“Big boys don’t cry unless their last name is Boehner, or they’re a banker in need of a bailout.”

-William H. Gross

Bill Gross is one of the buy-side’s best writers. And in his Investment Outlook note from PIMCO yesterday, that was one of his best one liners. There’s nothing quite like having the Big Boy discussion out there about what’s actually happening in the marketplace.

What’s happening out there is that The Ber-nank and the bullish Bond Boys are all of a sudden getting smoked out of their holes by inflation. And the manager of the world’s biggest bond fund isn’t happy about it.

Before I recap some of Gross’ snarly attacks on The Ber-nank (he one-upped me!), let’s preface this Big Boy argument not with what should be happening to bond yields (Bernanke’s QG2 promise is that they’d remain low), but what is happening to bond yields:

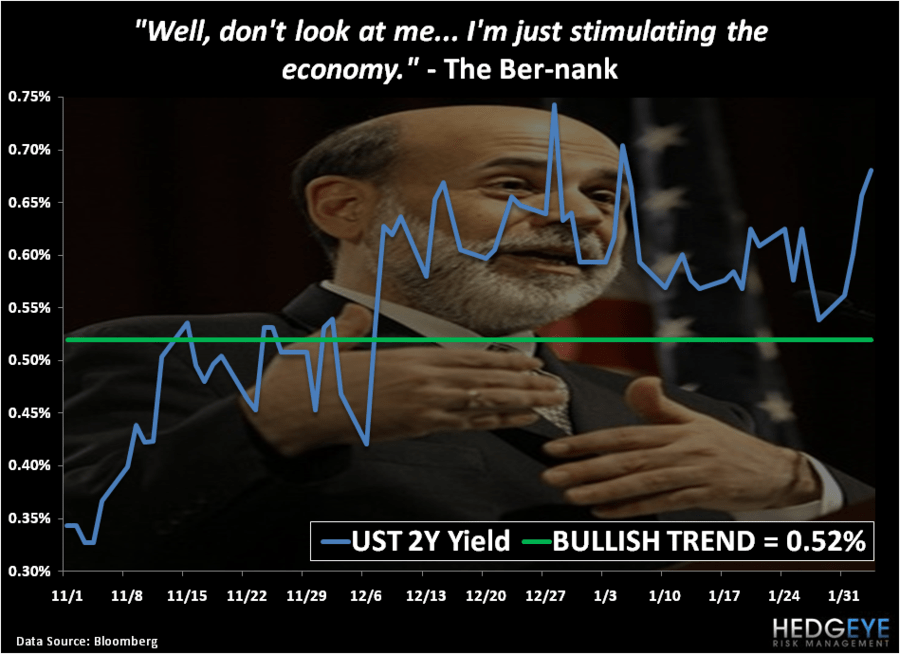

- 2-year US Treasury yields - continue to make higher-highs and higher lows since Bernanke made his Quantitative Guessing 2 promises. This morning 2’s are busting a move towards 0.67%, which is a +24% move for the week-to-date and +103% move since the 1st wk of November

- 10-year US Treasury yields - broke the sound barrier of their December highs yesterday and at 3.52% are +38% higher since the 1st wk of November.

- 30-year US Treasury yields – continue to make higher 9-month highs, pushing towards 4.64% yesterday which is up +17% since the 1st week of November, and up +31% since the 1st week of September.

So what gives here? Isn’t Big Government Intervention the elixir of American life?

Obviously a few things seem to be going the wrong way on Bernanke here - as they should when Global Inflation Accelerates. After all, there is always another side to any government supported trade. Debauching the US Dollar = inflation. And inflation kills bonds.

Now for a more sophisticated Big Boy dress-down on the matter, let’s turn back to what Bill Gross has to say about this:

- “A low or negative real interest rate for an “extended period of time” is the most devilish of all policy tools.”

- “This is the framework that has been created by modern-day policymakers who have innovated far beyond their biblical counterparts.”

- “Today’s rock bottom yields, however, have less to do with disinflation and more to do with providing fuel for an asset based economy that promotes unsustainable wealth creation and false confidence in perpetual capital gains.”

Well done Mr. Gross. Well done.

You see, the Thunder Bay Bear isn’t balled up in his ice fishing gear clawing at Bernanke’s beard all on his very own here. From Jim Grant in New York to Bill Gross in California, this is turning into a whale hunting expedition - with the hunted being the Chairman of the Fiat Fools.

Yes, I am pushing my own book here because I am long inflation (short bonds) and Gross is trying his best to protect his book (all bonds), but no matter where Bernanke may want this little inconvenient critter called real-time market prices to go, there it is…

Now, to be fair to the perma-stock market bulls who claim that they don’t see any inflation anywhere (despite being long commodity and energy stocks), there are 2 cornerstones to the argument that rising inflation and rising borrowing costs won’t hurt US stocks or corporate margins (even though borrowing costs are at all time lows and operating margins are at all time highs):

- This move higher in US interest rates is all about US growth accelerating

- And if US Growth doesn’t accelerate from here, we’ll blame the snow and/or dial up The Ber-nank for some QG3

There is also the infamous “flows” argument, but US stock market history fans should be reminded of what happens to legendary long only guys like Bill Miller when “the flows” stop…

Interestingly (and not ironically in terms of market timing), according to a Bloomberg headline this morning “Bill Miller Is Back On Top”…

Can someone get me a quote on what a dollar invested with ole Bill at the last US stock market top (2007) looks like today (give the poor guy some marking-to-model and don’t adjust that dollar for its debauchery).

I guess another angle you could take on why the Bond Boys are bitter is the upcoming calendar of events in US Congress:

- Midterm Message - the newly minted chairman of the US Financial Services Sub-Committee on Domestic Monetary Policy (Ron Paul) will be hosting his first dance with Ben Bernanke in Washington, DC next week (February the 9th)

- US Budget Deficit - at some point in the coming week, President Obama needs to unveil the alchemist draft of the US Federal Budget (don’t forget that the CBO just raised the Budget Deficit forecast by 46% for the next 3 years, so Barry has some pencil pushing to do).

- US Debt Ceiling – that needs to be addressed over the course of the coming month because, in theory, America needs to make a decision on this before March 4th, or our creditors might get a little peeved.

Or are they already right p.o.’d? If you were The Creditor of this nation (China) and watched Geithner mimic Larry Summers’ hand signals on C-SPAN as he threatens the white wall of Congressional stares with “the alternative”, wouldn’t you be?

This morning, Timmy’s assistant at the Treasury for financial markets, Mary Miller, said this about raising America’s $14.3 TRILLION debt ceiling: “We expect that Congress will do the right thing.”

With all due disrespect for what these government people have considered “the right thing” for the last 10 years, I’ll stay with the right risk management call that we’ve been making here in Q1 called “Trashing Treasuries.” (email if you’d like the 50 slide Q1 Macro Theme deck). Big Boys don’t cry wolf.

My immediate term support and resistance lines for the SP500 are now 1292 and 1311, respectively. We remain bullish on inflation and bearish on bonds. Our latest call to short Treasuries on the short end of the curve was made at 320PM EST on January 27th, 2010.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer