NewsWire: 3/21/22

- According to Larry Summers, measured housing inflation will speed up in 2022 and through most of 2023. By late fall of this year, past housing inflation will cause the CPI to rise by one full percentage point over what it would be otherwise. (MarketWatch)

- NH: Over the last few months, many investors have been puzzled by the disconnect between the rapid rise in housing costs and the absence of any corresponding rise in the CPI.

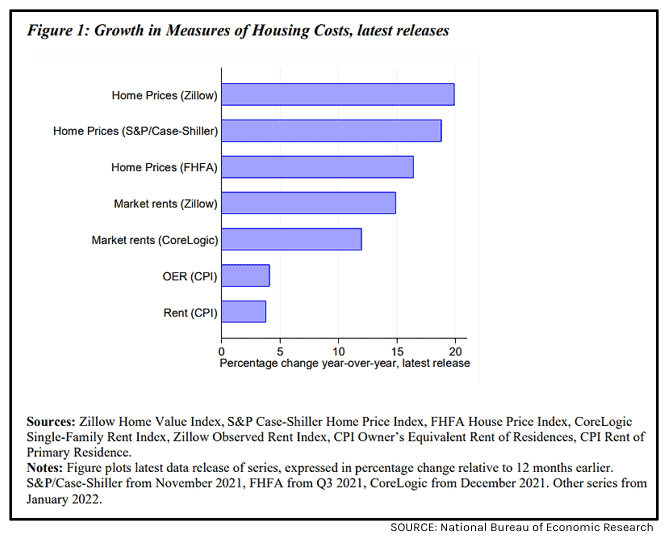

- According to Zillow's surveys, for example, housing prices jumped +20% and rent prices +15% over the 12 month period ending in January 2022. But according to the CPI, which also relies on monthly surveys, housing inflation rose only +4.1% for homeowners (OER or "owner equivalency rent") and +3.8% for renters over the same period.

- Now comes a much-cited paper by Larry Summers and two other economists that tries to account for this disparity. While the full explanation is quite technical, sometimes involving the complex and staggered survey methods employed by BLS, the basic story is pretty simple. Here it goes.

- All the private-sector measures like Zillow, Case-Shiller, etc., focus exclusively on housing prices and rental rates that have changed in the last month. Zillow only looks at price changes in homes now on the market and at changes in "asking rent" for new leases. The government measures, on the other hand, try to look at the housing values and current rents of all homeowners and renters.

- So when Zillow says that rents are up +15% YoY, what it means is that new rentals being asked are up by +15%. But most renters aren't paying those higher rates. Not yet, anyway. (More on that shortly.) Similarly, when Zillow says that home prices are up by +20%, the great majority of homeowners aren't affected by these new prices. True, the BLS does ask all homeowners how much they could now rent their home for. But honestly, most homeowners have no idea. And their estimates typically reflect what they originally paid for their homes, an amount which is no longer economically relevant.

- To sum up: It's not that either set of measures is wrong; it's just that they're trying to quantify two different things.

- Yet this difference results in two rather predictable gaps between the two measures.

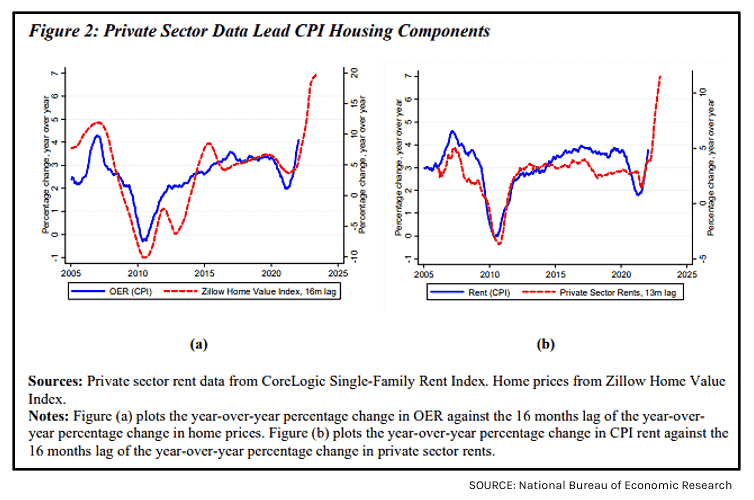

- First, changes in the private-sector measures will tend to be greater in amplitude than changes in the government-sector measures. That's because the private-sector measures will race up or down in response to how immediate market forces are pushing the relatively small share of all leases or homes that are being renegotiated during the month. The average for all housing units will show much more inertia.

- Second--and this is the most important--the private-sector measures will also tend to anticipate the direction of the government-sector measures. That's because a strong and durable rate-of-change shift in market forces lasting over several months (or years) will steadily affect a greater share of all housing units with each passing month. The Summers team calls the combined government housing cost figure "a backward looking measure."

- Great. So now you may ask: Are the amplitudes and lags constant? And, if so, does that mean that the government numbers can be forecasted from the private numbers?

- According to the Summers team: yes and yes.

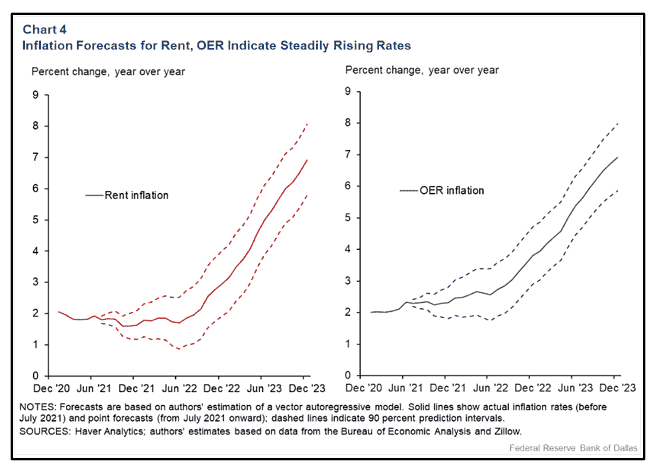

- Over time, the amplitudes of the government-sector measures for OER and rent are reasonably steady at roughly 15% and 50% (respectively) of the amplitude for the private-sector measures. And the lags are also steady, at about 12 months for rent and about 18 months for OER.

- In this chart, the amplitude difference is reflected in the calibration of the Y-axis scales, more dilated for the (left-hand) government measure than for the (right-hand) private-sector measure. As for the two lags, they work pretty well in this simple backcast.

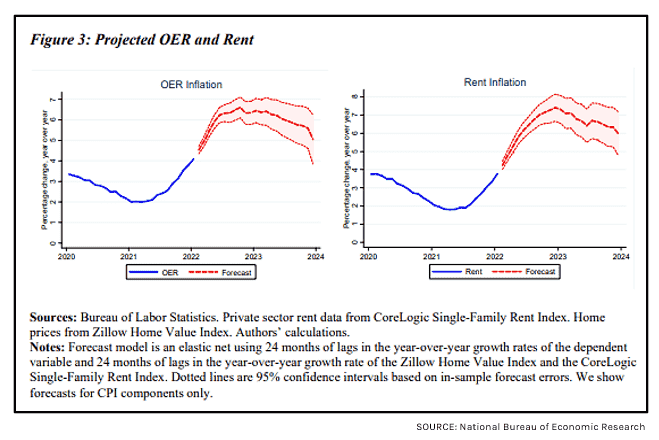

- The authors then model the future using a simple ML regression method ("elastic net"). They find, in this forecast, that both the OER and rent components of the government measures will indeed rise in future months in a trajectory similar to the one implied by the backcast. The OER will rise through most of the rest of this year, from just under 4% to between 6% and 7%. And the rent will rise by a slightly greater amount. While both measures will decline gradually during 2023, they will remain well over current rates until the end of that year.

- So what does this imply for inflation? You can find the details in the paper. But the bottom line is this: Per this forecast, the combined housing component of the CPI (which has close to a 40% weight within the CPI) will rise by 2.9 percentage points YoY by December 2022. That implies a +1.0 positive push to the overall CPI over what it is now; a +1.1 push to "core" CPI; and a +1.5 push to CPI "services." The boost to the PCE deflator will be smaller, given housing's smaller weight within the PCE.

- The Summers team is by no means alone in this forecast.

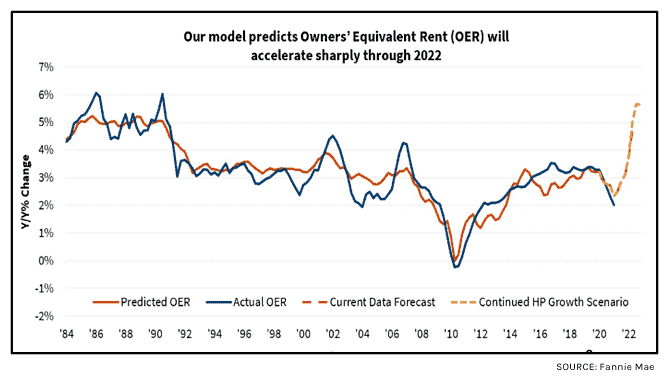

- Researchers at Fannie Mae (whom the Summers' team acknowledges) came to much the same conclusion in June of last year. They did a simple OLS regression on the same backcasted relationship and came up with their own forecast. Because they did not yet know about the last six months of 2021, their projected increase through the end of 2023 (understandably enough) was not quite as high as in the Summers' paper.

- In August 2021, researchers at the Dallas Fed once again came to a similar conclusion. Their projection shows much the same trajectory.

- The Dallas model points to the housing component hitting 6.9% by December 2023--which is 0.3% higher than the Summers model. And now there's a new model by researchers at the San Francisco Fed. Their prognosis: "Applied to CPI inflation, our results imply an additional increase of 1.1pp for both 2022 and 2023. Applied to PCE inflation, which is the measure used by the Federal Reserve to gauge its 2% inflation target, our results imply an additional increase of 0.5pp for both 2022 and 2023." Again, these numbers are marginally higher than in the Summers' forecast.

- To be sure, Larry Summers has a reputational stake in his team's findings. Early last year, he warned the Democrats about large budget deficits in the midst of ongoing monetary stimulus from the Fed--and told them that inflation was likely to exceed their expectations a year later. He got that right. And, as Summers often does, he delighted in reminding everyone that he was right. What's more, he believes more is on the way. But Summers is no longer alone. Plenty of other economists are coming to the same conclusion.

- Needless to say, this puts the Fed into an even worse position than it was in already. The current Fed action plan (10 more 0.25% hikes over the next two years plus as-yet unspecified quantitative tightening) hinges on its success in quelling inflation. And that inflation is currently racing 300+ basis points over the Fed's long-term PCE-deflator target. No doubt Fed Chairman Powell hopes he is so successful that he can defer many of the scheduled hikes--thereby conquering inflation while simultaneously keeping the economy out of recession.

- Powell is worried about plenty of incoming news that could derail this happy scenario--starting with higher global energy and food prices triggered by the Ukraine war. Now here's something else that will make his job that much harder: the upcoming inflation boost already baked into future CPI and PCE prints due to a massive 21-month surge in housing prices.

| To view and search all NewsWires, reports, videos, and podcasts, visit Demography World. For help making full use of our archives, see this short tutorial. |