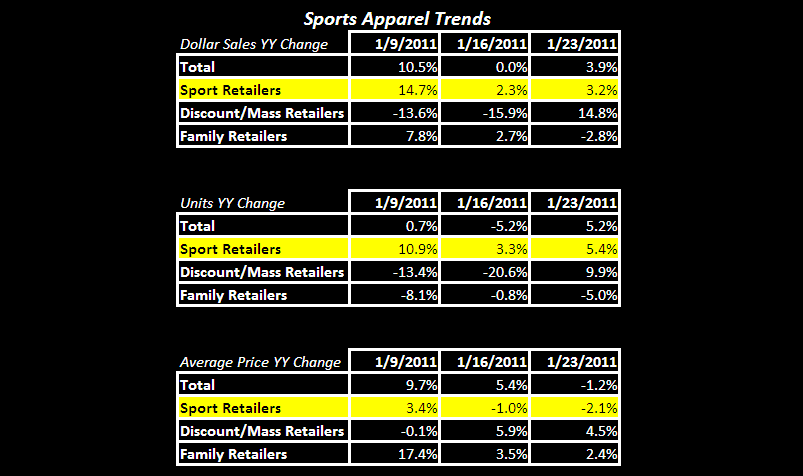

Underlying trends for athletic apparel remain strong with sales reaccelerating after a meaningful slowdown last week. The rebound was less significant than we had expected, however given unprecedented weather disruptions year-to-date, the reacceleration should be viewed positively on the margin. In looking at the regional trends in greater detail, there was a notable divergence between sales in western regions (Pacific and Mountain) compared to reaccelerating trends across all other regions – particularly the South Atlantic and South Central. While the national weather data suggests more precipitation out west than average last week, we suspect year-over-year comparisons to be the cause for underperformance.

Lastly, given disruptions over the last few weeks we expect to see continued acceleration in sales next week. With the final two weeks of the retail calendar accounting for 40%-50% more sales volume compared to the 1H of the month, January’s monthly performance will fall largely on the shoulders of next weeks’ results.

Casey Flavin

Director