In the absence of hard data in between the longest reporting period drought of the year, speculation on Foot Locker’s sales trends reached a fever pitch at mid-day today. In part due to the release of the NPD weekly athletic footwear data and in part due to a large bulge bracket firm making a call that sales have slowed materially in the second to last week of the company’s fiscal fourth quarter. Speculating on one week alone can be dangerous and as such we don’t normally spend too much time supporting or refuting “channel checks” or weekly scan data. However, the facts in this situation are worth exploring in greater detail.

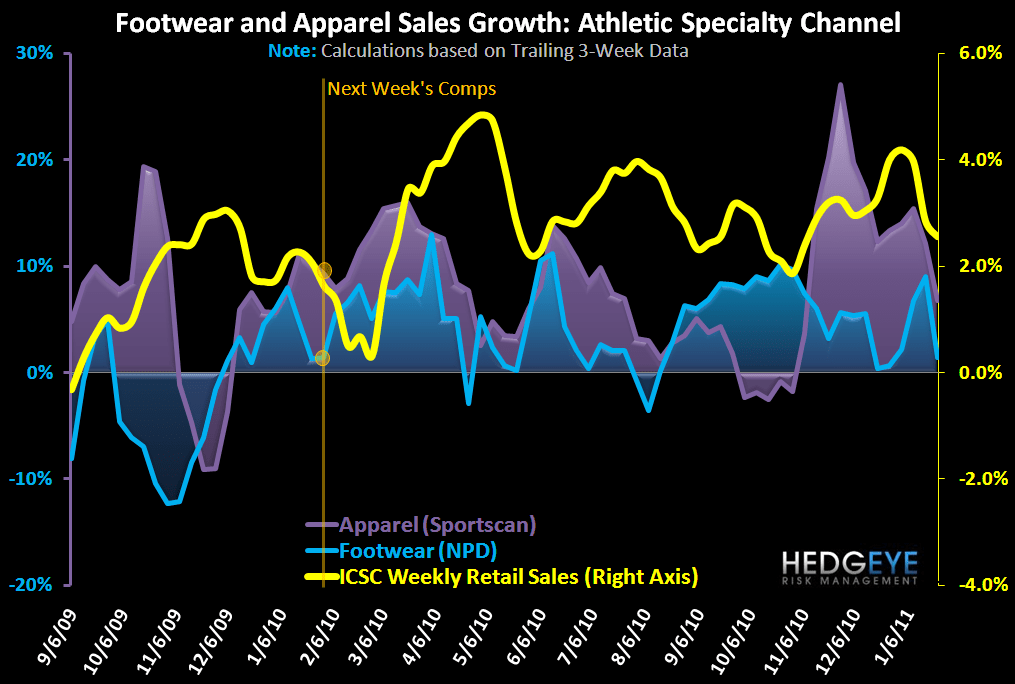

Fact 1: Weekly athletic footwear sales for the athletic specialty/sporting goods channel were down 9.4% for the week as per NPD data. This clearly marks a meaningful deceleration over the past two weeks.

Fact 2: Foot Locker reported same store sales have been tracking in a range of 100-200 bps HIGHER than our blended NPD/Sportscan Index.

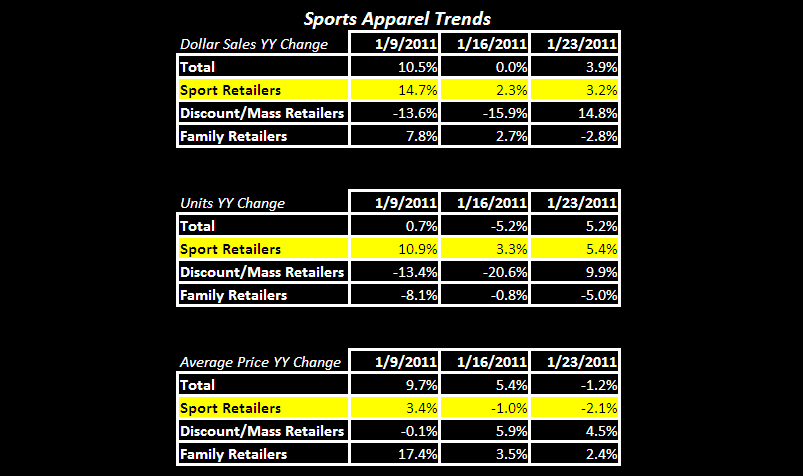

Fact 3: Apparel accelerated this past week to up 3.2% y/y from +2.3% in the prior week. Nothing heroic here but not nearly as challenging as footwear.

The Math:

If we assume that Foot Locker outperformed the industry for the week in question, as it has recently, then we put the week’s performance at down 7%. Next, we must estimate what “weighting” the week in question represents as a percentage of the total quarter. Clearly January is the smallest volume month of the fiscal quarter, suggesting that an equal weighting of week 51 at 8.33% would be overstating the importance of the said week. So in making realistic assumptions (in this exercise for which we may never know precisely what one weeks of sales momentum really did), we assume that the week is worth 4-5% to the quarter. All in, this results in a hit to overall quarterly comps of 28-35 bps on our modeling assumption that same store sales will end the quarter up 6%.

Importantly, the same weekly trend underpinning this analysis is being used by a competitor to adjust estimates down by 100 bps. Of course these are all just estimates, but by our math it isn’t practical to assume that week 51 of Foot Locker’s year is big enough, or bad enough to derail the topline expectations by a meaningful amount.

Additional Points to Consider:

- It’s no secret that the weather has had some impact on business across all of retail this month, not just the athletic channel. However, we must also consider the flipside which is the opportunity FL has to clear its boot/cold weather offering at a healthy margin aided by the tough weather backdrop. This cannot be quantified, but qualitatively bad weather during “normal” winter months can be good for sell throughs of cold weather product.

- Promotional activity remains benign, which bodes well for margins. For anyone that has been tracking their inbox over the past couple of months, we challenge you to email us a copy of a coupon good for an in-store discount. Yes, we’re aware of the constant barrage of promos centered on Eastbay or .com only, but the effort to drive sales via price has been noticeably absent of late. And yes, this applies in particular to the last couple of weeks.

Overall, we remain comfortable with our 6% same store sales estimate and $0.44 above Street estimate for FL’s fourth quarter. One week in late January does not change our thesis one bit. As such we’ve taken this opportunity to use the noise out there to add the position to Hedgeye’s virtual portfolio. Speculation is likely to remain high until the company reports in early March, however the momentum in the underlying business remains solid and on track to meet our admittedly bullish expectations.

Eric Levine

Director