The third largest denim fabric manufacturer (and major textile conglomerate) Arvind Mills reported a couple of weeks ago. Below we include some relevant data points comparing the company’s textile results over the past two quarters as well as comments from the company’s chairman on the pricing environment. Arvind’s large customers include Wal-Mart and Gap Inc to name a few.

Q&A with Sanjay Lalbhai, Chairman and Managing Director of Arvind via CNBC-TV18:

When we spoke to a couple of textile players last, they indicated that because of the surge in cotton prices there is a shift that many of the makers are doing to polyester and they are increasing the production units there, are you doing anything of that sort and is the gap increasing between cotton and polyester?

The gap is increasing, we have a large range of polyester denims which is growing rapidly but there is a large portion of our business which is cotton and it's very difficult to move it into polyester because this is high-end cotton. We do believe that even with high prices in cotton, these prices have been absorbed and expected in the US and European markets and also the Indian market. And we believe these prices are sustainable now that the consumers have also accepted them and now all the buyers have also accepted them. So unless the prices further go up dramatically there should not be any reason for worry.

How is FY12 shaping up, now that you have turned around your operations effectively in FY11 – FY12 both in terms of topline and also your EBITDA level performance given that cotton prices are so high, do you think 14% kind of margins are sustainable?

We believe so, but you are right that cotton has touched all time highs. This kind of cotton prices have never been seen before and we have been able to pass on this costs until now but if the cotton situation gets worse then I think there could be issues whether there would be erosion in demand. Q3 Textiles (ending 12/31)

Q3 comments: Cotton prices have more than doubled in last one year and the prices have shot up very sharply in last 3-4 months. The company has increased selling price of its products to offset the cost push, any significant increase in cotton price could affect the margin if company is not able to pass on the cost increases.

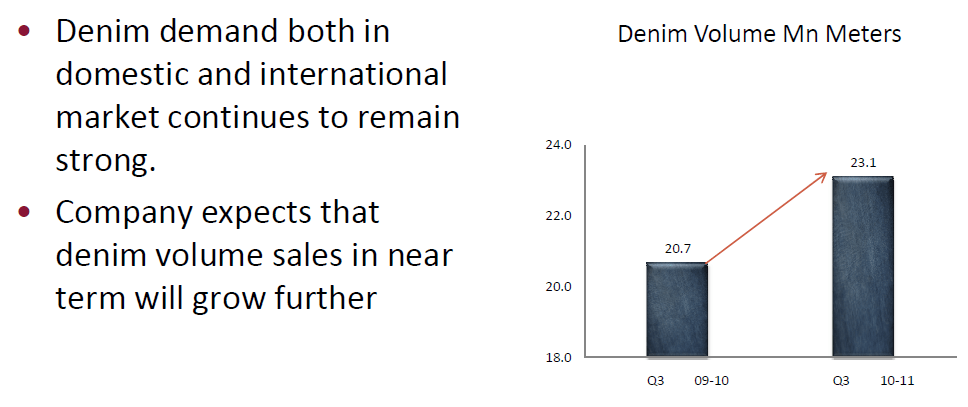

Q3 Textile Summary (ending 12/31)

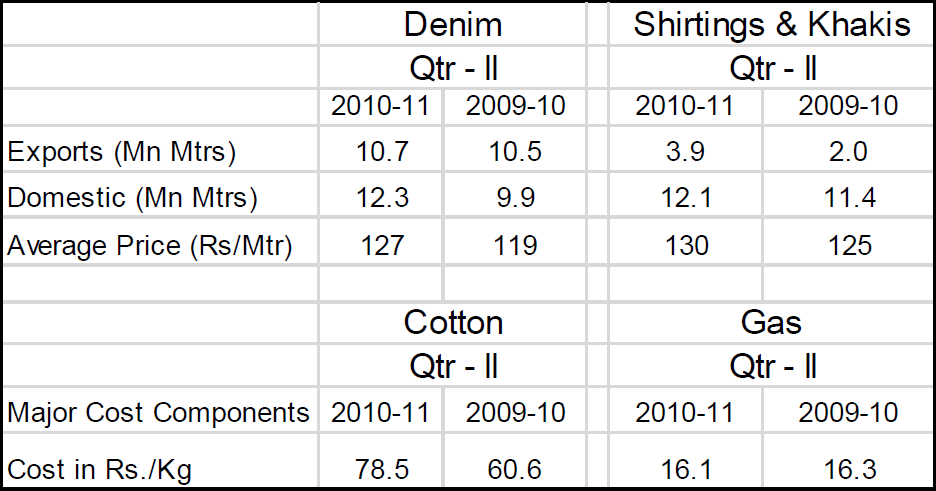

Q2 Textile Summary (ending 9/30)

Despite rising costs, potential for trading down, and increasing use of substitute materials-

Eric Levine

Director