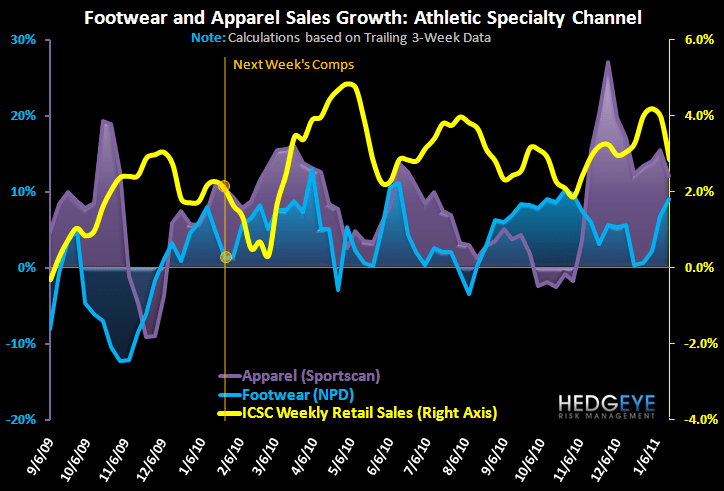

Underlying trends for the athletic space remain very positive despite a meaningful deceleration in the latest week’s data. We’re going to float some benefit to the industry for taking a sales hit last week due to weather, and therefore expect it to pick up meaningfully this week. It is also worth noting that the second week in January has been among the Top 5 lowest grossing weeks in footwear in each of the last 2-years with the final two weeks of the retail calendar typically recording 40%-50% more sales volume compared to the 1H of the month. Here are a few key callouts from the week:

- The bifurcation between performance and non-performance footwear continues to be at near-term highs of a 40% differential. Product portfolio management continues to be a potential source of outperformance at individual retailers – good for DKS & HIBB, even more favorable for FL & FINL.

- In apparel, Running and Basketball apparel were the clear positive callouts accelerating on the week up +17% and +11% respectively while Outerwear was not only noticeably absent from the top performing categories, but actually turned negative on the week down -5%.

- Sales of sports apparel at athletic specialty retailers continue to outperform up +2.3% on the week compared to +0% for the overall category. The family channel lead the week up +2.7%.

- Continued apparel ASP increases were offset by a decline in unit sales across the industry reflecting the impact of anomalous weather. Sport Retailers were the only channel to increase unit sales on the week driven by lower prices down -1%.

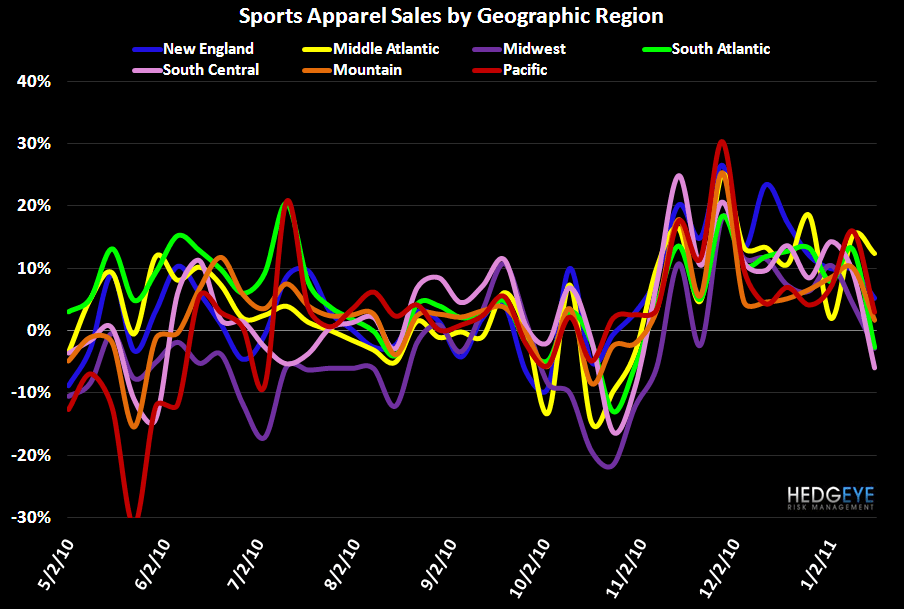

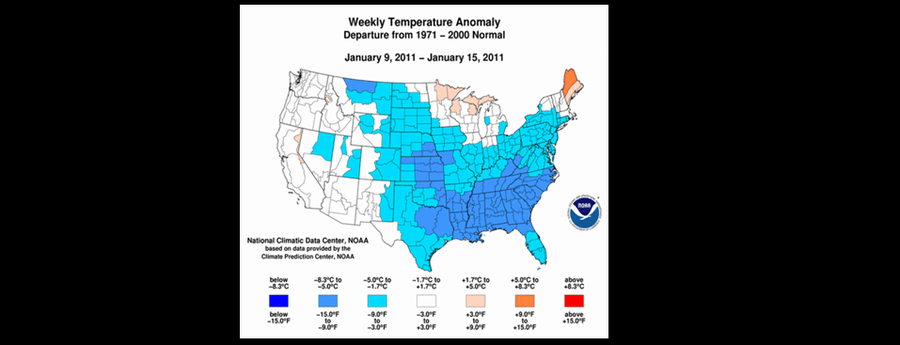

- On a regional basis, the South Central and South Atlantic regions materially underperformed after snow blanketed the region early in the week causing many businesses to close Monday. The Mid-Atlantic region was the positive callout up +12% after bringing up the rear only 2-weeks ago.

Casey Flavin

Director