“If history is any guide, this scenario will develop not gradually but abruptly.”

-Barry Eichengreen, (“Exorbitant Privilege” page 165)

Evidently a lot of investors didn’t prepare their portfolios for The Inflation. Some reconciled this mother of all inflation shocks in food prices as “supply and demand” imbalances. Some said everything was going to be fine because The Ber-nank said so. Some even said $4-5 at the pump is fine.

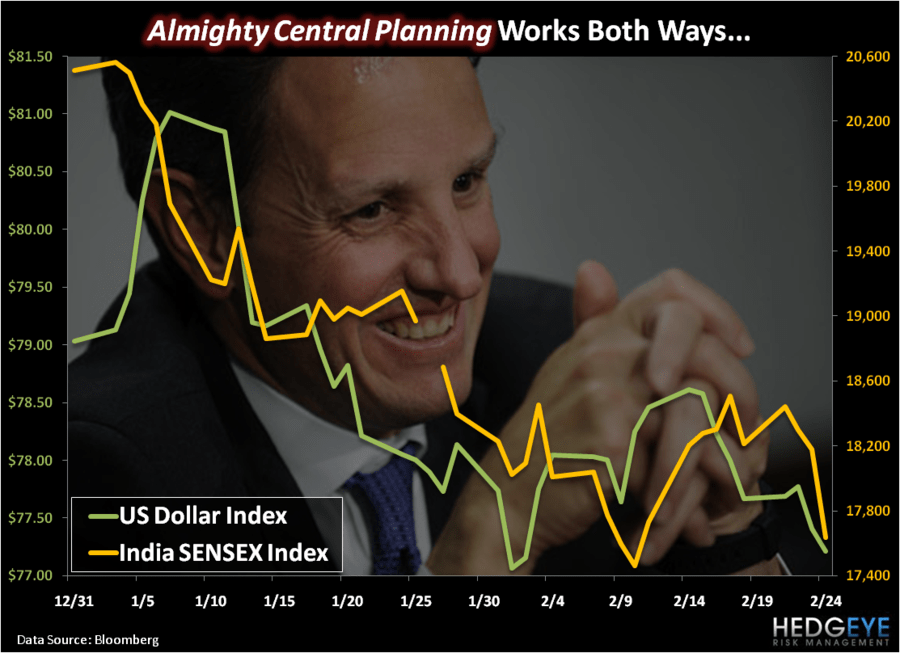

We’ve said that as Global inflation Accelerates, Global Growth Decelerates. This might be a little easier to see when you have a $100 handle on the price of oil per barrel. Inflation is both a policy and a consumption tax. Global inflation is also priced in US Dollars.

Sadly, with stock markets around the world getting rocked this week, the US Dollar continues to be debauched. There was a time when America’s independent price stabilizer (Paul Volcker) treated the US Dollar with respect. Today, our Almighty Central Planners are willing to watch the Buck Burn.

The math doesn’t lie here folks; professional US politicians do. For the week-to-date, here’s your US Dollar/Commodity Inflation score:

- US Dollar Index DOWN -0.33% for the week-to-date (down for 7 out of the last 9 weeks)

- CRB Commodities Index UP +1.7% to 347 (making a series of fresh weekly closing highs all the while)

Sure, there’s a nut-job out there in Libya, but there’s also a very blunt instrument that can take his grandstanding on “fighting to the last drop of blood” away – a STRONG US DOLLAR policy.

Most American stock market fans definitely don’t want the short-term tough love associated with that. If anything, the perma-bulls are already cheering The Ber-nank on to implement Quantitative Guessing III (QG3) as a weapon against Gaddafi’s self-destruction.

The reality is that if The Ber-nank and Timmy Geithner woke up this morning and unilaterally raised interest rates and took a whack out of this Disaster Deficit, the US Dollar would strengthen and the price of oil would drop in a straight line.

This, of course, isn’t going to happen. Instead we are fostering a finger pointing and unaccountable political leadership class that continues to frustrate Americans to the core.

While Timmy Geithner was self-aggrandizing himself yesterday with his banking cronies from Dollar Destruction Inc., someone asked him what he thought about the price of oil’s impact on the US economy – and I couldn’t make this up if I tried, but he said that the economy that he helped put into crisis (before he helped saved us all from it) “can handle it.”

The Twitter-sphere lit up like a Christmas tree after Timmy said that – and The Rest of The World erupted in laughter. He must have been joking, but Bloomberg reporter Rich Miller didn’t seem to think so - and I couldn’t make this one up if I tried either – as Miller recapped the Geithner Groupthink session yesterday with this morning’s Bloomberg headline:

“GEITHNER BUTT OF JOKES NO MORE AS OBAMA’S MONEY MAN NOW ON TOP”

On top of what? The Disaster Deficit, The Burning Buck, or the resume pile to go join the Pandit Bandit at Citigroup? The manic media pandering to the political winds of Washington, DC access is both frightening and sad. Arianna Huffington, nice sale!

Don’t worry, I can answer the Wall Street question on, “how do you make money on this”? I laid this out in Friday morning’s Early Look note titled “Hawkish Winds” and my Global Macro positioning in being bullish on The Inflation remains the same:

- LONG - Dollar denominated food and energy Inflation

- LONG - Currencies of countries with hawkish central banks

- LONG - Financials in socialized countries that have made banks too big to fail

- SHORT - Sovereign Bonds of countries with deficit and currency devaluation central planners

- SHORT - Currencies of countries with dovish central banks

- SHORT - Emerging Markets

As for managing around the implied mean-reversion risks associated with the institutional investment community in America chasing the “flows” rather than the Global Macro fundamentals, my strategy on US Equities is this – trade them like the Price Volatility Casino that your central bankers sponsor.

After all, as Timmy reminded his fans at the “Bloomberg Breakfast” in Washington, DC yesterday, “central bankers have a lot of experience in managing these things”!

Indeed they do Mr. “Money Man”, indeed.

My immediate term support and resistance levels for the SP500 are 1306 and 1330, respectively. If 1306 in the SP500 doesn’t hold on a closing basis, I think this -3% correction in US stocks starts to resemble a February 2008 like crack. That wasn’t a good crack.

Best of luck out there,

KM

Keith R. McCullough

Chief Executive Officer