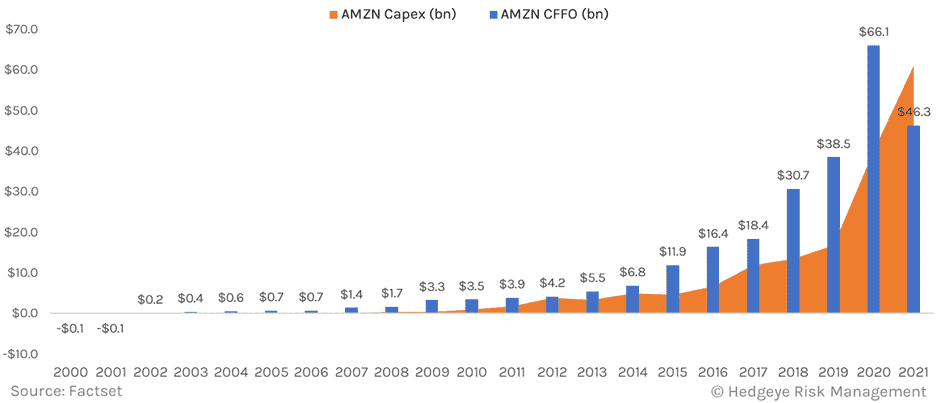

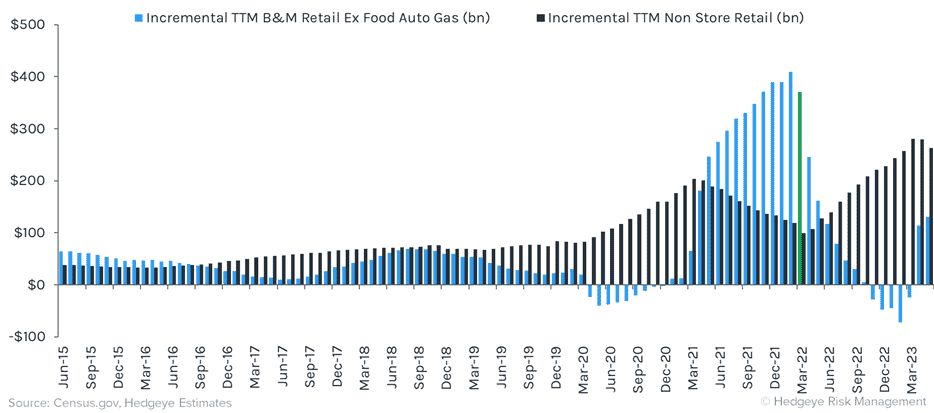

Best Idea Long AMZN reports 1Q earnigns on Thursday after the close. This is another quarter where AMZN stock is making lows ahead of the print. Macro Quad4 continues to rear its head on consumer growth names, as our net view on ecommerce remains short, though within the space we like Long AMZN and CHWY vs short ETSY and W. We are within about a month of what should be an inflection in the ecommerce space from slowing trends to accelerations in growth. Last Q proved to be better than feared in terms of the market reaction. We're not overly bullish on 1Q vs expectations, but think the company is likely to come out ahead on 2Q guidance. In 1Q we are slightly below the street on both revenue and EBIT, though with both still inside the company's guided ranges, if there is a line we think could beat it's gross margin. For the first quarter we have seen nonstore retail growth in the US slow about 300bps and since the guidance in February we have a war in Ukraine with AMZN suspending shipments in Russia and Belarus as a result. So it would not surprise us to see another revenue slowdown and pressure vs consensus in the 1Q result. As we look to 2Q however, we think we are likely to see solid guidance and an inflection to acceleration. The street looks too low on 2Q revenue, that should also mean some EBIT upside in the guide, but we can always expect AMZN to be aggressive on SG&A investment rate, though it did acknowledge moderating investments in fulfillment, suggesting some potential leverage on that line. Ultimately we think we have a model where both revenue and gross profit growth are going from slowing down to the single digits to accelerating back up to around 30% growth by 2H. That should drive the AMZN multiple higher. The precise real time point for an inflection would be around Mid-may as the company hits easier compares and leverages the significant investments it has made into share gains and outsized growth in the online space. 2021 was the first year Amazon invested more in Capex than it generated in CFFO. Historically, AMZN has done an outstanding job turning capital deployment in to incremental cash flow.

The immediate market term signal is still negative on AMZN and we are still in Quad4, the only Macro Quad historically where you don’t want to own AMZN. With that said, the intermediate term Trend fundamental model setup is about as bullish as it has been since the early days of the pandemic. We think there is 50%+ upside for this mega cap name over 12 months.

Here is our note from last AMZN earnings: AMZN | Just Guided The Trough, Best Idea Long

If interested in our guest speaker call with Hedgeye's legal/policy analyst Paul Glenchur and 3p Ecommerce Lawyer Paul Rafelson on AMZN regulatory risk here is the Video Replay Link: CLICK HERE