting earnings. It beat on headline rev/adj EBTIDA results but there were lots of holes in this business while carrying a bigger multiple than peers with better growth prospects in the coming quarters. Sellers in decline, buyers in decline, GMS down 7% and slowing. Top line growth came was from seller fee increase and inorganic acquisition contribution yet 1H EBIT was down 35%, while Adjusted EBITDA was about flat, and up in 2Q, aided by a massive ramp in stock based comp being added back. Customer churn remains a risk, with 12mm customers churning off this Q, higher than we expected and new adds/reactivations also slightly higher. Amazon is getting more aggressive in driving share and is reportedly going to do a second “Prime Day” type event in 4Q on top of Cyber5. Growth will continue to be hard to come by for ETSY which actually has relatively tough compares when matched up against the rest of ecommerce. On disappointing top line trends in 2H we think the multiple compresses and stock revisits the $75 range.