This week we are rolling out our weekly commodity monitor.

Commodity costs, and how companies manage them, are going to play a large role in deciding the winners and losers in the restaurant space in 2011. This product is going to be developed further over the coming weeks and makes up an important part of our daily process.

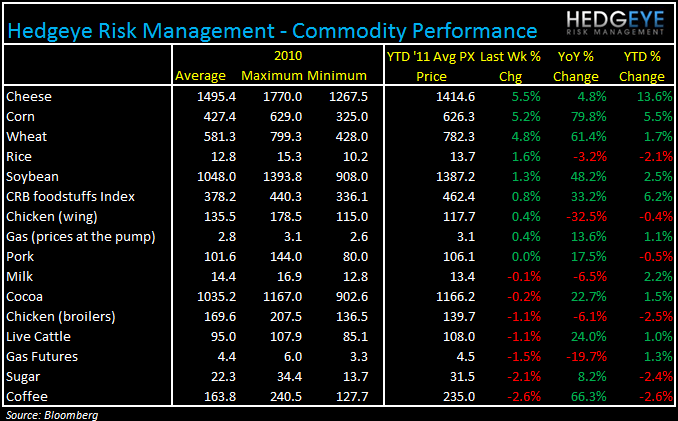

KEY TAKEAWAYS

1. The sharp increase in dairy costs, especially cheese, is notable for many companies within the restaurant space.

- CAKE’s COGS increased by 50 basis points last quarter largely due to pressure from dairy and cheese costs. The company’s commodity basket remains exposed to dairy.

- DPZ saw margins impacted adversely by rising cheese prices in 3Q10. Cheese prices in that quarter rose 28.6% versus the prior year, according to management commentary on the earnings call.

- CMG recently moved from contract to spot prices for sour cream in order to source from local and organic sources. The company is exposed to the possibility of further gains in food stuffs prices given their sourcing of ingredients from spot markets.

2. Coffee prices came down week-over-week. The absolute level remains high, however, and the year-over-year column tells the more pertinent story for coffee vendors.

- SBUX have raised coffee prices along with many others in the space due to the upsurge in coffee prices over the past year.

- The recent abatement will provide some relief for SBUX, GMCR, and PEET.

3. Beef costs slowed down week-over-week. Year-over-year, prices are still at high levels and will impact the bottom line of many restaurant stocks as we move through 2011.

- SONC is only locked in on beef costs through the end of January 2011, according to their most recent earnings transcript.

- MCD guidance is for approximately 1-2% of blended food basket inflation in 2011. I expect high year-over-year margins to hamper MCD’s efforts to maintain the lofty margins achieved in recent quarters, helped greatly by beverage sales. See my latest MCD Black Book for details.

- PFCB is locked in for beef for 2011.

- TXRH has 80% of protein needs contracted for 2011.

- MRT disclosed that it is not contracted on any beef purchases past 2010 and expressed a willingness to pursue several strategies, including taking price, if appropriate.

Howard Penney

Managing Director