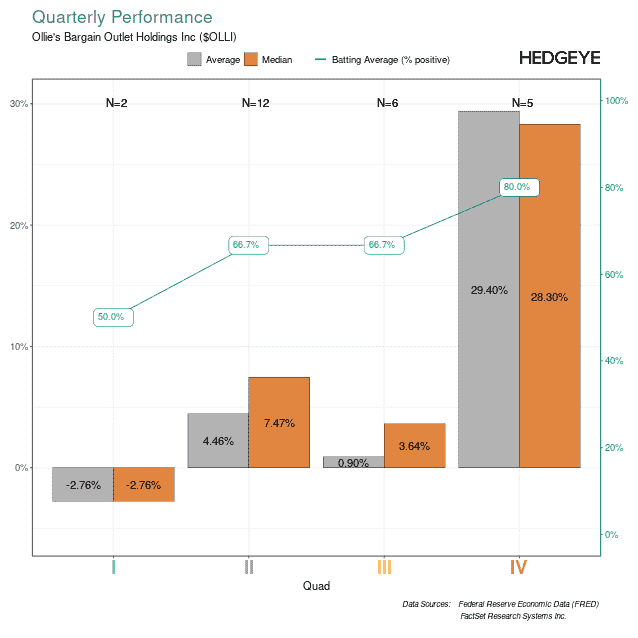

Adding OLLI to our Best Ideas Long list. This is a beaten up retail name that is likely to see a bullish inflection in the P&L next quarter. Rate of change in revenue and profits is likely to accelerate imminently. Contrary to most of retail, OLLI actually had a rough 2021 after standout performance in the early days of the pandemic. We were correctly short it from August 2020 to August 2021 expecting a material revenue slowdown and margin pressure, which we got. Now it's facing easing compares while the underlying business trends are likely to improve. We expect a consumer slowdown near term, and that might sound like a bad thing, but for OLLI it means consumers become more cost conscious and go bargain hunting (at Ollie's) at the same time the other retailers will see inventory building creating good closeout buying opportunities for OLLI. Tack on a long term store growth story with stores planned to grow low double digits for the next couple years. The punchline is a model that is churning out 45%+ earnings growth by 2H while much of the rest of retail will continue to see EPS pressure. With unit growth, low SD comps and gross margin reversion, the out years' EPS growth CAGR remains around 20%. OLLI is coming off trough valuation multiples. With the company returning to growth it should go back to reasonable historical multiple levels of 25x to 35x PE. For NTM earnings as of 2Q22 we're getting to $2.80, Tail earnings power of $3.50 to $4.00, and we think a rare unit growth story with this earning growth profile deserves a 25x to 30x PE. That gets to a fair value of the stock around $70 to $80 or 35% to 60% upside from here. We think this is a name you can own right now. It's historically a good Macro Quad4 performer, and it syncs with our CEO Keith McCullough's quantitative signal as a long on both Trade and Trend durations.