This commentary was written by Dr. Daniel Thornton of D.L. Thornton Economics. Thornton spent over three decades at the St. Louis Fed as vice president and economic advisor.

With inflation on the rise, many economists are calling on the Fed to increase its federal funds target rate more aggressively. They believe that other interest rates are somehow mechanically tied to it.

I believed that what the Fed does with its federal funds rate target would be totally irrelevant were it not for the fact that market participants, like the citizens of OZ, believe in an all-powerful Fed.

Increasing the federal funds rate target will be of little use, because interest rates will increase whether the Fed does that or not. Moreover, the Fed has always followed the market.

For recent evidence of this, see On the Fed’s (In)Ability to Affect Interest Rates.

Others, including myself, believe the Fed needs to drastically reduce its balance sheet which it created in the wake of the 2007-2009 financial crisis and recession, and the pandemic. I want this in large part because the Fed should not be financing government and private debt. This is the job of financial markets. The Fed has no business doing it.

I also want the Fed to drastically reduce its balance sheet because it might reduce the money supply. I doubt that it will make much difference for inflation. The remainder of this essay explains the thought process that led me to this conclusion.

The Link between Money and Spending

The monetary theory of inflation is based on the belief that there is a direct causal link between money and inflation. The idea was that in order to purchase anything, you need money (cash and/or checking account balances).

Hence, if the Fed increases the money supply people would be holding more money than they wanted to, so they would spend it. Since production cannot be ramped up quickly, prices would increase. If the money supply is increased at a faster rate than people are demanding it at current prices, prices would rise persistently, i.e., inflation would result.

Hence, inflation could be controlled by reducing the growth rate of the money supply to a rate that matches the public’s demand for money at the current price level. This gave rise to Milton Friedman’s famous money growth rate rule. By matching the growth rate of the money supply to the growth rate of society’s demand for it, the Fed—indeed, any central bank—could stabilize the price level.

A problem for this theory arises when there are a myriad of other ways that purchases can be made; even if a person has little or no money.

In this environment, a person only needs to have income producing assets, or the expectation that such assets will produce income in the future to make purchases.

Economists realized this problem a long time ago. The problem was recognized in what was called the income velocity of money, i.e., the ratio of nominal output (nominal GDP) to the supply of money. Specifically, economists recognized that the money theory of inflation required the velocity of money to be relatively stable.

If the velocity of money were to decline, people would be holding less money relative to their income, which could cause prices to rise unless the Fed reduced the supply of money accordingly. [For a complete analysis of the role of velocity, see the paper I published in 1983, Why Does Velocity Matter?]

In the early 1980s, the velocity of money began behaving erratically and unpredictably, and has ever since. In 1987 I published a paper with Courtenay Stone which investigated several theories of velocity aberrant behavior (Solving the 1980s’ Velocity Puzzle), but to no avail.

As a consequence of the aberrant behavior of velocity, economists began combining an increasing variety of financial assets into alternative measures of “money.” These data mining exercises produced a number of “monetary aggregates,” but none had a significant relationship with inflation. The Fed eventually stopped publishing data on these monetary aggregates except for M1 and M2.

The failure of this effort coincided with Greenspan’s adoption of the federal funds rate as the Fed’s policy instrument, see Greenspan’s Conundrum and The Fed’s Effect on Long-Term Yields.

On page 20 of this paper is a quote from Chairman Greenspan explaining the reason for this change. Monetary policy became about interest rates, money was only mentioned by economists who continued to believe there was a strong link between money and inflation, even if they were not able to find a strong relationship between any measure of “money” and inflation.

I have always favored the M1 measure (cash + checkable deposits) because that is the only measure the Fed could directly control, see Targeting M2: The Issue of Monetary Control. I believe that it is useless to target something that you cannot control.

However, on March 26, 2020, the Board of Governors reduced the reserve requirement on checkable deposits to zero. This action ended the Fed’s ability to control M1. In February 2021 the Board redefined M1 so that M1 and M2 are very nearly identical. Consequently, it makes little sense to distinguish between them.

In any event, the checkable deposit portion of M2 cannot be controlled now because there are no longer reserve requirements on these deposits. Here is the reason the Fed cannot control these deposits. [The reader who understands this process can skip to the next paragraph.]

If the reserve requirement (RR) was 10%, and reserves were say $25 billion, the most checkable deposits the banking system could create would be $250 billion. However, if the RR was 5%, the banking system could create $500 billion. If the RR was just 0.005%, the banking system could create $5 trillion. With the RR at zero, there is no limit to the amount of checkable deposits the banking system can create.

This process works in reverse. With reserve requirements, checkable deposits decline by a multiple of the quantity of reserves the Fed drains from the banking system. When RR is zero, draining reserves will not necessarily reduce the quantity of checkable deposits.

This means that even if the Fed were to drastically reduce its balance sheet, the checkable part of M2 may not contract as much as it would if reserve requirements had remained in force.

M2 will contract even less since the reserve requirements on the non-M1 components of M2 were reduced to zero in January 1990. It is much less likely that the Fed would re-impose reserve requirements on them than on checkable deposits.

Even with reserve requirements at zero, contracting the balance sheet aggressively will initially reduce the amount of bank reserves, i.e., deposits with Federal Reserve Banks, and checkable deposits by the amount of the securities sold.

The effect on banks’ reserves will be permanent, but given the lack of reserve requirements there is no guarantee that the effect on checkable deposits will be. Nevertheless, the sale of securities will permanently reduce the amount of credit the Fed is supplying to the market by the amount of the sales.

This is a good thing because financial markets should be financing government and private spending, not the Fed.

Can the Fed Stop Inflation?

Now back to the question of whether the Fed can control inflation. The answer depends on what is causing the inflation. I will address this question, starting with the supply chain problems.

If supply chain issues were the sole cause of inflation two things would be true. First, the inflation would be temporary and end once these problems ceased.

Prices might return to their pre-pandemic levels, but I wouldn’t bet on that. However, the price level would likely decline from its post-pandemic peak. Second, there is nothing the Fed can do to control it.

In a letter to the Wall Street Journal, WSJ Dec. 20, 2021, I suggested the Cares Act was the main inflation culprit because it gave trillions to people who didn’t need it—those with twice the median income.

The Cares Act was essentially a helicopter money drop, which nearly everyone agrees is inflationary. While I didn’t say this in the letter, the Fed’s massive bond buying program also put trillions directly in the hands of the public. The Cares Act just did it more directly and more quickly. However, inflation is a dynamic process.

To be an inflationary process, it must be systemic; it needs to be caused by factors that affect a wide variety of prices.

Moreover, it must be persistent. The Cares Act alone would have produced a one-off increase in prices. If this was the only thing that happened, it wouldn’t necessarily cause inflation.

It wasn’t the only thing that was occurring. Wages are a factor that could produce a persistent increase in a large number of prices. After trending up from 1950 to the late 1970s, wages and salaries trended down until 2021.

Even though inflation was relatively low, real wages have declined even more during this period. The 2007-2009 financial crisis and recession was accompanied by a historically large decline in the labor force participation rate, much of which is yet unexplained. The pandemic has been accompanied by an inability of many firms to hire workers even though wages and salaries have increased significantly in 2021.

These facts suggest the possibility that the pandemic and the loss of over 1 million lives and the prospect that the pandemic is not yet over, may have caused many people to reevaluate their work/leisure tradeoff in favor of working less.

That workers are seeking higher wages is witnessed by the recent trend toward unionization. Wages will have to increase a lot to offset the wage losses since 1970s. Wages will have to increase even more to offset the effects of inflation on real wages. Hence, wage growth may be one of the dynamic factors that cause inflation to persist for some time.

Combine this with the likelihood of even larger government deficits, and the strong possibility that the supply chain problems will continue for some time because of a senseless war, excessive Covid lockdowns in China and China’s transition from market-based production to government-controlled production, inflation could be with us for a long time.

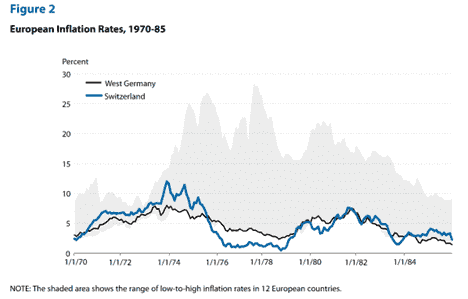

Can monetary policy help? Let’s see what historical experience suggests. As is the case now, the Great Inflation was global.

This is shown in the figure below which shows the range of the inflation rates for 12 European countries (not including Switzerland) with West Germany and Switzerland emphasized. [The figure was from a Cambridge conference volume, and was reprinted in the Federal Reserve Bank of St. Louis Review, here]

The figure shows that while all of the countries experienced inflation during the period, West Germany and Switzerland fared much better.

West Germany and Switzerland did so by constraining the growth of the monetary aggregates. This suggests the possibility that the Fed could significantly reduce inflation by restricting the growth of the monetary aggregates in the same way.

Could this approach work for the Fed? Perhaps, but I doubt it for several reasons. In economics, the past is not necessarily a guide to the future. As I noted above, the connection between money and spending has changed dramatically since the early 1980s. Hence, there is no reason that a policy of constraining the growth of the monetary aggregates will work now.

Then there is the fact that unlike West Germany and Switzerland in the 70s and early 80s, the Fed is focused on trying to affect interest rates. The Fed hasn’t shown any interest in controlling the growth of the monetary aggregates.

It is unlikely to do so now. If it was concerned about the growth of the M1 and M2, it would shrink its balance sheet at a faster rate than it increased it since March 2020. It is not!

So what do I conclude from all of this? First, I believe that inflation is no longer “always and everywhere a monetary phenomenon,” at least in the sense that Milton Friedman once asserted it was.

Inflation is likely due to a confluence of a variety of factors, only one of which is the money supply. This is why the massive increase in M1 and M2 from 2009 to late 2020 did not cause inflation to increase above the Fed’s 2% inflation target. Nevertheless, I believe that a monetary policy that controls the growth rate of M2 is the Fed’s best hope of reducing inflation.

This would require the Fed to re-impose reserve requirements on all of the components of M2 and conduct policy based on significantly reducing it and thereafter controlling its growth rate. But even this would not prevent periods of inflation from occurring. Nevertheless, this is the Fed’s best, indeed the only chance, that monetary policy can reduce inflation.

I believe the best thing the Fed can do now is to aggressively reduce its balance sheet and, hence, reduce the amount of credit it is currently supplying to the market.

If this were to result in a marked reduction in M2, it would be a good thing in that there would be fewer highly liquid assets that could help fuel inflation. As I point out above, in the absence of reserve requirements it is unlikely that this will produce a large enough reduction in liquid assets, but it could help. I don’t see the Fed restoring reserve requirements or trying to control M2.

Like most people and all government agencies, the Fed won’t make drastic changes until its back is against the wall. This is why I believe that it is unlikely the Fed can do much to quell inflation.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.